Everything is connected.

Well it might be, but only armchair philosophers can leave that statement hanging unsupported in the ether as a universal fact. The job of scientists, and financial analysts for that matter, is to show how things are connected rather than assert relationships are real without providing evidence.

And sometimes the evidence leads scientists, and investors, into strange, contradictory places. In the early 20th century, for instance, the then emerging field of quantum mechanics (QM) spun off in a weird direction after Albert Einstein first floated the idea that would become known as ‘entanglement’.

Einstein arrived at entanglement, which he dubbed “spooky action at a distance”1, in a ‘thought experiment’ designed to settle an argument with proponents of a QM model that implied a somewhat random, probablistic universe.

Along with physicist colleagues Boris Podolsky and Nathan Rosen, Einstein formalised the point in a paper theorising that if the QM worldview is correct, then two particles could become ‘entangled’, allowing the observation of values (such as direction of momentum) of one particle to automatically assign a certain value to the other particle even if they were on opposite sides of the universe.

The EPR (named after the last initials of the three scientists who authored the paper) conclusion violated two key assumptions of physics as understood then:

- realism – or the concept that objects possess properties separate of any external observer; and,

- locality – the idea that the measurement of one object can’t affect the measured values of another far-away object.

“No reasonable definition of reality could permit this,” Einstein said at the time2.

But reasonableness in physics has since proven to be a relative quality. Instead of restoring the pre-QM notion that “God does not play dice with universe” as Einstein hoped, EPR set in motion a multi-decade scientific effort that has instead established entanglement as a real – if still poorly understood – phenomenon.

As a 2017 Cosmos article notes: “Entanglement is no longer a philosophical curio: not only are physicists using it to encrypt information and relying on it to underpin the design of tomorrow’s quantum computers, they are once again grappling with the hard questions about the nature of reality that entanglement raises.”3

Out of the mix: unemployment and consumer lending lose touch

Meanwhile, after a decade or more of disruptive monetary policies, investors are facing similar challenges to long-held views about the nature of markets and the relationships between underlying causal factors.

For example, exactly a year ago we studied the health of the US consumer as viewed through the historically entangled data points of unemployment and loan performance of two companies in our credit portfolios.

Using the well-established net charge-off ratio (as the percentage average loans outstanding) as a proxy for default risk, we tracked two US non-prime lenders – Ally Financial and OnMain Financial (OMF) – across the unemployment/credit quality continuum for more than a decade. While both companies play in the riskier lending sector, Ally features a higher proportion of near-prime loans compared to OMF, which leans more to sub-prime.

