Physics is broken.

Every physicist knows the two fundamental theories of reality – quantum mechanics and general relativity – remain hopelessly estranged after more than a century of uncomfortable co-existence.

Resolving this theoretical dissonance has consumed some of the biggest brains in science since the early 20th century. The most promising efforts to address the quandary emerged in the 1970s as the ‘string theory’ movement took hold.

Instead of treating subatomic particles as the fundamental building blocks of matter, string theory contends that everything is made of unbelievably tiny strings, whose vibrations produce effects that we interpret as atoms, electrons and quarks1.

String theory’s complex mathematical model has developed into an all-purpose explainer for the nature of everything – even the mystery of the universe itself.

The theory’s advocates contend that that the universe conducts itself – at its most elementary level – like a complicated musical symphony, producing spectacular harmonies and rhythms. As it stands, however, we do not yet understand the score.

Figure 1: String theory’s multiple dimensions

Standard Euclidean geometry (left) vs. string theory’s topological perspective (right)

Alternative dimensions

According to general relativity, we live in four dimensions – height, width and depth, and time. For string theory to become viable, it requires at least 10 ‘spacetime’ dimensions (See Figure 1). A mind-bending leap of understanding for most people.

In the modern financial world, credit analysts – while probably not as wound-up as theoretical physicists – have also been searching for explanations in alternative dimensions in recent years as markets defy the standard debt model.

In a late 2021 article, for example, Fiorino questioned whether the long-term relationship between credit quality and US unemployment statistics had broken down2.

Fast forward to mid-2023 and US consumers remain bullish despite the possibility of a recession – albeit diminishing – and the risk of job losses.

Any worries US workers have about future employment is not evident in the New York Fed’s latest quarterly report on household debt and credit (see Figure 2).

Total US household debt rose by US$16bn to reach US$17tn in the second quarter of 2023, the official government statistics show3.

Similarly, Credit card balances saw brisk growth, rising by US$45bn to US$1tn. Other balances, which include retail credit cards and other consumer loans, and auto loans increased by US$15bn and US$20bn, respectively.

Figure 2: Outstanding US consumer debt

And creditworthiness remains strong as the historical auto loan data below highlights (see Figure 3).

Figure 3: Credit scores at origination for auto loans

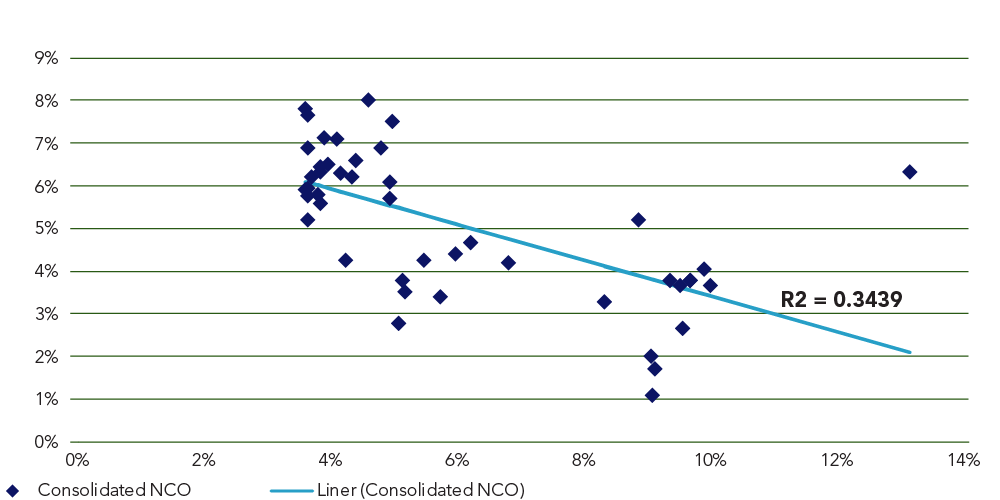

Fiorino repeated its December 2021 exercise, mapping the relationship between net charge off (NCO) rates and unemployment for two US lenders in the Federated Hermes credit portfolio, Ally Financial and OneMain Financial (OMF) with Q1 2023 data.

The statistical correlations between NCOs and unemployment for both institutions have barely changed over the previous 18 months, deferring once more the long-expected uptick in consumer loan defaults associated with a slowing economy (see Figure 4).

Figure 4: Consolidated NCO and US unemployment rate

The credit and default data provides a timely reminder to investors: never underestimate US consumers, which represent almost 70% of GDP, and seem able to continue servicing more debt, despite the risks and possible advent of a recession.

What’s holding the economy together?

As US consumer credit quality continues to surprise on the upside, analysts have downgraded their gloomier predictions based on a number of underlying factors, including:

- Persistently tight labour markets for service and hourly wage jobs – a trend that should limit the impact of any slowdown should it occur with middle- and lower-income consumers also likely to benefit from cheaper gas and moderating inflation.

- The ongoing impact of the massive US savings buffer accrued during the Covid-19 years. Despite recent rapid drawdowns of those savings, a large amount – around US$500bn – remains in the overall economy.4

- A resilient US economy.

- Significant US student debt relief over the last couple of years – albeit that interest resumes on student loans on 1 September this year with payments due the following month.

Outlook: tying up loose ends

All the evidence points to a ‘soft landing’ in the US and a subdued default cycle.

Nonetheless, most financial institutions have used the benign economic conditions of 2023 to date to shore-up loan reserves in case rainy days lie ahead, foreshadowed by risks on the horizon such as:

- Credit normalisation – for example, anecdotal evidence suggests OMF began tightening its lending criteria in Q2 2022, reducing the weighted average life of loan instalments to about a year, in moves that should shift the portfolio credit quality to the higher end this year.

- Higher interest rates.

- Margin compression for lenders as depositors demand higher rates.

For all its elegant mathematical modelling, string theory has yet to deliver an evidence-based example of its existence in the real world – and it may never do so.

Fixed income investors, meanwhile, betting on a novel, painless lending cycle might likewise want to probe the theory a little deeper; the long history of debt markets suggests that if credit is pulled too tight, something invariably breaks.

Richard Feynman (1918-1988), theoretical physicist and Nobel laureate.