Stripped down to the basics, life on Earth offers local respite from the universal, inexorable drift towards entropy by using information to create order from chaos for the price of energy.

The anti-entropy trick in all living cells relies on three key molecules that orchestrate, implement, and fuel an intricate, ingenious cycle:

- deoxyribonucleic acid, better-known as DNA, to govern the process.

- proteins that translate orders into action; and,

- adenosine triphosphate – or ATP, the highly efficient power storage and exchange mechanism often described as the cellular ‘energy currency’.

In fact, ATP dances a delicate pas de deux with sister molecule, adenosine diphosphate (ADP), to capture and release life-giving energy via a continual cycle of merger and separation as below:

Figure 1: The structure of ATP

The structure of ATP is a nucleoside triphosphate, consisting of a nitrogenous base (adenine), a ribose sugar, and three serially-bonded phosphate groups.

Waiting for the spark

Banking is where risk meets regulation.

Governed by rules that have evolved over hundreds of years of trial and error, banks distribute credit across the economy in a system designed to keep financial chaos at bay.

But just as DNA is a useless chain of chemicals without efficient molecular intermediaries and energy-replenishing processes, edicts from Brussels and Frankfurt alone cannot spark life in a complacent banking industry.

Historically, merger and acquisition (M&A) activity has been an important re-energising source for the commercial bank sector, allowing stronger institutions to absorb weaker rivals or for equals to create a whole that is greater than the sum of its parts.

At its best, M&A drives efficiencies, innovation, better risk management and higher profits that benefit consumers, shareholders, and the wider economy alike.

It’s no secret, though, that the European banking system remains highly balkanised, more than 10 years after the European Central Bank (ECB) launched its own Asset Quality Review.

The vision of a banking union providing free movement of capital and liquidity across the region, facilitated by trans-continental institutions, remains very much in embryo phase.

Former ECB boss, Mario Draghi, said as much in his EU revival report published this September, identifying telco and bank sector reforms as critical to livening up competition in the region.

