Looking for Goldilocks: not too hot, nor too cold

The coronavirus pandemic has placed credit markets in a precarious position. Currently, there is a tug-of-war between deteriorating market fundamentals and the incessant injections of liquidity and support from financial banks and governments.

Market fundamentals are now in a far worse position than in February. The market bounce was no natural rise from the bottom, but a massive upwards boost that was triggered by the largest, fastest and most coordinated central-bank intervention in the history of modern finance.

Yet coupled with these risks, there are metrics which indicate that markets are not in a uniformly poorer state – nor that the situation is so bad that fixed-income investors can’t find pockets of good value. In fact, the crisis has highlighted both the relative resilience and value of fixed income as defensive asset class.

With both perspectives in mind, we find ourselves in the middle ground. Overall, we have a positive view on credit – but with caveats. For years, we heard about the Goldilocks economy in which credit thrived when growth was neither too hot nor too cold. Now, credit markets should perform in a scenario that is not too safe, nor too risky.

Overall, we expect ongoing volatility, corporate casualties, for sectors to fight for survival and for an appealing trade-off of risks and returns. Importantly, we believe that both public and private credit markets offer the chance to seek relative value and see a wealth of opportunities to seek alpha in this new coronavirus era.

Relative value between asset classes

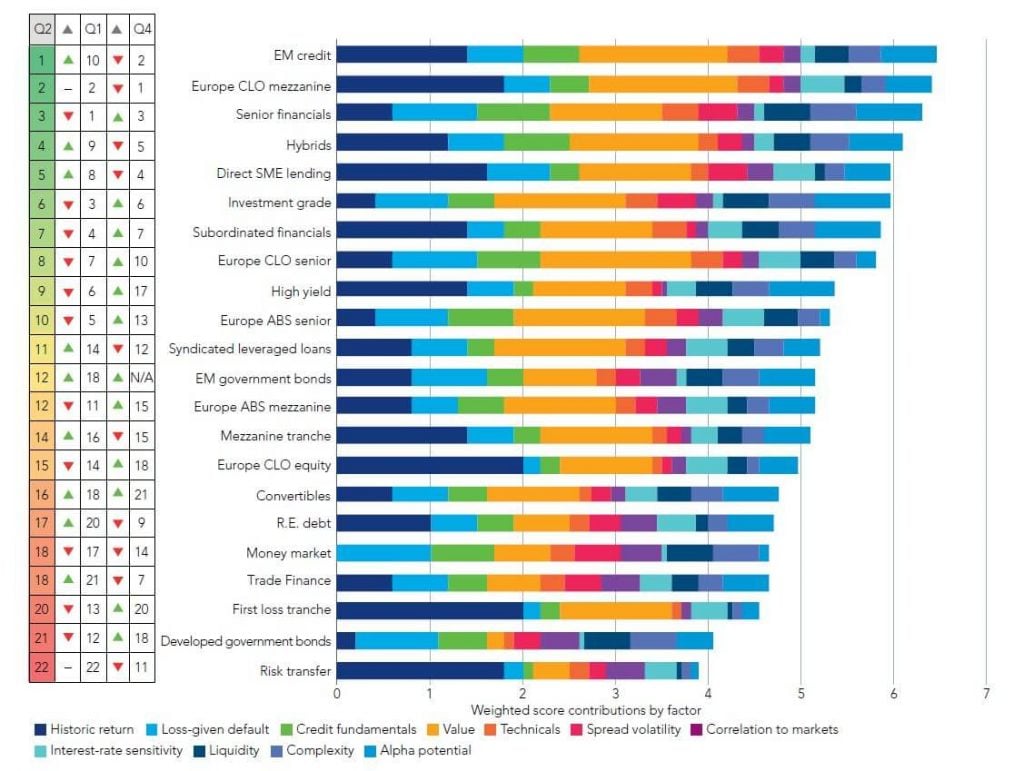

Every quarter, we compile a relative-value framework of fixed-income assets across the public and private credit spectrum, ranking them by 11 different factors. When we compiled our last report, uncertainty had peaked, and our framework favoured more defensive, higher-quality and liquid exposures.

