Lending protections are eroding in Europe: cov-lite loans are now the norm in the large-cap loan segment, while cov-loose loans and add-backs to EBITDA are gaining ground in mid-market deals. Today, we explore the implications of loosening covenants and explain why we avoid these instruments, focusing instead on mid-market deals, which are governed by more robust loan documentation and offer attractive returns under strict risk controls.

Navigating the new normal

Last month, Bank of England governor Mark Carney sounded the alarm about the deterioration in lending standards1. He joins the US Federal Reserve, the International Monetary Fund and the Bank for International Settlements in decrying the leveraged loan market.

Why the concern?

In recent years, the leveraged-loan market has become increasingly competitive: strong inflows of capital into private debt funds and collateralised loan obligations, along with improving bank balance sheets, have driven demand for loans higher – particularly in the more easily accessible large-cap segment of the market, which consists of loans to companies with EBITDA in excess of €75m.

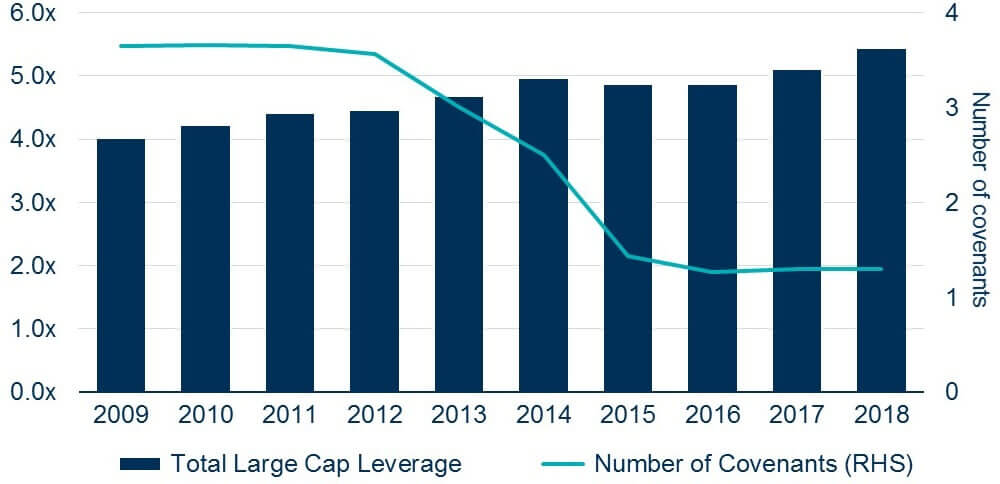

In this environment, lenders have competed by offering borrowers higher leverage levels and looser loan terms. Over the last three years, the level of total leverage in the large-cap market has gradually inched higher, from 4.8x to 5.4x2. There was however some reprieve: the average proportion of equity contributed by private-equity owners – which acts as a cushion behind debt in the capital structure – has remained stable at about 50% over the same time period (compared to a love of 34% in 2007)3.

But beneath this lies an unsettling trend: in order to compete, lenders have been forfeiting protections in the underlying documentation that governs a loan (see Figure 1). This has resulted in:

- a surge in so-called cov-lite loans – senior loans that do not provide lenders with the safety of regularly recurring maintenance covenant tests;

- the loosening of covenant headroom (where a covenant has been present); and

- the inclusion of increasingly flexible add-backs in the EBITDA number that is used to calculate leverage (the ratio of debt-to EBITDA).

Figure 1. Protection erosion in the large-cap market

Source: S&P Global Market Intelligence as at Q4 2018.

Recap: what are maintenance covenants?

Until 2013, it was standard practice to include a maintenance covenant package in loan documentation. Borrowers had to satisfy quarterly recurring financial tests, known as maintenance covenants – consisting of debt-to-EBITDA, interest-to-EBITDA and cash-to-debt-service financial ratios. Using management’s forecasts as a base, a headroom level of about 25-30% was applied to these ratios to generate the covenant test. Failure to satisfy any of these tests would constitute a default on the loan.