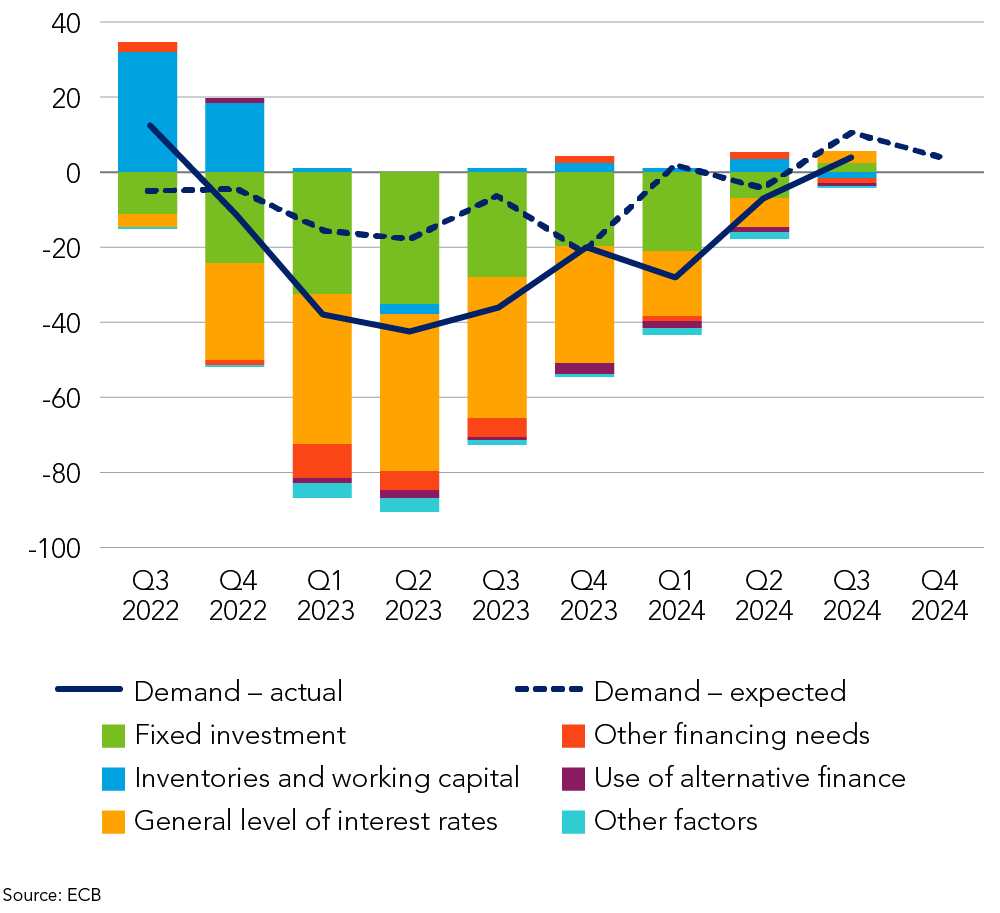

Yet it is more likely that savvy management teams within institutions will inject life into the EU banking system through smart M&A moves rather than political calls for innovation – especially amid the current period of insipid loan growth (see Figure 2).

Figure 2: Changes in demand for loans or credit lines to enterprises, and contributing factors

Vital signs improve

Virtually all EU banks are, as we speak, scouring every balance sheet line in search of opportunities to improve their cost-to-income ratios to meet return-on-equity (ROE) targets in an increasingly competitive environment.

Lenders typically tend to fall shy of strict ROE requirements through the combination of higher fixed costs and weaker revenues per mix of assets.

M&A has proven to be a useful lifeline for low-energy banks.

Domestic bank mergers, for example, can help the combined institutions achieve economic scale and increase market share.

By contrast, cost-savings and revenue-synergies in cross-border banking unions are more difficult to come by – and harder to sell to investors.

Incentives, however, are on the table that could trigger a new round of trans-EU merger-mania among banks in the region.

From higher-value acquirers booking profits on day one through the monetisation of ‘badwill’ in takeover targets, to improving regulatory capital positions, EU banks stand to gain much from well-planned multi-country mergers.

Most recently, a Basel III amendment allowing banks a more favourable Common Equity Tier 1 (CET1) risk-weight for insurance company holdings, looks set to boost M&A activity.

Under the so-called ‘Danish compromise’, bank equity in insurers will carry a CET1 risk-weighting of 250% compared to the original 370% – a very beneficial boost to those institutions with large operations and low risk-weight density.

Meanwhile in the UK, the Bank of England has proposed to formalise a transitional Minimum Requirement for Own Funds and Eligible Liabilities (MREL) grandfathering provision it granted in the recent Nationwide buyout of Virgin Money: if adopted, the proposal would support smaller banks looking at M&A opportunities.

More generally, as central banks continue to ease rates the profit-streams flowing from insurance, investment banking, asset management and wealth management will be valued at higher multiples by the stock market – potentially encouraging banks to buy such adjacent businesses to offset lower net interest income profits and breathe new life into the long-dead ‘bancassurance’ model.

With up to €600bn of net interest income at risk based on current EURIBOR forward curve projections, the pressure is mounting on European bank management teams to deliver on cost-savings soon… in that context, M&A is very much a live option.

Conclusion

DNA is the plan for life that depends on, and adapts to, a series of intermediary molecules and the energy-giving feedback loop of the ATP-ADP cycle for successful implementation.

Banking is also a dynamic process where the vitality of the system as whole depends as much on bottom-up innovation as much as top-down regulation.

After a long dormant period, it seems a renewed M&A energy is again coursing through EU banks, sparked into life, perhaps, by a determined management team in Italy ready to show where a plan meets action.

Richard Dawkins, evolutionary biologist, The Selfish Gene, 1976.

Dawkins later regretted the title of his book, noting that many readers failed to see ‘selfish’ was being used metaphorically.

BD014827