The next generation: balancing conservatism versus flexibility in the world of CLOs

Financial markets have an uncanny ability to innovate and reinvent themselves.

Despite an absence of meaningful losses and defaults, such innovation was evident in the European CLO market after the financial crisis. The focus here lay on structures and documentation, which translated into a market morphing from CLO 1.0 to CLO 2.0. As a result, CLO debt investors benefited from greater loss absorption, as the capital structure and documentation of the later generation of CLOs is more conservative. Meanwhile, managers gained some flexibility to optimise the lifetime cost of the liabilities.

Changes in Europe included:

- Less structural leverage: equity cheques increased from 7% to 10%

- A more conservative approach from rating agencies: what was rated ‘AA’ pre-crisis would be rated ‘A’ today, due to credit enhancement

- More restrictions on asset holdings and the prohibition of CLO-squared: CLOs no longer investing in other CLOs

- Realignment of maturities: CLOs can no longer buy assets maturing after the CLO’s maturity

- Greater ability and flexibility to manage CLO liabilities: Deals can be refinanced, re-set or re-issued in order to align liabilities with current market conditions

But where an investor in a CLO’s debt will favour predictability and conservative practices, an equity holder will seek to maximise gains. The documentation associated with CLOs is therefore constructed in a balanced way to allow a manager the flexibility to add value to the equity and make substitutions to buffer the debt stack from losses.

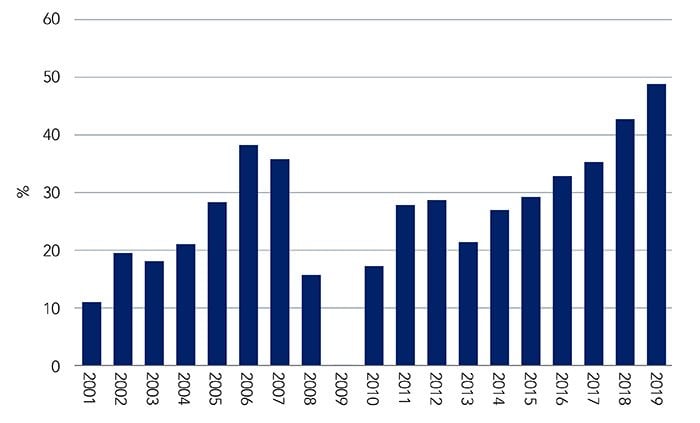

And while some boundaries are used to constrain the manager to permissible behaviour, such boundaries sometimes need to be revisited in order to strengthen the position of CLOs. In the CLO 1.0 world, it was believed that a deal would benefit from preventing CLO managers from dabbling too much in distressed credits – hence, the manager’s ability to hold restructured debt and equity was negligible. By the time defaults started in earnest during the financial crisis, it became clear that astute participants in the distressed market understood how to maximise their returns potential by taking advantage of the forced sellers in the CLO market, an ever growing part of the leveraged loan investor base (see Figure 1).

Figure 1. Primary market share of CLO managers (2001-2019)

Source: LCD, an offering of S&P Global Market Intelligence, as at Q3 2020.

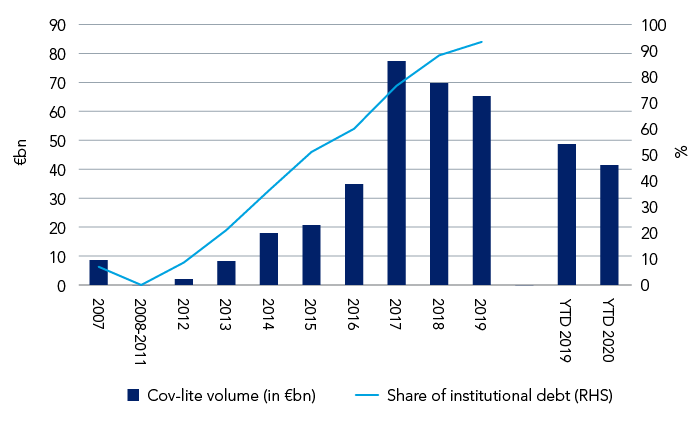

As a result of this experience, managers in the CLO 2.0 world are now looking to protect both their equity and debt investors by increasing their arsenal of responses to distressed credits, thereby preventing predatory buyers from scooping up bargains. As Covid-19 continues to disrupt the global economy and affect many sectors and companies, the possibility of credit deterioration must be addressed. Covenant-lite loans (cov-lites) reached over 80% of issuance last year (see Figure 2), meaning there will likely be a delay in defaults and more restructurings on the way.

