Fast reading

- EMD has delivered a strong performance in 2025, and we believe the backdrop looks supportive of further outperformance in 2026.

- Leading EM central banks are running orthodox monetary policy, which has helped anchor prices and set long-term inflation expectations.

- Select exposure to local currency bonds could prove to be a significant source of alpha in 2026.

Emerging market debt (EMD) has outpaced both developed market (DM) and broader fixed income gains in 2025. The asset class has benefited from shifts in the investment environment, which have set the stage for further opportunities.

Hard currency EM sovereign bonds have returned over 12% year to date, while EM local currency bonds have returned 15%1 – and these returns have been balanced between both capital appreciation and income. We believe the momentum behind EMD looks likely to continue into 2025, as the asset class continues to benefit from a series of wide-ranging reforms that have reinforced stability in various domestic markets.

Building the foundations

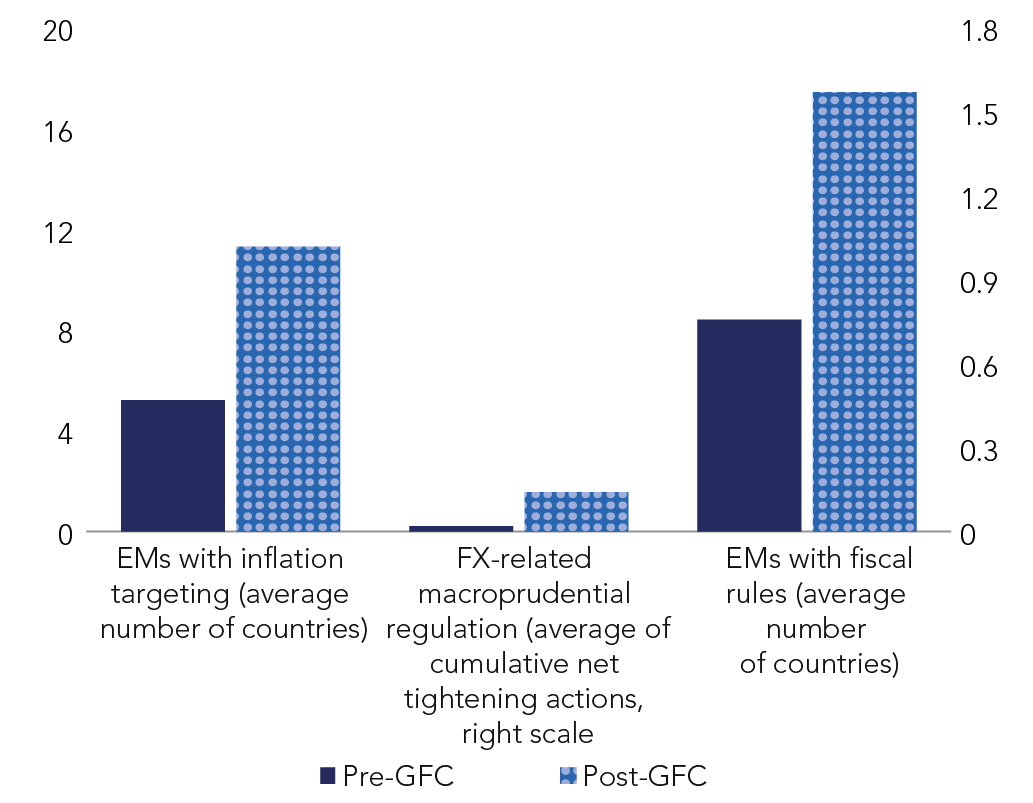

Emerging markets have historically been vulnerable to global financial shocks, such as the 2008-09 global financial crisis (GFC). However, EM authorities responded to the market meltdown by adopting inflation-targeting regimes and fiscal rules, as well as tightening macro-prudential regulations. These post-GFC reforms have played a crucial role in bringing greater macroeconomic stability in the wider EM region.

These post-GFC reforms have played a crucial role in bringing greater macroeconomic stability in the wider EM region.

Figure 1 illustrates the extent of the reforms carried out in the wake of the GFC. The imposition of these frameworks served to enhance these markets’ ability to absorb external shocks and stabilise economic conditions. Stronger policy frameworks also helped enable access to IMF precautionary instruments, which are designed to meet the liquidity needs of member countries.

Figure 1: The 2008-09 GFC spurred policy reforms across EMs

Source: The International Monetary Fund (IMF).