Figure 1. Our Multi Asset Credit relative value framework, 30 June 2020

Federated Hermes, as at 30 June 2020

Since then, a rally in higher-quality exposures, an improved economic outlook and the re-emergence of an illiquidity premium in areas of private credit means the rankings have shifted. For more detail about how our ranking has changed over the last quarter, click between the credit classes below.

The credit class has risen up the ranking as transaction activity picks up and senior and unitranche middle-market margins remain resilient, with the added benefit of stricter covenants and fewer ‘cov-lite’ deals. We see most value in senior secured loans, where an illiquidity premium has resurfaced.

Euro CLO mezzanine tranches continue to offer an attractive spread premium, while the recovery in loan prices demonstrates the market’s resilience. Euro CLO AAA-rated exposures offer interesting spreads and 0% coupon floors.

The spreads of commercial mortgage-backed securities and residential mortgage-backed securities moved wider, reflecting continued uncertainty and the prospect of payment holidays ending.

A balancing act: issues in focus this quarter

In this issue of 360°, we also take a closer look at three areas:

- The Marshall Plan: understanding the historical precedence for coronavirus-era stimulus

- Credit fundamentals: the impact of unprecedented levels of central-bank triage

- Structured credit: how payment holidays could affect asset-backed securities

See below for a flavour of these sections or read the full report for a more comprehensive picture.

Ursula von der Leyen, the European Commission President, recently referenced the Second World War in a bid to put the economic damage from the pandemic into context, arguing that the global economy would require investment “in the form of a Marshall Plan for Europe.”1

In a similar vein to the Marshall Plan, a programme that transferred over $12.9bn ($128bn in today’s money) to European countries after the war, governments across the world are putting in place fiscal measures to stem the damage caused by the pandemic.

Our analysis of the immediate fiscal impulse of five European countries shows that the coronavirus fiscal response significantly outweighs the Marshall Plan program. In Italy, the immediate fiscal measures are worth almost 18 times the amount the country received through the Marshall Plan.

During the second quarter, credit spreads rallied, curves steepened, and macroeconomic data improved sharply. The global response to the coronavirus crisis served to mitigate the immediate and acute financial risks as cash balances were padded, front-end debt was rolled forward (or exchanged) and refinancing rates declined.

Yet this was facilitated by an expansion of already-high central-bank and government balance sheets. This, combined with a forthcoming decline in operating cashflows, means that financial leverage is rising. Operating risks also remain very high, particularly for small and medium-sized businesses.

On the whole, we believe that credit fundamentals will remain challenged as it becomes even more difficult for highly levered firms (particularly in coronavirus-affected sectors) to grow into their balance sheets. The strong and well-provisioned will survive, while the weaker will suffer – making it all the more important to carry out a granular, bottom-up analysis of issuers and their securities.

The structured-credit market appeared to have stabilised by the end of June and the quarter saw new issues of both CLOs and ABSs, which were met with enthusiastic demand from investors. Yet credit fundamentals have deteriorated and there is a sense that the full economic fallout from the pandemic has yet to affect structured securities.

Although CLOs remained liquid and trading volumes held up throughout the quarter, most European CLOs now have high levels of CCC-rated exposures and deteriorating collateral metrics. It is clear that manager selection remains critical to success in the market.

Meanwhile, ABS credit structures continue to function well, although payment-holiday relief – which many debtors have taken advantage of – has created some stress in the market. Going forward, investors will be watching closely to see how many consumers remain on payment holidays at the end of the first three-month relief period.

360° - Credit investing in the coronavirus era:

a new Goldilocks scenario?

Archive: previous editions of 360°

As fixed-income markets have moved through the economic cycle, our thinking has also developed – take a look at some of our previous reports to see how the investment landscape has changed over the past year.