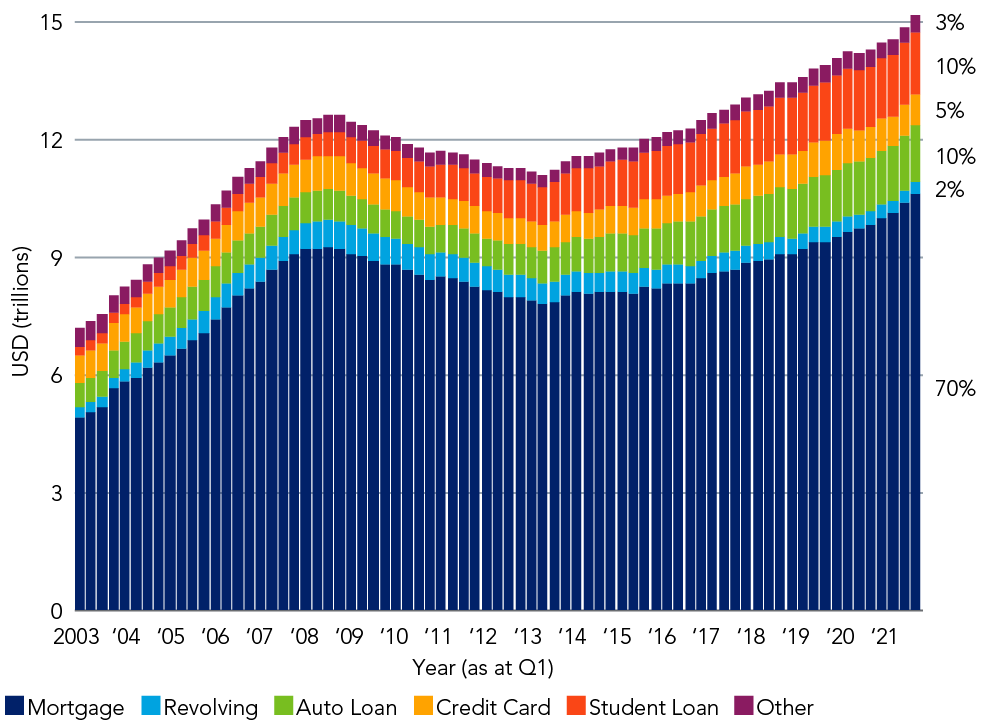

As the graph below reveals, since our 2020 analysis overall US consumer debt has ballooned to almost $15.3tn – a cool trillion dollars more in the space of 12 months.

