Fast reading

- In May, Moody’s stripped the US of its triple-A credit rating, leaving the world’s largest economy without a top rating for the first time in over a century.

- The volatile market conditions support the case for a flexible and dynamic multi-asset credit investment approach.

- An unconstrained strategy has the ability to adapt to market conditions and can pull multiple performance levers to try and optimise results.

US President Donald Trump has adopted a scattergun approach to his implementing flagship tariff scheme since taking office in January.

In the space of few weeks, the US imposed 145% tariffs on China – the world’s second-largest economy – only to back peddle and drop them down to 30%. The US trade court ruling on 28 May that Trump’s ‘liberation day’ tariff scheme is illegal only adds to the sense of confusion. The US administration is appealing the ruling.

Beyond the economic impact of the tariffs themselves, the abrupt back-and-forth rollout has caused a lot of uncertainty and left markets in a bit of a holding pattern. It is hard to set out a long-term position when a single social media post can add – then wipe out – US$2.4tn of market value in seven minutes.

Meanwhile, rising levels of government debt and a widening budget deficit in the world’s biggest economy led Moody’s1 to strip the US of its triple-A credit rating for the first time in over a century.

The volatile and uncertain market conditions support the case for a flexible and dynamic multi-asset approach to credit investment.

An unconstrained strategy can adapt and respond to choppy and turbulent conditions, and has the ability to pull multiple performance levers to potentially generate alpha.

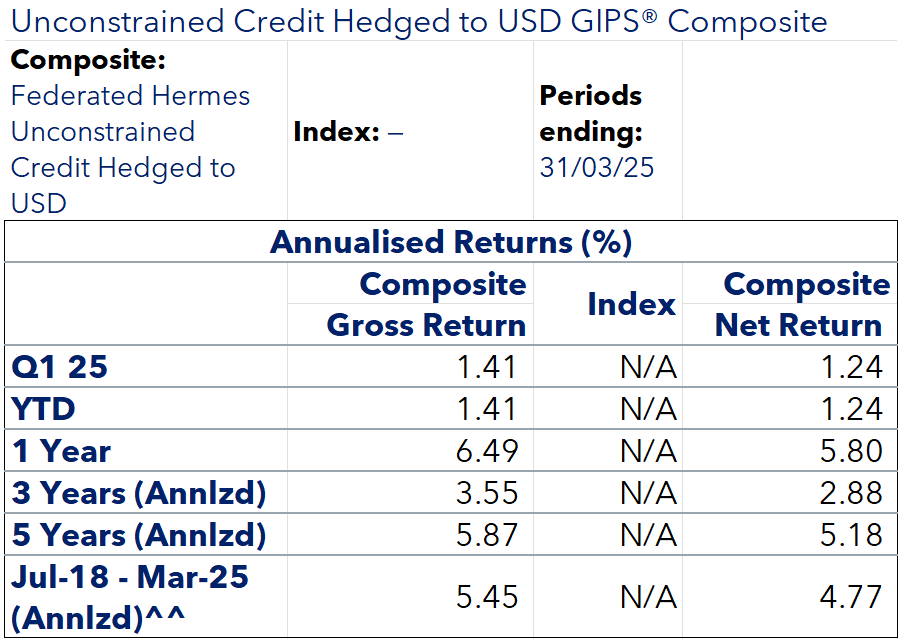

Figure 1: Taking an unconstrained approach

Note: The unconstrained strategy does not have a benchmark. The comparison depicted in figure 1 serves to demonstrate the difference between an unconstrained and other approaches to credit investing.

Source: Federated Hermes. Performance data as at 31 March 2025. Performance shown is the Federated Hermes Unconstrained Credit Hedged to USD strategy. Performance is in USD, gross of fees. Management fees will have the effect of reducing performance. Subscription and redemption fees are not included. Data is supplementary to GIPS® report that follows. Past performance is not a reliable indicator of future returns.

^^Represents composite inception period. See below for additional notes to the schedule of rates of return and statistics.

*Represents the 3-year annualized standard deviation for both the gross composite and the index returns. Statistic is used to measure the volatility of composite returns.

**Standard deviation is calculated using gross returns. Standard deviation is not applicable (N/A) for any period if fewer than five accounts are in the composite for that period.

