Hermes Investment Management, the £28.5 billion manager committed to delivering holistic returns – outcomes for its clients that go far beyond the financial, has today published research by its Credit and stewardship teams demonstrating the impact of ESG (environmental, social and governance) factors on credit spreads, and developed a pricing model to capture the influence of these factors on credit instruments.

The white paper, Pricing ESG risks in credit markets, by Mitch Reznick, CFA, Co-Head of Credit, and Dr Michael Viehs, Manager, Hermes EOS, examines the relationship between a company’s Quantitative ESG (QESG) Score and credit default swaps (CDS). The QESG Score is a measure used across Hermes’ investment teams which is derived from a range of sustainability data, including proprietary insights from the stewardship and engagement team, Hermes EOS.

The research found that:

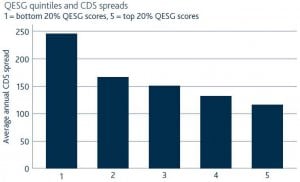

- Companies with the lowest QESG Scores, i.e. the weakest ESG credentials, tend to have the widest CDS spreads

- The correlation between QESG Scores and spreads is consistent but not entirely linear, with the greatest change occurring between the lowest ESG-scoring first quintile and the second quintile (see chart 1 below)

- Although there are correlations between companies’ QESG Scores and their credit ratings, there is a wide dispersion of QESG Scores within each rating band. This means that credit ratings do not sufficiently reflect ESG risks

- Hermes have now developed a model that can be used to quantify the contribution of ESG risk to credit spreads. This model can be used to identify potential outperformers – companies with wide spreads and high QESG Scores – and potential underperformers – companies with tight spreads but poor QESG Scores

While the Credit team have been integrating ESG considerations into their investment decisions for several years, this research is the first time a clear relationship between ESG credentials and performance has been proven from a credit perspective. Prior to these innovative findings, the team estimated the impact of ESG risk on valuations in anecdotal terms. By plotting spreads against QESG Scores, they have developed a pricing model that quantifies the compensation investors should receive for a given level of ESG risk. This complements the models investors currently use to price the ‘core’ operating and financial credit risks.

“Although credit risk is the principal driver of both the level of and changes in credit spreads, we know that ESG factors also influence credit spreads. Given that we know this, in order to deliver on our fiduciary duties we are compelled to asses and price ESG risks when making investment decisions.”

“Until now our ability to price ESG risk was limited because there was no optimal pricing model for ESG risks. This research is a first step from which to develop more investment tools that bring ESG analysis even further into the investment process. Its findings add more weight to the argument that ESG risks are ignored at investors’ peril.”

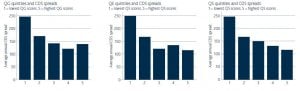

“Because ESG analysis considers multiple sustainability concerns, it is worth taking a closer look at the three main sub-categories – environmental, social and governance – to learn if any one of them had a stronger correlation with spreads than others. By examining the average annual CDS spreads for every environmental, social and governance quintile, we can determine whether the observed effect for the overall QESG Scores holds true in a similar way. The results matched our analysis of the link between QESG Scores and spreads: for all three ESG dimensions, issuers with the lowest scores had the highest CDS spreads (see chart 2 below).”

“Credit investors must use a more precise measure of ESG risk if they aim to accurately capture its influence on spreads. By plotting spreads against QESG Scores, we have been able to develop a pricing model that quantifies the compensation we should receive for a given level of ESG risk. As such, the model helps us identify opportunities in lower-rated companies with higher ESG scores, and to spot issuers at risk because their spreads are too tight relative to their ESG scores.”

Read the paper in full here

Chart 1: Average annual CDS spreads by QESG quintile (2012-2016)

Source: Own calculations as at February 2017. Data sourced from Hermes Global Equities and Bloomberg. Corrected for outliers.

Chart 2: Average CDS spreads by environmental, social and governance quintiles, 2012-2016

Source: Own calculations as at February 2017. Data sourced from Hermes Global Equities and Bloomberg. Corrected for outliers.

In September 2016 Hermes’ Global Equities team published the report ESG Investing: It still makes you feel good, it still makes you money, which followed on from an earlier study conducted by the team in 2014 and examined the impact of environmental, social and governance (ESG) factors on equity returns from 2009-2016.