Figure 1. Total debt balance, including composition

Source: New York Fed Consumer Credit Panel/Equifax

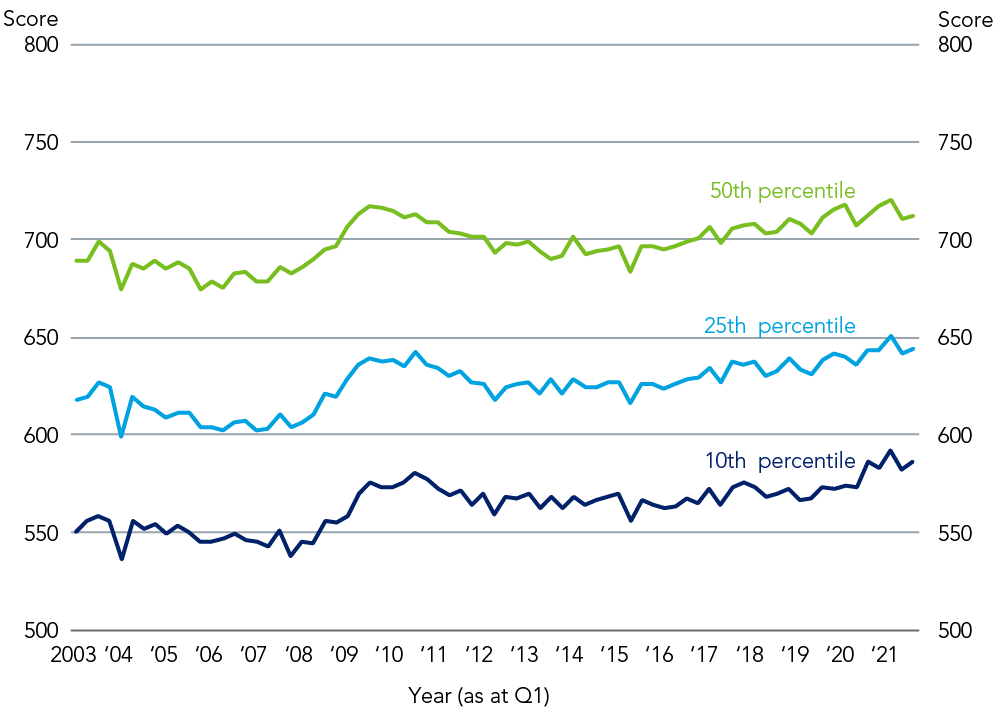

Figure 2. Credit score at origination: auto loans*

Source: New York Fed Consumer Credit Panel/Equifax

* Credit Score is Equifax Riskscore 3.0

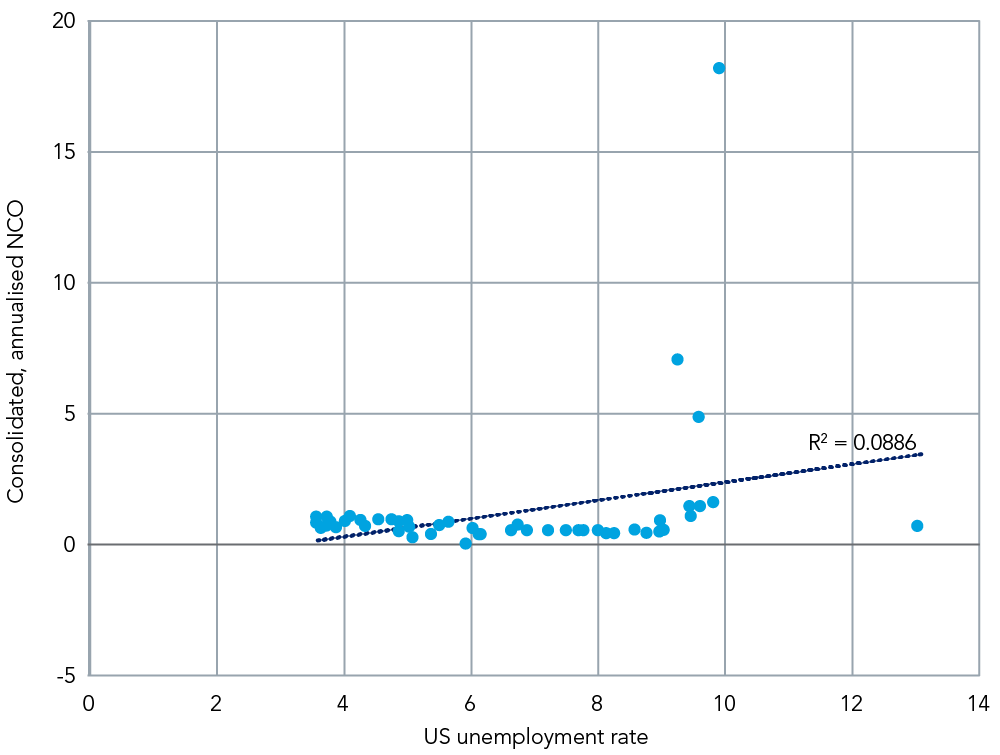

Figure 3. Ally Financial Inc.’s NCO and the US unemployment rate (Q2 2009 – Q3 2021)

Source: Federated Hermes International, using data from Ally Financial Inc./Bureau of Labor Statistics

