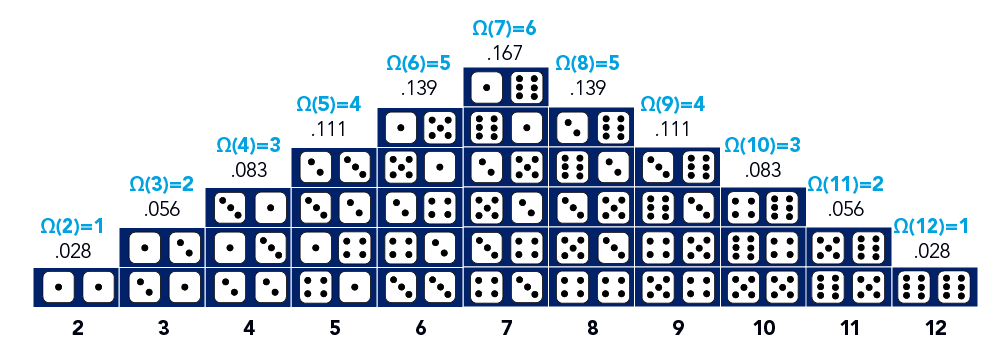

God does not play dice with the universe, according to Einstein, but, if he did, the outcome would look something like the chart below – only with somewhere between a vigintillion and acentillion of different particles to rearrange instead of two, six-sided die.

Chart 1: Towards entropy

The double-die example (as opposed to a universe of some 3.28 x 1080 particles) offers an easy-to-grasp image of entropy as a combination of all possible ‘microstates’ within a closed system to form a ‘macrostate’ as described by a probability distribution of outcomes.1

Ludwig Boltzmann, the ahead-of-his-time 19th century Austrian physicist, was the first to formalise entropy as a probabilistic measure of states in his now iconic formula: S=k log W.

Under the notation: S stands for the entropy of a given system; k is ‘Boltzmann’s constant’ – a number that relates energy and temperature; and W equals the number of microstates within the macrostate in question.

Essentially, the equation measures the number of possible ways to arrange the pieces of a system such that the overall picture doesn’t change. In a closed system – ie one where no new energy is added – entropy (disorder) increases as per the, somewhat depressing, Second Law of Thermodynamics.

The entropy of QT

While its variables might be harder to pin down than for dice, the global financial universe – and, in particular, the US dollar-denominated system – can also be described as a macrostate with microstate, whose components include:

- The Federal Reserve-determined repo rate;

- Banks;

- Money market funds (MMF); and,

- Collateral etc.

As the ‘prime mover’ in the US-centric financial system, the Fed plays an oversize role in rearranging the microstates through multiple policy levers such as setting the repo rate or adjusting money supply via so-called quantitative easing (QE) in the aftermath of the Global Financial Crisis – a process the central bank (along with monetary authorities in other jurisdictions) is now trying to reverse through quantitative tightening (QT).

The Fed began its latest QT efforts in June 2022 (after abandoning a previous attempt in 2018 due to market pushback), looking to slowly reduce its balance sheet that had been bloated by huge bond purchases made to keep the financial system afloat during the Covid-19 pandemic.

If QT proves successful in ‘sterilising’ the excesses of QE, this could have an enormous impact on monetary policy theory and practice: balance-sheet expansion and contraction may emerge as a staple, financial crisis-fighting tool for central banks rather than a one-off, desperate experiment to avert disaster.

However, in tinkering with the financial microstates, the Fed runs the risk of increasing the entropy – Boltzmann’s ‘S’ – of the system as a whole: which can be viewed as either skewing the odds to a particular outcome or creating more disorder.

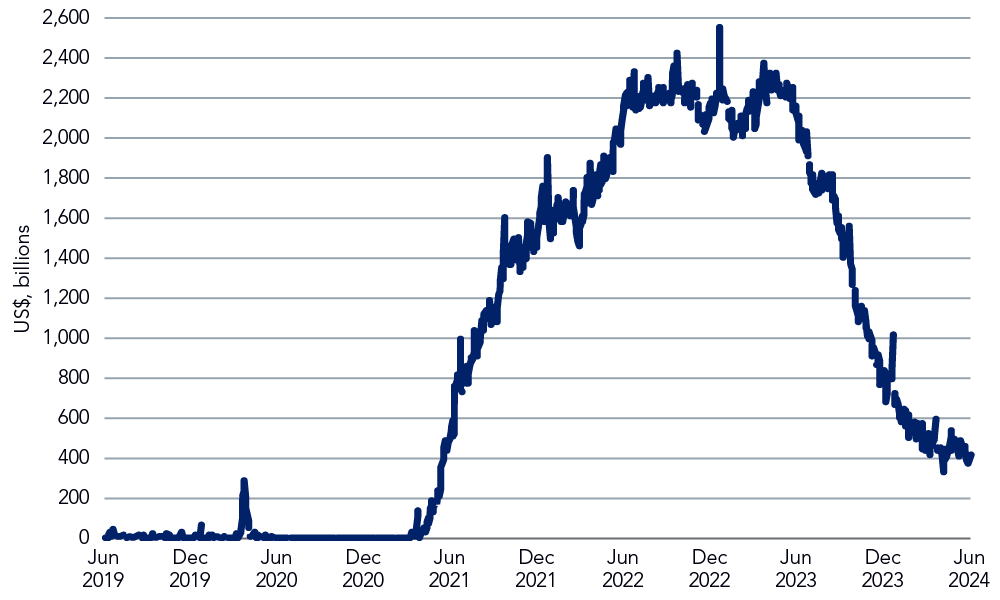

Reverse-repo: mop-up or spill-over?