Figure 2 shows how improved policy frameworks and fiscal discipline have helped boost the broader macroeconomic picture for EMs

Figure 2: EMs boast stronger fundamentals

Source: The International Monetary Fund (IMF). Past performance is no guarantee of future results.

The Covid-19 crisis in 2020-21 put these frameworks to the test as the economic fallout from the pandemic was followed by a surge in global inflation.

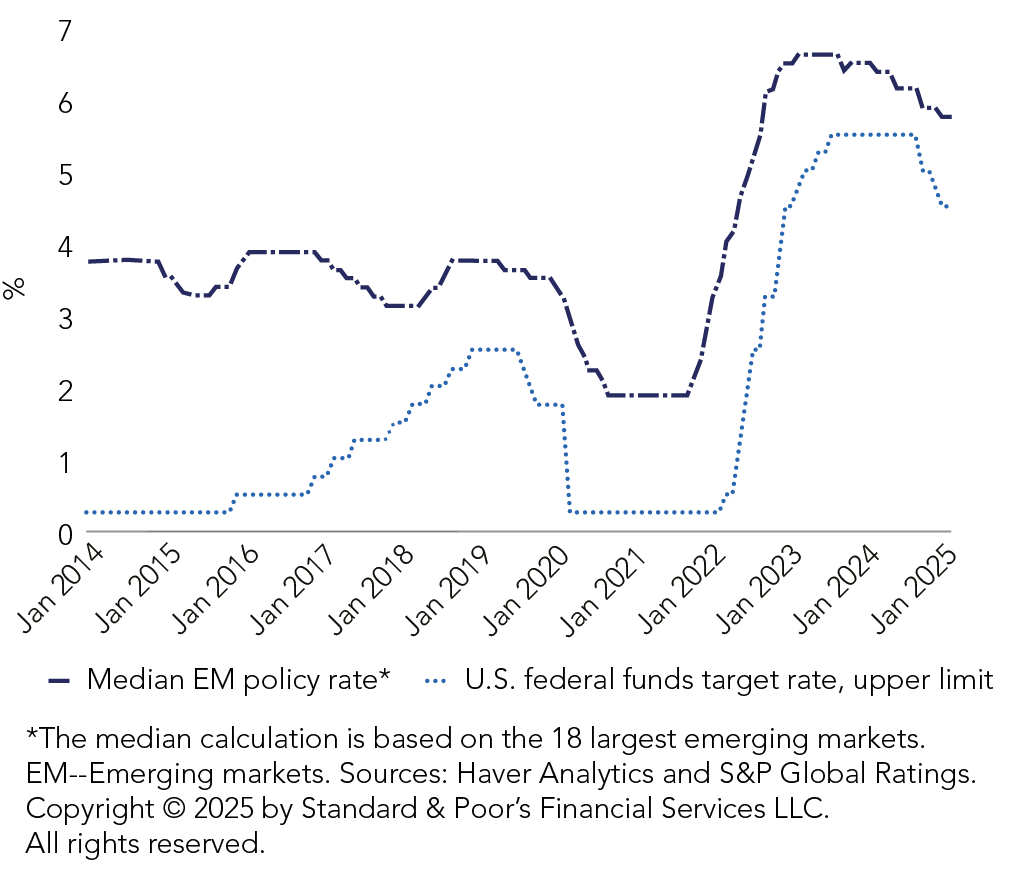

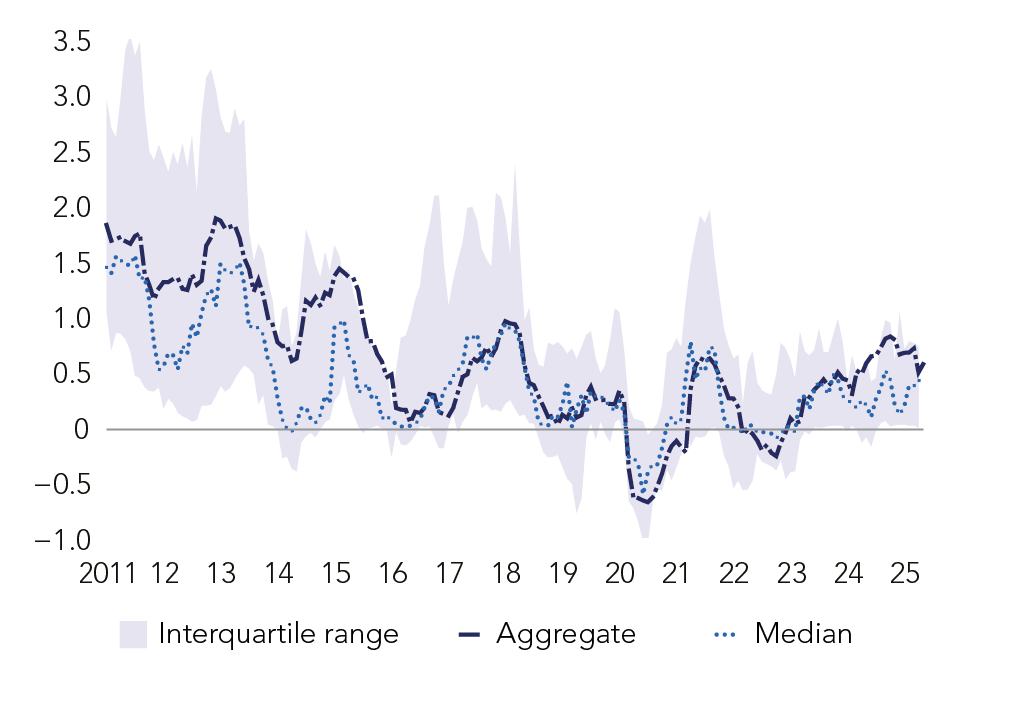

While some, including former US Treasury Secretary Janet Yellen, believed this inflationary surge would be transitory2, many EM central banks took a more cautious approach and began hiking interest rates much earlier and at a faster pace than their DM counterparts (Figure 3).