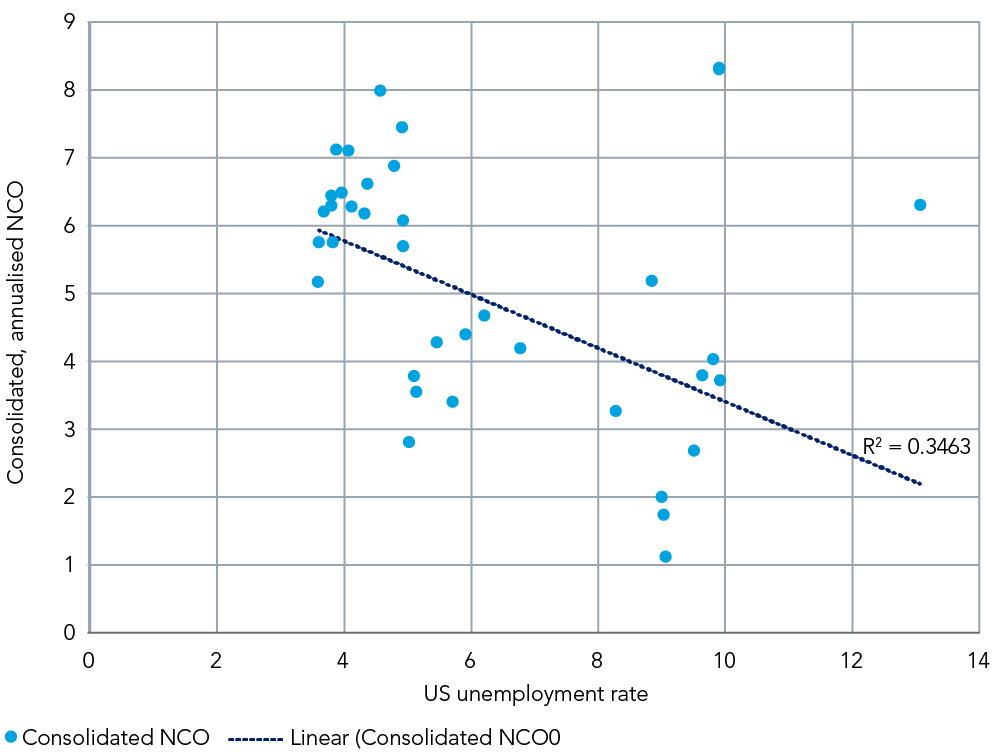

Figure 4. OneMain Financial (OMF)’s NCO and US unemployment rate (Q1 2009 – Q3 2021)

Source: Federated Hermes International, using data from OnMain Financial (OMF)/Bureau of Labor Statistics

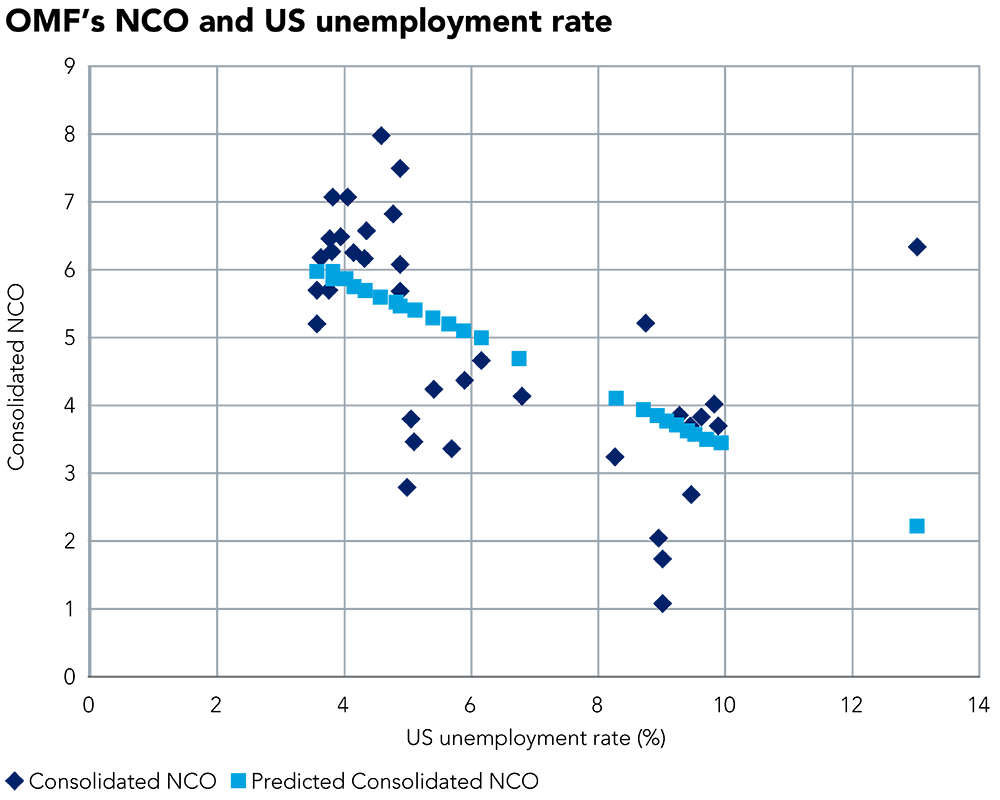

Figure 5: US unemployment rate vs. OMF NCO (predicted and actual) – Q1 2009-Q3 2021

Source: OMF

Hidden variables; unspooken truths

However, it might be too early to declare unemployment and credit risk as disentangled factors, floating independently in economic reality – other relationships could be temporarily distorting the truth.

