When investing for the long term, many people find it difficult to choose the right time to make inflows or outflows in a portfolio. They tend to rely on funds that have performed well to make inflows and therefore can be expected to perform better in the future. Conversely, if a fund performs poorly, net outflows are normal. But a rise can sometimes be fleeting, and a fall can be short-lived. So how do you make these decisions to maintain (and even increase) investment returns?

For Federated Hermes, the key is an active and responsible investment strategy to grow invested assets over time. Its investment team includes portfolio managers who take a contrarian approach to investment – i.e., they bet on assets that are not doing well in the market for reasons they consider temporary, so that when they recover, they can obtain optimal results. The approach seeks to maximise risk-adjusted returns (the balance between return and risk associated with an investment).

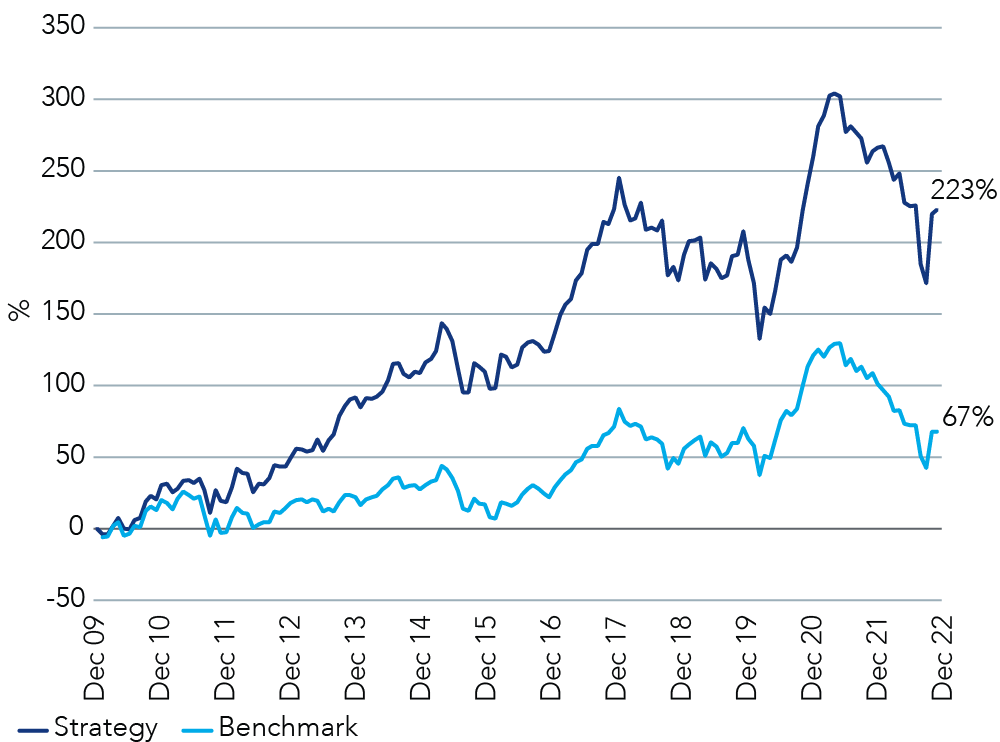

The objective is to help its clients identify a contrarian investment opportunity that is capable of outperforming its benchmark. This “search for yield followed by a deep drawdown” is the manager’s rule. And a clear example of this is the Asia ex-Japan Equity Strategy, which has managed to achieve quality and cheap valuation versus the benchmark (MSCI AC Asia ex-Japan Investable Market Index).

Jonathan Pines, Lead Portfolio Manager, in his annual Letter to Investors reviews the Strategy since its launch in 2010. He highlights that in years when the benchmark index has fallen, the Strategy has outperformed its benchmark. As a result, long-term investors – those who have held on during portfolio swings – have significantly outperformed that index, to achieve the highest level of cumulative relative performance since the Strategy’s inception.