Figure 3: EMs moved quickly to head off pandemic inflation risk

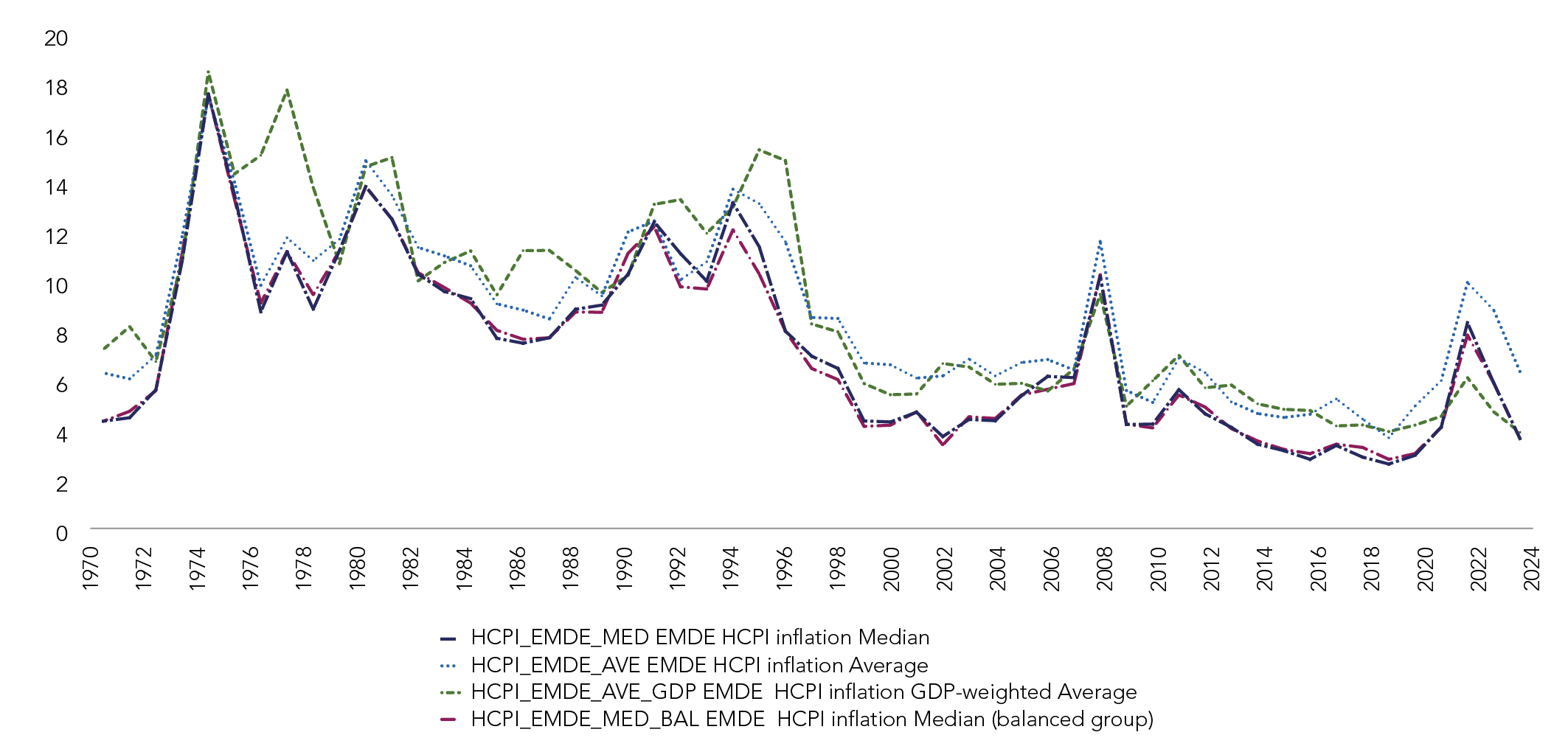

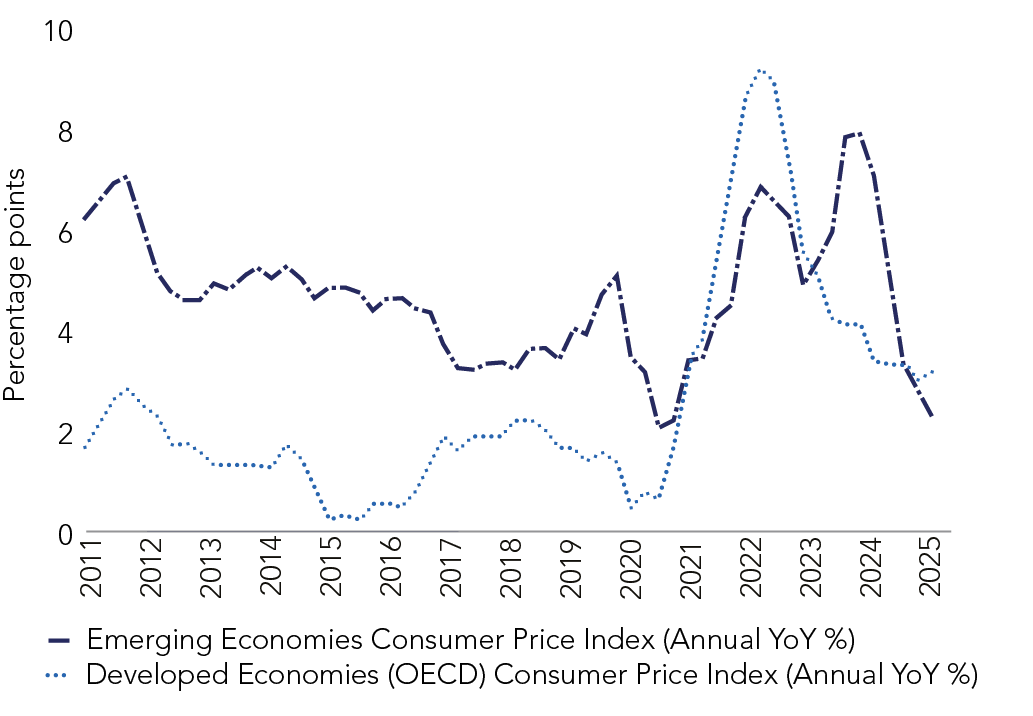

Leading EM central banks have prioritised credible, orthodox monetary policy to anchor prices and moderate long-term inflation expectations. Brazil, Mexico, and Chile, among others, began their tightening cycles in 2021, which has helped bring inflation under control faster than developed market counterparts (Figures 4 and 5)

Figure 4: EM inflation is coming down

Source: The World Bank. Version: April 2025

Figure 5: Inflation trends invert

Source: Bloomberg as at 25 November 2025.

The moderation of domestic inflation means that EM central banks now have this additional capacity to stimulate economic growth through rate cuts, heading into 2026.

Targeting local opportunities

Another positive driver is the concerted effort to increase domestic ownership of local currency EM bonds – denominated in issuers domestic currencies – which have the knock-on benefit of making EM economies less dependent on foreign inflows and the instability that this can lead to during times of market stress.

