Amid bouts of panic buying and a surge in people cooking at home, Covid-19 lockdowns triggered a shift in the relationship between individuals and their local supermarkets – grocery stores were one of the few places where people were free to go.

During the height of the pandemic, the UK supermarket sector saw grocery sales soar; for example, alcohol (+ 27.6%), sweet foods used in home cooking (+23.5%) and snacks (+18.8%). Perhaps surprisingly, oral care was the only category that declined (-2.6%) during the period1.

Where next for the Covid winners?

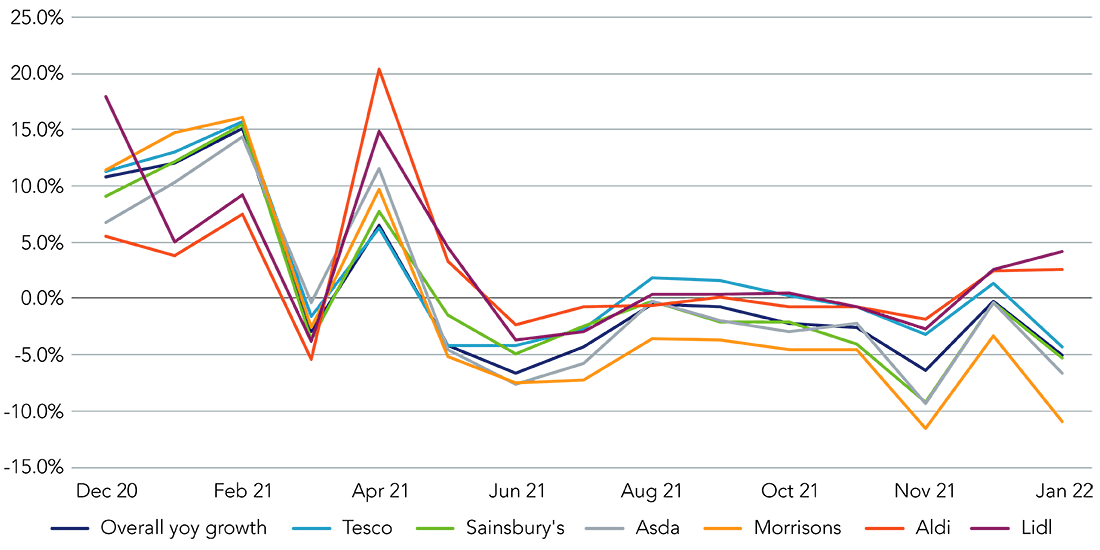

In the three months to 23 January 2022, UK grocery sales were down 3.8% from a year earlier, although sales across the sector are still up 8% against pre-pandemic levels (2019)2. January data from Kantar suggest that the slowdown in sales will continue as buying habits revert to their pre-pandemic norms, characterised by lower basket sizes and higher footfall.

Figure 1. Sales growth among UK supermarkets

Source: Kantar, January 2022

We expect the slowdown in grocery sales volume to continue through 2022 as Covid-related restrictions on the hospitality sector ease and people return to offices (flexible working is likely to keep sales above pre-pandemic levels into the medium term). However, as the sector emerges from the fog of one global crisis, it immediately finds itself on the frontline of another.

Negotiating rising prices

Having played a vital role during the worst months of the pandemic, the supermarket sector also finds itself at the sharp edge of the inflation crisis, which is widely expected to get worse before it gets better. With inflation hovering at the 5.5% mark in the UK, our senior economist expects prices to touch 7% before eventually declining over the latter half of the year. This trend will give rise to yet another shift in the pattern of the weekly shop.

So far, supermarkets are managing inflation pressures effectively. Suppliers and supermarkets are experiencing cost pressures, driven by high commodity and freight costs, a shortage of HGV drivers and wage inflation. These headwinds make them particularly vulnerable given the sector’s low margins. However, leading chains have been able to offset this through increased prices, cost savings and by working with suppliers. Tesco, the country’s largest supermarket chain, is experiencing cost inflation of around 5% and has identified £1bn of cost savings over the next three years. Sainsbury’s, the country’s second-largest chain, has raised its retail profit guidance by £50m, driven largely by volume but also by tighter cost controls3.