The Fed rolled out the reverse-repurchase agreement (RRP or reverse-repo) for the first time in 2013 as a new-fangled financial device to mop-up excess reserves, some of which were created during the QE era.

Importantly, the reverse-repo facility is the only non-reserve liability on which the Fed pays interest. The RRP allows the Fed to absorb excess liquidity held by money market funds (MMF), government-sponsored entities (GSEs), and primary dealers.

Under normal circumstances such excess reserves don’t earn interest but the reverse-repo magic sees the counterparties ‘lend’ cash to the central bank overnight, collateralised against Treasuries in the Fed’s securities portfolio.

One important feature of the RRP rate is that it is meant to set a floor under all market rates.

Every day the New York Fed carries out repo and reverse repo operations to keep the federal funds rate in the target range set by the Federal Open Market Committee, covering: all repo and reverse repo operations conducted, including ‘small value exercises’ (market test runs, in effect).

As the chart below reveals2, 3, the reverse-repo market has been on quite a ride since early 2021.

Chart 2: Treasury Securities sold by the Federal Reserve in temporary open market operations

Clearly, the RRP has served as a ‘risk-free’ safe harbour in recent times.

But a 2015 paper written by Fabio Natalucci – now at the International Monetary Fund – and colleagues at the New York Fed, highlights some risks posed by the RRP as investors ‘fly to quality’ during market volatility: at the time, those concerns were brushed aside.

Now almost 10 years down the track, we can see the dampening effect on lending – and possibly the wider economy – with the sharply higher reverse-repo rates transmitting immediately to MMFs, in particular, but only slowly to bank depositors.

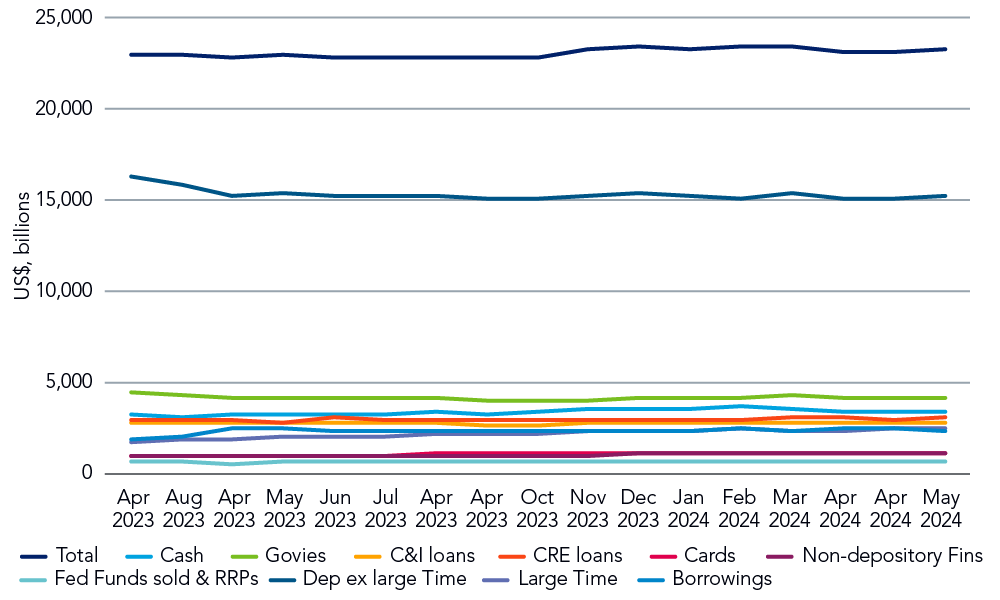

Banks now have abundant reserves. Thanks to the RRP, banks have operated with defensive cash positions since the onset of the regional banking crisis in March 2023.

Chart 3: Evolution of selected A & L of US banks

With investors increasingly shifting funds from low interest-bearing deposits to higher-yielding options (notably, MMFs), bank net interest margins have come under pressure while also reducing the availability of cost-effective funding for new loans.

Instead of expanding their lending books – and helping the economy grow – US banks have been focused on remixing maturing assets to manage yields higher.

Order rolls on

The Fed does not play dice with the financial system.

But with innovations from QE to QT and RRP, the US central bank has shown a willingness to experiment to keep the system in a balanced state. Of course, rearranging the microstates will impact the overall macrostate – as entropy theory implies and the practical experience of RRP reveals.

Is more disorder the most likely outcome? Perhaps we don’t need to despair.

As witnessed in the wake of the regional bank ‘mini run’ in March 2023, the US central bank is ready to move quickly and create new tools to ring-fence problems: it might not be able to fight entropy but the Fed won’t tolerate chaos.

Nobel-prize physicist Richard Feynman (1918-1988) musing.

Learn more about the views of our credit team in our Q2 360° report.