The term the ‘Fragile Five’ was coined by Morgan Stanley in 2013 to describe five EM economies – Brazil, India, Indonesia, South Africa, and Turkey – that were perceived as particularly sensitive to capital outflows because they exhibited sizable current account deficits and leaned heavily on foreign investment. The so-called ‘taper tantrum’ in 2013 – market volatility sparked by the Fed tapering quantitative easing – had a significant impact on the five economies.

As a result, many EMs have sought to increase the role of resident buyers in their financing strategies. Sovereigns are no longer heavily reliant on external borrowing as domestic markets have expanded (see Figure 6).

Bangladesh, for example, identified local currency bond market development as a policy priority3 and foundational reforms doubled the nominal stock of marketable bonds between 2019 and 2024. Georgia’s Ministry of Finance, meanwhile, launched a programme in 2020 which improved price discovery on benchmark bonds.

EMs with higher shares of local currency debt and more diverse investor bases have exhibited more stable bond yields and market liquidity during periods of global stress, according to IMF research4.

Figure 6: Foreign flows to local currency bonds markets have slowed

Source: The World Bank.

Local issuance remains strong even as foreign flows slow. EM-17’s corporate and sovereign issuance has reached US$286bn in 20255, exceeding the record-high level set in 20216. As a consequence, these countries have seen their currencies appreciate by a median value of 4% year to date, while the median of real yields exceeds that of developed market counterparts by 330 basis points (bps)7.

We are selectively increasing exposure to local currency bonds in response to this trend of EMs building out more robust domestic markets. We believe exposure in this area could prove to be a significant source of alpha in 2026.

Dollar weakness as a catalyst

A weaker US dollar and the resumption of the Federal Reserve’s easing cycle have helped provide supportive financing conditions for EMs in 2025 and we expect this favourable backdrop will continue in 2026.

President Donald Trump has repeatedly expressed his desire for swifter and deeper cuts from the US central bank and has aimed a number of barbs at Fed Chair Jerome Powell. Powell’s stint as chair ends in May 2026, leaving Trump the option to install a new chair who is more aligned with his priorities.

Meanwhile, US CPI has remained stubbornly above the central bank’s 2% target, but it has spent the better part of the year contending with a choppy labour market. The Fed may have to prioritise stimulating economic growth over tackling inflation, which would point to further rate cuts. The weakness of the US dollar has already been a major theme in 2025 – it is down by around 8.2%8 YTD – and more rate cuts are likely to put further downward pressure on the greenback.

A weaker US dollar, however, particularly benefits EM issuers with a significant share of unhedged debt denominated in US dollars.

Countries to watch

We see strong potential in several frontier markets. Disinflation is underway in Nigeria as a result of wide-ranging reforms, and the central bank has started to cut rates to support growth for the first time since the pandemic. Sri Lanka’s economic reform programme is positive for the country’s long-term outlook and we are optimistic about its prospects. Ecuador’s fiscal profile is improving, and the IMF has noted substantial progress on the implementation of their structural reform agenda, notably on fiscal, governance, and growth-enhancing areas9.

We are also positive on several countries supported by orthodox macroeconomic policies that have anchored spreads. Turkey South Africa and Brazil all offer a valuable income component on this front.

The economic rebound in Argentina remains a compelling story, particularly following the mid-term election result in October, which saw a landslide win for President Javier Milei’s party. The Trump administration’s US$20bn support package, should help to unlock further value. Meanwhile, Columbia’s debt buyback strategy – part of efforts to cut borrowing costs – looks set to deliver a boost to the country’s sovereign debt.

EMD report Q4 2025

For more information on Emerging Markets Debt

1 Source: Bloomberg, as at 5 November 2025. Past performance is not a reliable indicator of future performance.

3 ch3.pdf

4 Ibid

5S&P Global. 30 September 2025.

6 The EM-17 group includes 17 EMs, namely Argentina, Brazil, Chile, Colombia, Egypt, India, Indonesia, Malaysia, Mexico, Nigeria, Peru, the Philippines, Saudi Arabia, South Africa, Thailand, Turkiye, and Vietnam.

7 Emerging Market Brief: Weak Dollar And High Real | S&P Global Ratings

8 US dollar index as at 27 November 2025.

BD016934