Fast reading

- We have recently upgraded our overall appetite for credit risk as corporate earnings, liquidity and credit fundamentals remain broadly satisfactory.

- Our principal concern is valuations. Even on a duration- and quality-adjusted basis, spreads remain on the rich side of fair.

- Predicting government bond valuations has become more complex, while credit spreads have been relatively more stable. Have sovereign yields now become riskier than credit spreads?

German physicist Werner Heisenberg’s ‘uncertainty principle’ remains foundational to quantum mechanics and, as our latest ‘Fiorino’ column asserts, to market dynamics as well1. According to Heisenberg, it is possible to understand the momentum of an object in motion or its position – but we cannot know both simultaneously.

What makes Heisenberg’s analogy even more appropriate is that the uncertainty principle is explained in waves, which, of course, is analogous to the patterns and gyrations in the market. What goes up, must come down… and vice versa2.

Moreover, the uncertainty principle provides an excellent framework for how we assess the market forces that govern the position and the momentum of credit spreads at our monthly, top-down US-focus Sector Pod meeting and our global, Multi Asset Credit Strategy Meeting (MACSM).

Senior members of the global fixed income team use the meetings to assess and ‘score’ key market drivers such as: macroeconomics, credit fundamentals, technicals, sentiment, and rates (duration and curve). It can help us understand the position of each of these drivers, but our ability to precisely state the momentum can be uncertain.

Uncertainty has been a dominant factor in 2025. It’s worth revisiting our chart that tracks the number of times the word “uncertainty” has been used in the US Federal Reserve’s Beige Book this year3. The downward trend that we observed in late summer has continued. We can see the exact position, and can see the momentum before the event, but not after. The reduction in the word count for “uncertainty” provides the context for our recent upgrades to our overall appetite to credit risk, despite still-tight credit spreads.

Figure 1: Mentions of “uncertainty” in the Fed’s ‘Beige Book’

There was a simultaneous reduction in uncertainty in our macroeconomic and fundamental outlooks over the past two months. This was a key driver of the small upgrade to our overall score for the appetite for credit risk.

Our confidence in moderate, credit-friendly growth on a global basis has improved. Corporate earnings, liquidity and credit fundamentals remain broadly satisfactory4. We remain concerned about the position of lower-end consumers in the US. As a result, smaller, weaker US credit at the margins of the global high yield (HY) market is a no-go area for us at present.

We fully expect to see a few more ‘credit cockroaches5’ peek out from the darkness, and speculate that over-levered, over-bid names in private credit funds will struggle, despite the fact that those same names will benefit from a likely lower interest-rate environment in 2026.

Certain aspects of credit remains appealing based on still-attractive all-in yields, and demand is robust. Market technicals support credit spreads as shown by primary markets in which issuance is absorbed well, even if Microsoft’s record near-US$20bn deal signed in September to boost AI datacentre capacity caused some widening in investment grade (IG) markets.

While we have some concerns about the weaker US consumer outlook, the consumer outlook in Europe remains supported by savings and personal balance sheets. As such, we still like strong asset-backed security (ABS) structures. Our collateralised loan obligation (CLO) book provides us with good ‘carry’ that we lose from keeping the credit book up-in-quality.

Credit remains appealing, based on still-attractive all-in yields, and demand is robust.

In light of tight valuations in CLO tranches, we have been gradually leaning into the ‘decompression trade’ and trimmed some double-B exposure. As for our European subordinated financials (sub-fins)6 exposure, we continue to carry on with our gardening exercise of rotating into names with attractive structures. We believe that the re-rating we have seen this year in sub-fins makes sense because the structural fundamentals of banks has steadily improved over the last few years due to tighter regulations on balance-sheet health. Nonetheless, though diminished, we remain cognisant of the asset class’s potential for volatility.

Given that sentiment remains strong – despite a wobble in Q4 – credit options pricing remains attractive and our ‘credit insurance’ book was extended into 2026. In terms of sector, we can no longer ignore how cheap the chemicals segment has become. As we look into next year, we will investigate the relative value opportunity, particularly in the speciality end of the sector. Emerging market credit remains resilient but spread performance has been led by sectors that are tough for us to embrace, such as pure-play fossil fuels. We also noted at the most recent MACSM that credit default swaps (CDS) underperformed cash.

