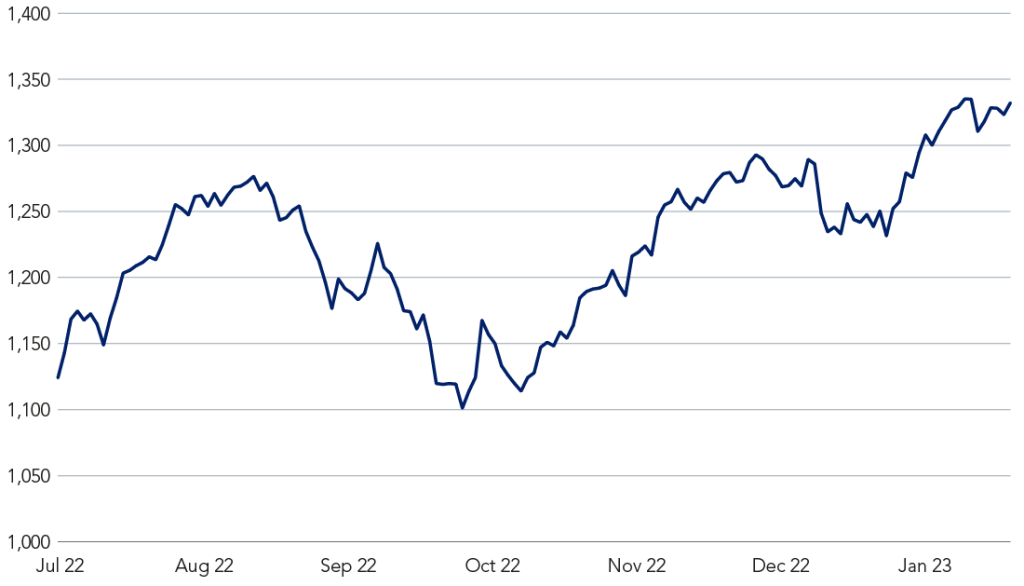

- The regional Euronext 100 index is up 8.17% year to date, while Germany’s Dax Index is 8.68% higher.

- Market optimism tempered by hawkish rhetoric from central bank officials with the ECB expected to deliver 50bps hikes at its next two meetings.

Equities have made an upbeat start to the year, amid indications that inflation is slowing and boosted by the re-opening of the Chinese economy after Beijing abandoned its zero-Covid policy. European stocks, in particular, have surged in January, supported by expectations that the eurozone will avoid a recession this year.

“European markets have performed particularly well as the mild winter weather reduced the likelihood of energy rationing and gas prices have declined, reducing fears of a recession,” says James Rutherford, Head of European Equities at Federated Hermes Limited. “In addition, investors are placing a higher probability on the US Federal Reserve engineering a soft landing by taming inflation without pushing the economy into a recession,” he says.

“The re-opening of China should also provide a relative tailwind for Europe versus other regions. European equity benchmarks have higher weightings in Materials, Energy, Industrials and Consumer Discretionary sectors which tend to be more geared to Chinese demand.”

The regional Euronext 100 index was up 8.17% year to date as at 16:30 on 26 January, while Germany’s Dax Index rose 8.68%1. On the other side of the Atlantic, the US benchmark S&P 500 was up 4.92% over the same period.

Figure 1: Euronext 100 on the rise

Hawkish rhetoric

Market optimism has, however, been tempered by hawkish rhetoric from central bank officials. The European Central Bank (ECB) hiked rates four times last year in a bid to control high inflation, pushing the main deposit rate up from -0.5% to 2%. But despite a two-month consecutive drop in headline inflation, ECB officials have emphasised the need to “stay the course” in its policy.

Core inflation in the eurozone is still running at an all-time high (5.2%) and wage growth has picked up to about 4%2. December’s headline inflation of 9.2%3 remains a long way off the ECB’s 2% target and the central bank is widely expected to deliver 50bps rate rises at each of its next two meetings.

The eurozone economy has performed better than expected through the energy crisis

“The eurozone economy has performed better than expected through the energy crisis – stagnation for a couple of quarters at the turn of the year seems now to be more likely than outright GDP contraction. Granted, good luck has played a role as winter temperatures have been mild so far, but preparedness and the long tail of post-Covid recovery dynamics have also underpinned economic resilience,” says Silvia Dall’Angelo, Senior Economist at Federated Hermes Limited.

“An EU multi-year fiscal plan mainly targeting the most vulnerable eurozone members and, more recently, the quick re-opening of the Chinese economy are sources of upside risk to the eurozone economic outlook, although we expect global spill-overs from this stage of the recovery in China to be limited,” she adds.

A cautious outlook

The inflationary environment continues to eat into corporate profitability and earnings so far this year have been muted. “There was a time when the recession felt inevitable – particularly in Europe – and while that may no longer be the case, we believe the likelihood remains high,” says Lewis Grant, Senior Portfolio Manager – Global Equities at Federated Hermes Limited.

“As investors ponder whether the rally is merely paused or truly over, it’s worth considering the lessons of past bear markets. While by historic standards this bear market is not deep, especially with a recession yet to come, markets do tend to rebound ahead of the economy,” Grant adds.

“Longer term, China’s reopening may bring growth, but also has the potential to exacerbate inflation. Positive developments, such as a return to more stable energy prices and a weakening dollar, are encouraging, but past experience has taught us that volatility can return quickly.”

For further insights into the key themes that could shape markets in the year ahead, please see Federated Hermes 2023 Outlook