Figure 2. annual volume and institutional share of cov-lite issuance (2007-2020)

Source: LCD, an offering of S&P Global Market Intelligence, as at Q3 2020.

CLO 2.0 documentation and the fight to preserve value in a deteriorating credit environment

So, what could a CLO manager do to preserve value in a deteriorating credit environment? In CLO 2.0 documentation, investors will commonly find the following tools:

- Ability to invest in “Restructured Obligations”, as long as the obligation was not classed as “Default” or “Credit Impaired” at the time of purchase (unless the CLO is at its warehouse stage, in which case the manager needs to sell the obligation). This allows a CLO to hold the resulting debt from a workout situation, which in turn means they are not a forced seller in a restructuring.

- Ability to invest in “Corporate Rescue Loans,” which are a European version of a DIP facility (Debtor-in-Possession). In the US, only companies that have filed for bankruptcy protection under Chapter 11 can access DIP financing. Managers can usually invest up to 5% of the portfolio in these products and invest new money (i.e. the CLO doesn’t have to be invested in the initial loan). This allows a CLO to invest in new debt that will facilitate a restructuring and is usually more senior in ranking to the previous instruments issued.

- Ability to hold “Exchanged Equity Securities”, as part of the restructuring process. This will not affect the overcollateralization tests.

- Ability to invest in “Collateral Enhancement Obligations,” which amounts to any warrant or equity security ─ excluding “Exchanged Equity Securities” ─ including any equity received upon conversion or exchange of an option. Again, these exposures will not be included in the collateral and will not affect the overcollateralization.

These features help the manager to participate in restructurings. Additionally, the language used in CLO 2.0 documentation supports the overcollateralization buffer, as restructured obligations and corporate rescue loans aren’t considered as “Default Obligations”. As a reminder, in the calculation of the “Adjusted Collateral Principal Amount”, defaulted obligations are included at the lowest rating agency recovery value (rather than par).

Investors could argue that these tools are reasonable and help managers to avoid “forced sales”. Certainly, we have seen situations where the mechanism worked perfectly, gave managers respite, and helped them to avoid par losses. We analyse restructuring and distress capabilities in our review of CLO managers to determine how much we expect these features to be utilised and where they will add value.

Open to interpretation? The pros and cons of flexibility in CLO documentation

Many innovations in CLOs are developed in the US market and are subsequently imported into European deals. Since September 2020, there has been a surge of new tools in CLO documentation, some of which we believe can be beneficial to debt investors in the right hands.

These include “Loss Mitigation Loans and Workout Obligations”, which benefit the manager by allowing new money to be invested in a collateral obligation issued as part of a restructuring. There are no eligibility criteria, but the loan must be acquired in connection with such a restructuring or, if deemed necessary, enhance/protect the recovery value of the collateral obligation prior to the restructuring. We believe this feature takes positive steps to combat workout plans that do not allow CLOs participation in future upside.

However, other structural or definitional clauses seem to allow the manager too much leeway and could, potentially, result in further cash flow going to the equity without commensurate reward to the debt stack.

One such example is “Exchange Transactions,” which give the manager the ability to exchange any defaulted obligation for another defaulted, or sometimes credit impaired, obligation. There are limited eligibility criteria, but some seem subjective, such as (i) the new defaulted obligation needs to have a better likelihood of recovery, or (ii) the forecasted IRR of the new obligation should exceed that of the old obligation.

Another example is the “Reclassification of Collateral Enhancement Obligations,” which give the manager the ability to classify an asset that has defaulted as a “Collateral Enhancement Obligation”. The transfer is made on a market value basis (which can sometimes be subjective in a special situation) and could result in a pick-up of value for the CLO versus the recovery value applied by the rating agencies. Typically, this mechanism allows the equity holder to buy the asset from the deal. From the CLO’s point of view, this is no different than selling to a third-party, except that it reduces transparency around the market-clearing price of the position. It also benefits the CLO’s equity holder, in that the transaction becomes custodian of the distressed asset.

But for deals to exist, there needs to be an incentive for equity providers to be involved, and these investors expect returns that come not only from the leverage inherent in a CLO, but also from the added value created by a manager.

