As Europe grapples with a gas crisis caused by the war in Ukraine, investors are facing up to a fundamental truth: energy is everything.

Russia’s efforts to restrict, or cut off, the flow of natural gas to Europe via the Nord Stream 1 pipeline, which runs under the Baltic Sea from Russia to Germany, has led to fears of a full-blown recession in Germany and elsewhere, which could have dire consequences for financial institutions in the region.

At the time of writing, major gas leaks at the Nord Stream 1 and 2 pipelines, were being blamed on sabotage, underscoring Europe’s dependence on Russian energy.

While the energy crisis represents a serious threat to Europe’s economies, the fallout from this disruptive period may result in the region establishing more secure energy resources, which are more supportive of its financial institutions.

Quantum spin class

Quantum ‘spin’ is one of the most poorly understood but easily demonstrated properties of atomic particles.

First observed in an experiment by the German physicists Otto Stern and Walter Gerlach in the 1920s, spin describes the intrinsic ‘angular momentum’ of a quantum particle – subatomic particles such as electrons and the heavier muons – rather than actual spinning as understood in the macro world.

Imagine a ball rotating, except it’s not a ball and it isn’t rotating!

Figure 1. An electron’s spin

Stern and Gerlach showed that if exposed to an asymmetric magnetic force, quantum particles would only accumulate in two opposing directions – dubbed ‘up’ and ‘down’ – instead of scattering across a broad range of destinations as expected.

About a decade after the Stern-Gerlach experiment, the English physicist Paul Dirac combined some elements of the theory of relativity and quantum mechanics (the two most successful, if not compatible, physical explanations of our universe), to prove spin was an inbuilt, and inseparable, quality of particles.

Russia’s gas squeeze hits markets

In many ways, economies are more difficult to model than even quantum complexities, but markets can also reveal fundamental qualities when exposed to certain forces.

The Russian energy squeeze on Europe is undoubtedly one of the most disruptive forces imposed upon the region in decades.

The reduction in gas supply through Nord Stream 1 has sent energy prices surging higher, cutting into both household incomes and business profits. There is, however, also the possibility that soaring energy prices will lower demand, which could fend off the prospect of direct energy-rationing in Europe.

Should Russia turn off the gas pipelines completely, Europe would likely see further falls in demand. Since the Ukraine crisis began in February, Europe’s manufacturing industry has cut gas consumption by about 30% relative to average long-term usage, according to International Energy Agency figures.

Nonetheless, as households and small- and medium-sized enterprises (SMEs) consume more gas during the winter, they will need to rein-in energy use over the months ahead. The strain is already beginning to tell, and many European governments have announced energy price subsidies.

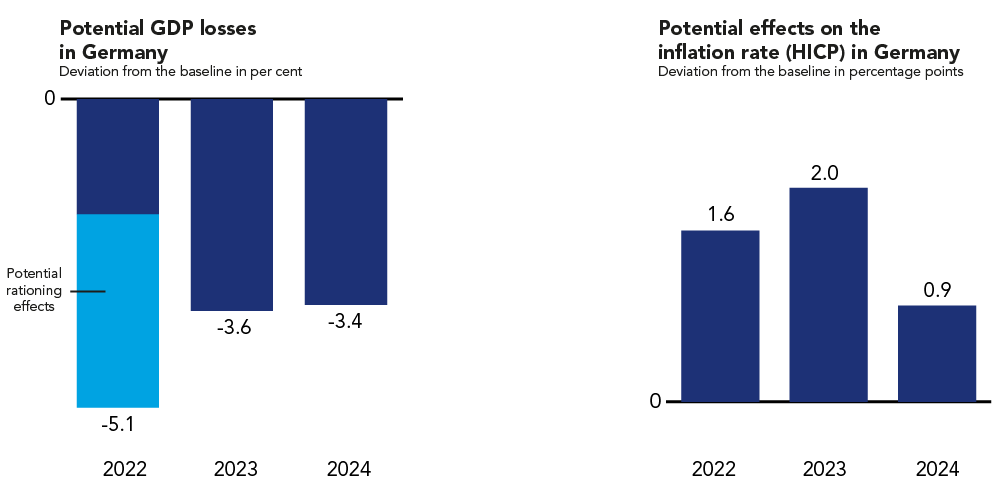

Risks if the gas flows stop

If the flow of Russian gas does stop, the German economy, in particular, would likely fall into a deep recession, according to an April 2022 analysis by Deutsche Bundesbank.

Figure 2: The impact of a halt to Russian gas supplies

Given the clear and present danger highlighted by this data, some European banks began disclosing internal stress-tests during the second quarter of this year to model the impact of Russian gas disruption on their balance sheets. A number of lenders will report detailed scenario analysis results to the European Central Bank with further disclosures expected from October this year.

Many European banks have begun addressing investor concerns around Russian natural gas. In June, Deutsche Bank’s Chief Financial Officer James von Moltke said the group’s own scenario analyses generated similar results to the Bundesbank study. “It is a relatively significant impact on the economy… and potentially a lasting one because you can’t re-factor the economy and source [new energy] supplies all that quickly, so it potentially would be an effect that goes beyond one year,” he said. Nonetheless, Mr von Moltke emphasised that the group’s credit book could manage even the most severe scenarios the stress tests presented, and that Germany had fiscal space and the political will to support the economy1.

We agree with the Deutsche Bank analysis. By some estimates Europe needs to cut energy consumption by a further 20% without Russian gas; while supply conditions are set to remain tight through 2023, implying a multi-year crunch.

As a result, European economies will need to turn on large-scale financial support mechanisms to cushion the energy blow.

We expect to see a combination of fiscal as well as forbearance measures in the form of:

- guarantee schemes;

- credit facility lines; and,

- reduction of capital buffers to avoid a repeat of the aggressive bank deleveraging experienced during the Euro sovereign crisis.

All is not lost, however.

Germany, for instance, says the country “is now better prepared for a halt to Russian supplies” and that the total gas storage level is almost 87%2.

EU-wide aggregate gas storage figures also support the German claims of resilience.

Despite all the angst surrounding Nord Stream 1, the Title Transfer Facility pricing benchmark – representing the state of the Northwest European natural gas market – has done a significant amount of work in attracting liquefied natural gas (LNG) imports to the region.

At the same time, JP Morgan economists have forecast Northwest European natural gas storage to reach 94% capacity by November, one month into the start of the official heating season for the region, even with Nord Stream 1 offline.

European banks, meanwhile, are flashing reassuring prudential metrics across fundamental balance sheet qualities such as capital, solvency, leverage and liquidity. Of course, non-performing loans will spike higher in a recession but from a low base (of just 1.9% at the end of the first quarter of this year, according to European Banking Authority data).

Overall, collateral values are holding even as the energy crunch bears down on markets. European banks with intrinsically high-quality features may still have plenty of upside.

The crisis as a catalyst to action

In summary, the world is spinning, seemingly out of control.

Spiralling energy prices in Europe on the back of deliberate Russian gas bottle-necking has put households, businesses, governments and markets on edge.

Yet the energy crisis has catalysed the region into action.

Within a couple of years Europe might be able to wean itself off Russian gas. Reforms in the European gas-pricing system, including pushing out hedging horizons, also offer the prospect of better-functioning markets over the long term.

If the energy transition is managed well, Europe – including its financial institutions – have a good chance of making it through the current turbulence with strong fundamentals pointing to a ‘spin up’ state.

Albert Einstein, 1949