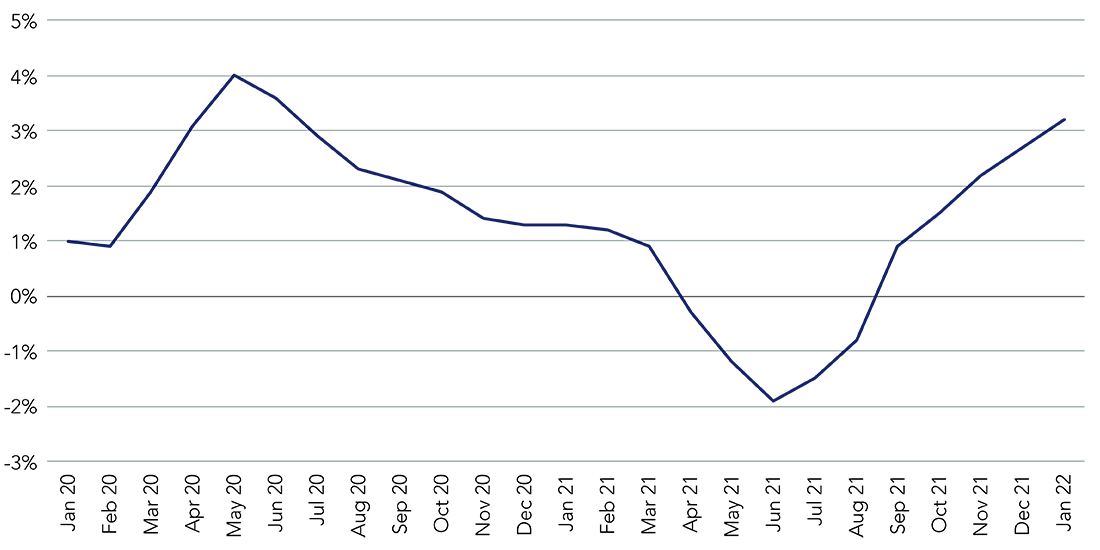

According to Kantar, grocery price inflation reached 3.8% in January 2022 (and was 3.2% during the 12 weeks to 23 January).

Figure 2. Food inflation rate

Source: Kantar, January 2022

Tesco and Sainsbury’s reported that in the third quarter, food inflation was around 1%; this is below the market as both companies strove to maintain value perception. Having said that, Tesco’s Chairman John Murray Allan recently commented that prices of Tesco products could increase by an average of 5% in the coming months4.

In our view, consumers will absorb these price increases by cutting down on non-discretionary spending, and shifting more towards private label products and promotions.

Private equity waiting in the wings: bad news for creditors

M&S: Performance improved and event risk

PE funds tend to significantly increase leverage of the acquired company, and sell assets to obtain a rapid financial gain or pursue dividend recapitalisations, which are negative for creditors. In the case of Asda, leverage increased to 5.9x (as of June 2021, according to Moody’s) and is expected to remain above 5x. We see risk of continued activity in the space, with rumours of Apollo showing interest in Sainsbury’s (reported in August) and M&S (reported in November).

Private equity funds have significant dry powder (unspent cash that is available to invest) with 25 private equity firms holding $509bn as of August 2021, according to S&P Global Market Intelligence. With significant capital to invest, the market has seen a boom in the number of deals, with 235 buyouts of UK-based companies in 2021, according to CMBOR5:

- In June, Morrisons was acquired by CD&R private equity firm, and the acquisition represented a 60% premium on the share price before the bid started, with an EV/EBITDA multiple estimated around 9.5x (based on 2019 EBITDA) for an enterprise value of around £10bn, financed through equity, and credit facilities that are yet to be refinanced as it got delayed to 2022. In February 2022, banks involved in the takeover of Morrisons sold £1.2bn in junior secured debt to credit funds, with the senior part of the capital structure left to be sold to investors through syndication.

- Asda was acquired by Issa brothers and TDR Capital for £6.8bn. The EV/EBITDA multiple was estimated at around 5.7x (based on 2019 EBITDA) with only £780m of equity contribution, and the rest coming from debt incurred, selling warehouses and distribution for £950m, and a £500m contribution from Walmart.

The attractiveness of the sector to private equity lies in their large property portfolios, reliable and predictable cash flows, and the UK’s historically tolerant attitude towards takeovers. That said, we acknowledge that the takeover rules announced in January (which will allow the government to scrutinise deals, impose conditions or block proposed deals that threaten national security), could act as a barrier for future buyouts.

1 Source: UK Government, Public Health England. Figures calculated to 21 June 2020, year on year.

2 Source: Kantar, January 2022

3 Source: Kantar, January 2022

5 The Centre for Private Equity and Market Buy-Out Research