Impact theme: Energy Transition

In 2018, the Intergovernmental Panel on Climate Change (IPCC) found that limiting global warming to 1.5°C would require a 45% reduction in global greenhouse gas (GHG) emissions by 20301.

At an average cost of $44/MWh, wind is on a par with solar power as one of the cheapest alternatives to fossil fuel. Turbine manufacturers account for the majority of costs associated with onshore wind, and there are surprisingly few in the business. Compared to the plethora of contractors involved in installation and site management, the onshore wind equipment market is dominated by three key players2.

Our holding – Vestas – is one such manufacturer. The company is the largest global supplier of onshore wind turbines, with an 18.1% market share in 20193.

Making wind power more accessible

Vestas is focused entirely on wind turbines: 84% of the company’s revenue is from the sale of wind turbines and blades, with 16% derived from servicing this equipment4.

Two things are particularly encouraging about Vestas’ product and service offering. First, Vestas’ 4MW platform accommodates a broad range of wind and site conditions, allowing users to mix turbines across various sites. Not only is this kind of solution becoming ever more popular as it delivers superior energy production5, Vestas also remains the supplier of choice, commanding over 50% of the product segment (ex. China)6.

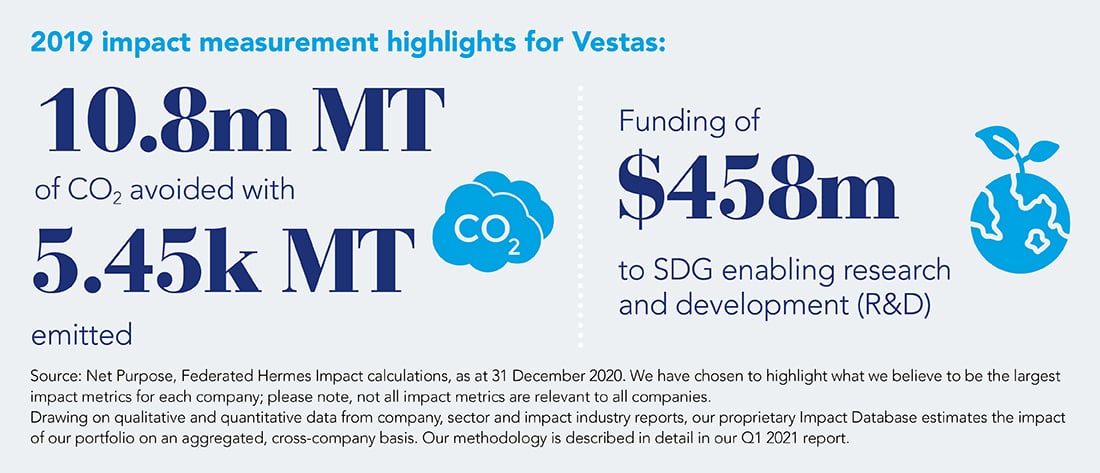

Targeting ‘zero-waste’ turbines

Vestas’ production chain does have a somewhat negative impact, although this is more than offset by the company’s product offering. While Vestas emitted 5.4k MT of CO2 (Scope 1 and 2) in 2019, for example, the company’s wind turbines helped displace around 10.8m MT of CO27.

Vestas disclose production inputs in their Sustainability Report, alongside targets. Encouragingly, the company have pledged to cut their operational emissions by 45% come 2030, with the production of ‘zero-waste’ turbines earmarked for 20408.

We believe the company’s impact to be scalable with the sale of more turbines, which will continue to displace CO2 intensive energy sources in years to come.

1 Relative to 2010 levels (Source: IPCC, Summary for Policymakers)

2 Excludes China.

6 Source: Bloomberg, in reference to FY 2020 market sizing.