- Maintenance covenants, which are set at a sensible headroom level, play a very important role in protecting investors. They:

- act as an early-warning system if a borrower’s trading performance declines

- provide lenders with an opportunity to take protective actions before diminishing corporate performance and enterprise value threaten the recovery of the loan

Without them, lenders may be unable to take any action until the borrower’s financial condition has eroded to the point of default – or in extreme instances, impairment – where the value of the loan exceeds the value of the borrower.

Cov-lite loans and beyond

Cov-lite loans are governed by documentation that does not include any maintenance covenants. Instead, they contain incurrence covenants, which offer far less protection to lenders. Incurrence covenants are tested solely upon the occurrence of pre-agreed events, such as a material drawdown on a revolving credit facility or the payment of a dividend, rather than on an automatically recurring basis. This means that borrowers can easily avoid financial ratio tests by not taking the specific actions which trigger them.

In contrast, cov-loose loans have at least one maintenance covenant, usually debt-to-EBITDA. The headroom level set on the covenant test – that is, the point at which the borrower’s earnings would have to degrade to trigger a default – is set so wide that by the time a covenant breach occurs, lenders have already missed the opportunity to engage with the borrow to try to remedy the underlying issue and maximise recovery on the loan. For such a transaction, a direct lender can purport that they avoid cov-lite loans, when in fact they do not. Investors must therefore tread with caution and ask direct lenders: what is the average level of covenant headroom of loans in your portfolio? Finding out will help investors ensure that they have adequate protections.

The value of maintenance covenants

Maintenance covenants give lenders strong negotiating powers, forcing an early discussion with management, as soon as trading performance declines and usually before there are any liquidity problems. In such circumstances, the options available to lenders can include:

- Increasing the yield of the loan to reflect the increased risk

- Requiring the borrower to prioritise cash generation over corporate expansion in order to pay down the loan

- Requiring the borrower to sell business divisions or assets to pay down the loan

- In a worst-case scenario, enforcing the security provided in the loan documentation to take ownership of the business

Conversely, in cov-loose deal structures, the warning signal is likely to be triggered when it is too late. Worse still, there is no automatic early-warning trigger in a cov-lite deal structure.

Under these two deal structures, a default may not occur until a very late stage in the decline of the business’s performance, possibly when the borrower encounters difficulty making an interest payment or scheduled repayment on its loan. This could be symptomatic of a near-insolvent borrower with significant liquidity problems. There are two key implications for lenders in such a scenario:

- They may have to support the borrower with emergency capital to keep it afloat, layering more debt into the capital structure and possibly subordinating the original senior debt.

- The borrower’s enterprise value may have fallen considerably before the default occurs, materially impairing the loan before lenders have any right to take protective actions.

Worsening lending protections

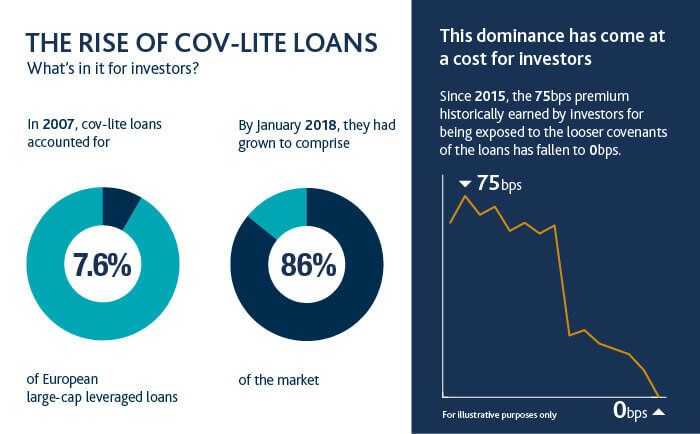

Despite the weaker lending protections, cov-lite loans do not offer greater potential returns. Historically, large-cap cov-lite loans were priced at a premium of up to 75bps4 relative to covenant loans, but this premium was eroded during 2016 and 2017, when cov-lite deals became more prevalent (see Figure 2). Since Q1 2017, the average yield-to-maturity of large-cap, single-B-rated cov-lite loans has declined to that of their equivalent covenanted deals5.