Our principal concern is valuations. Even on a duration- and quality-adjusted basis, spreads remain on the rich side of fair. We remain fully invested at the higher end of credit quality, save for a handful of attractive credit stories with risk profile slightly below the risk of the market.

Spotlight: Are sovereign yields riskier than credit spreads ?

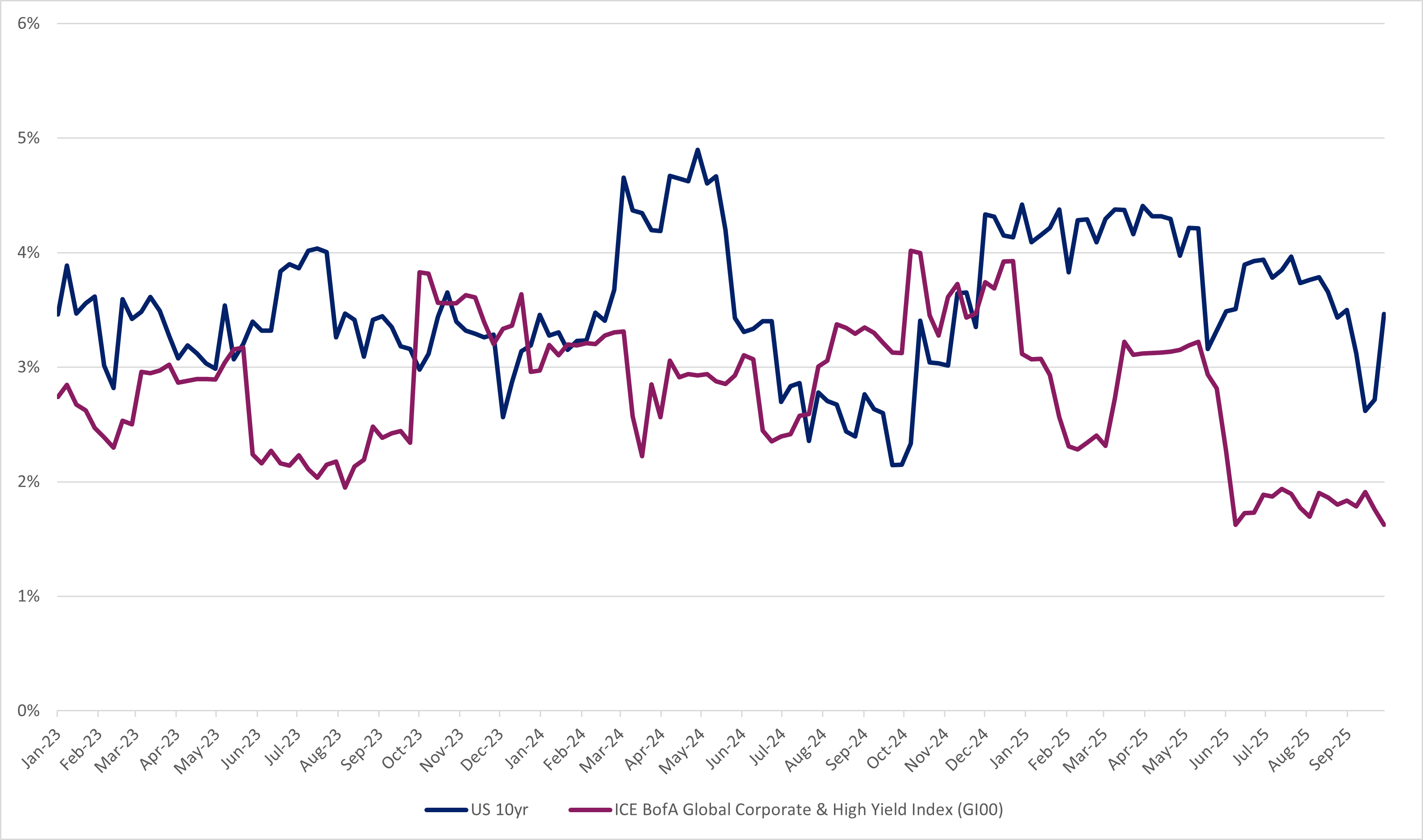

The so-called ‘risk-free rate’ is typically expressed in terms of US government bonds. If US Treasury valuations continue to be this unpredictable, could government yields be riskier than credit spreads?