The composite includes all discretionary portfolios following the Unconstrained Credit Hedged to USD strategy run by the Federated Hermes Global Credit team (London Office) and has an inception date of 1 July 2018. The objective of the strategy is to generate capital growth and a high level of income over the long term. The strategy may invest in a broad range of assets, either directly or through the use of derivatives, (including, but not limited to, equities, equity-related securities, Eligible CIS and/or financial indices, futures, options, swaps, debt, fx and money markets). The strategy through its investments in FDIs may be leveraged. The composite does not have a benchmark as it is an absolute return strategy, which aims to achieve capital appreciation regardless of market conditions. This composite was created in August 2018. Performance shown for 2018 is for a partial period starting 1 July 2018. Federated Hermes claims compliance with the Global Investment Performance Standards (“GIPS®”) and has prepared and presented this report in compliance with the GIPS® standards. Federated Hermes has been independently verified for the period of January 1, 1992, through December 31, 2024. The verification report is available upon request. A firm that claims compliance with the GIPS® standards must establish policies and procedures for complying with all the applicable requirements of the GIPS® standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS® standards and have been implemented on a firm-wide basis. Verification does not provide assurance on the accuracy of any specific performance report. The management fee schedule for this strategy is 0.65% per annum. Gross of fees returns have been calculated gross of management/custodial fees and net of reclaimable withholding taxes, but after all trading commissions.

Federated Hermes is a global, independent, multi-strategy investment management firm. For GIPS® purposes, Federated Hermes is defined to include the assets of registered investment companies that are advised or sub-advised by the various Federated Hermes advisory companies. Effective September 30, 2020, for GIPS® purposes the name of the firm was officially changed to Federated Hermes. Firm assets on this report exclude assets affiliated with Hermes GPE and the advisory-only, model-based assets that may be included in other reports providing total firm assets. Interest income and dividends are recognized on an accrual basis. Returns include the reinvestment of all income. All market values and performance information are valued in USD unless currency is denoted in composite description. Annual composite dispersion is measured and presented using the asset weighted standard deviation of the gross returns of all of the portfolios included in the composite over the entire year. See the composite description language for a discussion on appropriate fees currently applied to calculate composite performance. Net composite results are based off model fees using the stated fee schedule. In addition, further fee information can be obtained from the firm’s respective Forms ADV Part 2 Brochure Item 5. Additional information regarding the policies for valuing investments, calculating performance, and preparing GIPS® reports, as well as a complete list and description of the firm’s composites and pooled funds is available upon request. Past performance is not indicative of future results. GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. See disclosures on the Schedule of Rates of Return and Statistics Reports for additional information.

An option overlay

One such lever is an option overlay2 which seeks to hedge against downside risk. It is intended to allow for a degree of adjustment to the portfolio’s risk level, depending on prevailing market conditions, while limiting turnover. The reduced volatility also adds to the potential for strong risk-adjusted returns.

These levers also extend to sub-asset class opportunities. For example, structured credit – particularly asset-backed securities (ABS) – can be another driver of outperformance.

Asset-backed securities are a vital part of the financial system, providing liquidity and funding for a range of consumer and commercial loans and leases.

ABS offer a way for lenders to free up capital and for investors to gain exposure to different types of assets. They play a crucial role in the financial ecosystem by enhancing liquidity and providing investment opportunities.

An unconstrained strategy can adapt and respond to choppy and turbulent conditions

Positioning our Strategy

Fundamental to any market outperformance is portfolio positioning. We have identified several pockets of opportunity amid such an uncertain market backdrop.

Financials, for example, have been resilient through the tariff-talk. Banks, particularly in Europe, are fundamentally sound with solid capital ratios following years of balance-sheet repair and revenues are supported by a range of factors including falling deposit costs, and higher income streams. Finally, financials are largely out-of-scope from direct impact of a tariff war.

We see evidence of fresh buybacks driven by capital strength and there does not appear to have been any demonstrable deterioration in asset quality.

The Federated Hermes Unconstrained Strategy has an overweight positioning in AT1s (convertible fixed income instruments primarily issued by financial institutions), which has bolstered our performance in recent months.

Where next?

The Trump administration has demonstrated a flexibility to back peddle from the more strident elements of its tariff programme.

It’s an optimistic signal and could encourage a more ‘risk-on’ approach from many investors going forwards.

As we have previously seen, mostly notably in the autumn of 2024, a more risk-on environment can present buying opportunities in the options market. We are anticipating another entry point before adding further protection to the portfolio.

We expect to continue to see opportunities between the US and Europe in particular, given the events unfolding in the US together with the hope that austerity is easing in Europe. Elsewhere, and the volatility from tariffs is providing attractive potential opportunities in emerging markets (EMs).

1 Source: Ratings.Moodys.com/ratings-news/443154

2 Option overlay strategies can be constructed to mitigate systematic risk, enhance portfolio income, or improve risk/return, enabling investors to efficiently achieve long-term portfolio objectives. Overlays can use derivative investment vehicles to obtain, offset or substitute specific portfolio exposures, beyond those provided by the underlying portfolio assets.

BD016009