In an effort to defend the Einstein view of a non-gambling universe, American physicist, David Bohm, later put forward ‘hidden variables’ – actual values a particle may possess that are inaccessible to the external world – to explain away the ‘spooky action at a distance’.

And while experimental data has consistently ruled out ‘hidden variables’ as a plausible explanation for quantum entanglement, the recent relationship breakdown between unemployment and consumer loan quality might well be due to other factors outside the box, such as:

- an economic rebound from the depths of the global financial crisis (GFC) and Covid-19;

- high savings rates that have cushioned debt burdens – recent Bureau of Economic Analysis data, for instance, shows the US savings rate, which spiked higher during the Covid-19 crisis, has fallen from 8.2% to 7.3%;

- various government relief programs keeping poorer US families afloat; and,

- higher values of second-hand vehicles – due to well-documented supply-chain issues – supporting the viability of auto-loans (about 10% of US consumer lending).

Both borrowers and lenders seem relaxed; perhaps, too relaxed.

Released on November 8, 2021, the Fed’s most recent senior loan sector survey paints a picture of growing complacency and softer consumer lending standards.

“[…] Over the third quarter, significant and modest net shares of banks eased standards for credit card and auto loans, respectively,” the Fed report says. “A moderate net share of banks also reported having eased standards for consumer loans other than credit card and auto loans. Consistent with an easing of standards for credit card loans, a significant net share of banks reported easing minimum credit score requirements for credit card loans”.

Just as institutions lower lending standards, though, the background credit conditions look poised to reintroduce higher risks into the equation.

Most importantly, the Fed has flagged a quicker ‘tapering’ of its bond-buying program and potential interest rate rises in 2022 in the face of unexpectedly high inflation. Markets have already seen the short-end of the rates curve rise sharply in anticipation of a tightening Fed bias.

For financial companies, the spectre of falling liquidity and rising rates could bite into net interest margins as funding costs spike.

Despite the looming regime change we expect Ally and OMF to experience a gradual increase in longer-term funding costs rather than a violent upfront hit to margins due to well-diversified structures: Ally features a healthy mix of retail deposits and wholesale funding, while OMF has a 60/40 split of longer-dated fixed unsecured bonds and shorter-term floating notes.

Coming into year-end, US unemployment rates fell again in November to 4.2% – down 0.4% month-on-month and more than 10% below the April 2020 Covid-19 peak7.

Yet current US unemployment figures still remain above pre-pandemic levels just as rising inflation and potential rates increases threaten to reconnect highly indebted consumers with reality.

Investors must stay cool.

The author wishes to thank Nikhil Ajwani, Fixed Income Analyst at the international business of Federated Hermes.

“The more the universe seems comprehensible, the more it also seems pointless. But if there is no solace in the fruits of our research, there is at least consolation in the research itself.”

Steven Weinberg (1933-2021)

References

Ally Financial Inc.

Regression statistics | |

|---|---|

Multiple R | 0.297683767 |

R Square | 0.088615625 |

Adjusted R Square | 0.06962845 |

Standard Error | 0.025913212 |

Observations | 50 |

Source: Federated Hermes International, using data from Ally Financial Inc.

OneMain Financial (OMF)

Regression statistics | |

|---|---|

Multiple R | 0.588446793296888 |

R Square | 0.346269628541391 |

Adjusted R Square | 0.328110451556429 |

Standard Error | 0.014174721508835 |

Observations | 50 |

Source: Federated Hermes International, using data from OMF.