Assessing the direction of all-in yields has been materially compounded by considerations of fiscal policy as well as monetary policy. As a result, despite low default risk, predicting the valuations of US government bonds has become increasingly difficult.

Interest rate markets have experienced profound volatility driven by shifting monetary policy expectations; inflation surprises; geopolitical uncertainty; supply technicals and, of course, liberal fiscal policies. These factors have led to sharp swings in yields and heightened sensitivity to macro developments.

In comparison, credit spreads have demonstrated remarkable resilience. Supported by strong corporate fundamentals and favourable technical conditions, investment-grade and high-yield spreads have remained relatively stable. This stability has made credit an attractive anchor for portfolios during a period of significant rates turbulence.

Figure 2 shows that on a rolling 12-week basis, over the past three years, the volatility of the US 10-year Treasury has remained elevated compared to spreads for global credit markets.

Figure 2: Rolling 12 weeks volatility between 10-year US Treasuries and the global credit market

Source: Bloomberg, ICE BofA.

Pivoting from the visual presentation of volatility on a ‘flow’ basis, Figure 3 presents what the annual realised volatility was between the US 10-year and global credit. Over the three-year test period, the US 10-year has had an excess of realised volatility of over 75 basis points versus credit.

Figure 3: Annual realised volatility between 10-year US Treasuries and the global credit market

Why have credit spreads been so resilient?

Corporate issuers have entered this period with robust balance sheets, healthy earnings, and conservative leverage profiles. Liquidity buffers remain ample, and refinancing needs look manageable, limiting vulnerability to higher rates. Default rates have stayed low, and rating migration trends have been broadly positive, reinforcing confidence in the credit asset class.

Perhaps most importantly, persistent inflows into credit markets – across IG and HY – combined with limited net supply have created scarcity and driven outperformance. This contrasts with the rates space, where flow dynamics have been more volatile and of lower amplitude. Figure 4 shows this difference in market dynamics. Investment flows into the credit space have been nearly linear in a positive direction. This tells us that demand is the main driver of this period of muted credit-spread volatility.

Figure 4: Investment flows: Global credit cumulated flows vs. sovereign debt cumulated flows

Finally, the MOVE Index – a widely used proxy for US Treasury volatility – has normalised over the past few months. However, this reflects expectations regarding the timing and magnitude of central bank actions that haven’t materialised. Figure 5 shows there is notable dislocation, with realised volatility lagging implied volatility.

Figure 5: MOVE index vs. US 2,10- and 30-years level

What happens next?

On the one hand, credit remains supported by strong fundamentals, attractive carry, robust demand and low default rates, while facing limited volatility. On the other, a myriad of unknows is creating uncertainty in the US government bond market. What would likely make this dynamic reverse is a sharp spike in risk aversion. In this situation, we would expect to see a run for cover: sellers of risk, buyers of rates. We are, however, less confident than we have been in the past. In the spring of 2025, US government bonds failed to serve as the typical harbour from the risk storm caused by the implementation of tariffs. US rates, equities and spreads sold off. For the time being, the risk-free rate may not be so risk free.

1 With full attribution to my colleague Professor Filippo Alloatti, author of Fiorino, from whom I’ve shamelessly borrowed a medium to explain our thoughts on credit markets.

2 Sammy Davis, Jr. “Spinning Wheel” Sammy Davis, Jr. – Spinning Wheel Lyrics | Lyrics.com

3 The Beige Book is a Federal Reserve System publication about current economic conditions across the 12 Federal Reserve Districts. It characterises regional economic conditions and prospects based on a variety of mostly qualitative information, gathered directly from each District’s sources.

4 ‘Satisfactory’ is as a technical term that describes about as optimistic as a credit person can possibly be.

6 Tier 2 capital

BD016960