Figure 2. The rise of cov-lite loans: what’s in it for investors?

Source: Hermes and LCD as at May 20176.

Indeed, the overall ability of investors to recover value from defaulting cov-lite loans has yet to be properly tested through an entire economic cycle. However, a comparison of recovery rates between senior loans (both covenanted and cov-lite) and first-lien secured bonds (which are entirely cov-lite) from 2003-2016 might provide some insight: the average recoveries on loans was 74% versus 52% on secured bonds. This may be informative but cannot be categorically linked to the presence or lack of maintenance covenants given the other differences in the instruments7.

EBITDA add-backs in the spotlight

The proliferation of upward adjustments to a borrower’s earnings have also been flagged as a danger by the Bank of England’s Financial Policy Committee8. Known as EBITDA add-backs, they have long been present in loan documentation. In the past, examples included a contract win with committed future revenue, whereby earnings were adjusted upwards to account for the guaranteed future achievable revenues.

Much has changed in recent years: add-backs have become increasingly stretched in terms of quantum, definition and period of achievability. Today, for example, savings that are expected from company initiatives that will be implemented in the next 18 months or synergies to be achieved in the next two years from the integration of a new acquisition or a corporate structuring are added back to earnings. What’s more, these numbers can be very subjective.

It is therefore possible to overestimate the upside from loosely-defined future activities. Indeed, overstating earnings can have adverse impacts, such as:

- The debt-to-EBITDA ratio – that is, leverage levels – will be understated

- A borrower’s real earnings may not be sufficient to fully service the interest and debt repayments on the level of debt provided by lenders

If EBITDA – used in the loan documentation to calculate covenant levels – is overinflated, the financial test ratios will be looser, and their ability to act as an early warning trigger may prove to be ineffective

At present, mid-market lenders exert some control over the level of EBITDA add-backs: in general, they have to be certified by the borrower’s chief financial officer or auditors, depending on the level proposed. Alternatively, lenders can impose a cap on the level permitted to be added-back.

Focus on covenanted mid-market deals

We consider effective maintenance covenants to be an essential protection for lenders, so we never lend on cov-lite terms. By focusing on the mid-market – which consists of loans to companies generating €5m-€75m of EBITDA each year – we are targeting the part of the leveraged lending market where cov-lite has failed to gain ground. This market is dominated by heavily regulated, conservative corporate and commercial banks, which require loans to have maintenance covenants, set at meaningful headroom levels. In addition, mid-market companies are not large enough to access alternative sources of finance through the bond market, which is characterised by looser documentation.

In our view, the mid-market offers investors a more attractive and sustainable balance between risk and reward. It provides better downside protection than the large-cap market due to maintenance covenants being a standard feature of loan documentation, as well as providing a material illiquidity premium.

A question of selectivity

Investors need to be aware of the difference in downside risk between cov-lite, cov-loose and covenanted senior loans. While all three types of loans provide lenders with first-lien security over the borrower’s assets and operations, the time at which that security can be enforced through a loan default could differ materially.

In addition, investors must question direct lenders about the underlying protections in their loan portfolios, including getting a better understanding of how covenants are set. This will not only increase their understanding of the risk-reward profile different lenders offer, but it will also force direct lenders to achieve better terms, which in turn could boost lending protections.

At Hermes, we do not want to expose our investors to the risks presented by cov-lite and cov-loose deals. Instead, we invest exclusively in loans governed by meaningful covenants, found primarily in the mid-market segment where EBITDA add-backs are more effectively controlled. This is where we believe the most attractive returns for direct lenders in Europe are to be found.

The views and opinions contained herein are those of Laura Vaughan, Head of Direct Lending, and may not necessarily represent views expressed or reflected in other Hermes communications, strategies or products. This commentary is published solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments.

1 Carney raises pressure on leveraged loans,” published by Reuters on 21 January 2019

2 Europe LBO 2018 4Q” published by LCD News in Q4 2018.

7 2016 Annual Study of European Corporate Recoveries: The Highest Recovery Rate Since 2007, published by S&P Global RatingsDirect on 12 June 2017