We, as debt investors, also rely on a manager’s ability to “create alpha”, but not to the detriment of debt holders. So while we want to promote deals with the right balance of incentives and flexibility, we also need to pay close attention to how managers intend to use this flexibility, understand their philosophy and verify that their past behaviour corroborates their stated strategy.

How is our due diligence process taking stock of documentation changes?

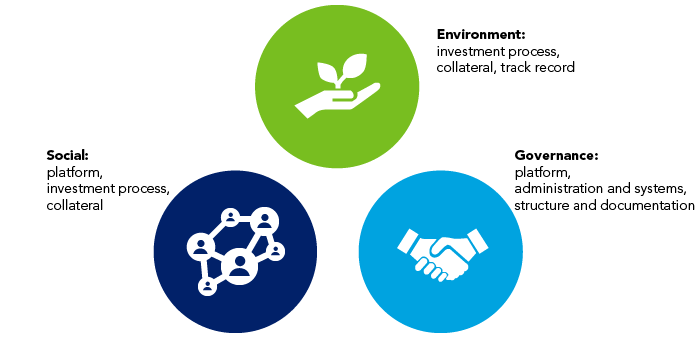

At the international business of Federated Hermes, we have multiple layers of analysis in our due diligence framework, which cover the manager’s platform and investment process, their track record and style, and their underlying portfolio of loans (see Figure 3). More importantly, we care deeply about ESG and believe that the new features of CLO documentation that we have discussed here have a strong impact on the methodology we employ, and the conclusions we are able to make. In particular, documentation analysis impacts the “Governance” score we assign to transactions.

Figure 3. The due diligence framework employed by the international business of Federated Hermes

Source: Federated Hermes, as at February 2020.

Greater flexibility for managers is a positive, but only if it benefits equity and debt holders alike

For us, this new legal framework raises three questions:

- To what extent should CLOs be flexible? In our view, CLOs should predominantly focus on performing loans and continue to support banking disintermediation. Managers should be able to participate in restructurings to avoid par losses, but CLOs are not meant to act as distressed funds. We also believe managers need to demonstrate that they have the requisite restructuring skills in-house to deliver additional value from the added flexibility discussed above.

- Will the price of liability and cost of debt be affected? It will be important to monitor the relative value between deals with limited flexibility to invest in special situations and deals with more aggressive language. We think investors should be paid more to invest in CLOs that are exposed to a greater number of non-performing loans.

- Who will benefit from such documentation? CLO managers holding their own equity could see an incentive to participate in restructurings to boost their performance. Equally, deals with third party equity investors (i.e. not the CLO manager) are motivated to meet ambitious IRR targets to generate performance fees and for future marketing purposes. Not all managers will have the requisite expertise to maximise returns from such a process, and to the extent that they are not arbitraged by distressed investors, we would prefer CLO managers to focus on performing loans.

One of the characteristics of structured finance is its inventiveness. It is what makes the product so unique and attractive, but it also means that investment professionals need to contextualise innovation, accept its benefits and push back against undesirable features.

While we support tools that enhance managers’ flexibility to protect our investments, especially as deals will be exposed to more difficult economic conditions, we do not embrace uniformly some recent attempts to extract value from distressed situations skewed to the benefit of equity holders.

Structured credit at the international business of Federated Hermes

We have a fundamental credit focus that is supported by our unique ESG analytics in structured credit.

We have been active investors in the structured credit asset class since before the global financial crisis. With experience in managing a wide range of underlying asset types, we take advantage of investment opportunities from across the structured credit asset class, and employs a rigorous, relative value framework to contextualise risks and returns. We also leverage the expertise of the wider Fixed Income team to gain a holistic understanding of securitisation transactions, as well as the drivers of markets and sectors. We manage structured credit in a number of multi-asset credit portfolios.

As pioneers of ESG investing, we leverage the vast resources of the firm and apply sector-specific expertise to integrate ESG criteria into our investment approach. Alongside our dedicated fixed income engagers and our stewardship team, EOS at Federated Hermes, we seek to drive positive progress in relation to disclosures and issuer behaviour in the asset class.

Share:

Risk profile

- Past performance is not a reliable indicator of future results.

- The value of investments and income from them may go down as well as up, and you may not get back the original amount invested.

- This information does not constitute a solicitation or offer to any person to buy or sell any related securities or financial instruments.