Robin Usson, Credit Analyst at the international business of Federated Hermes, believes new escrow rules could alleviate liquidity conditions onshore and mark the inflection point the industry had been waiting for, at the very least for selected privately-owned enterprises.

On January 19, 2022, Reuters reported that China was drafting rules to ease developers’ use of escrow funds. The proposed new rules would allow developers to use escrow funds to firstly complete unfinished buildings and then use for additional purposes, with a prioritisation on onshore debt repayment of developers and wages.

The proposed new rules are credit positive for the sector, alleviating the current liquidity crunch induced post-Evergrande when a clampdown on escrow funds only allowed developers to (a) complete a proportion of unfinished buildings and (b) nothing else.

Details of these new rules are yet to be published and whilst many conditions could be attached and implementation might not be uniform across regions, we believe they will mark an inflection point for the sector. Material onshore liquidity easing could ensue in the following weeks and months, essentially acting as the first domino for a broader recovery in spreads / bonds prices for offshore bonds.

Average OAS for Higher Quality / Xover risk China Property credits: most recent sell-off is an onshore liquidity sell-off (Note: POEs = Privately-owned enterprises)

Source: Federated Hermes, Bloomberg

To provide more colour on the reason why we view this as a turning point, we must take a step back and review the measures implemented on escrow accounts after the Evergrande fall-out.

Evergrande contagion

The default of Evergrande shed light on some “excesses” of pre-sales’ use of proceeds. It appeared that Evergrande was overusing proceeds from pre-sales to fund growth and other non-property related investments, effectively creating an insatiable need for everlasting growth. As the music stopped, this pre-sale funding model came tumbling down like a house of cards as part of the proceeds from pre-sales, which should have been earmarked for construction costs, had instead evaporated.

Scrambling to protect consumers’ interest (a key focus to ensure social stability in the context of Common Prosperity), local regulators shifted their stance on the use of escrow accounts from one extreme (little oversight) to the other (too much oversight), abruptly curbing withdrawals from these accounts amid fears of contagion post Evergrande fall-out. Consequently, developers became unable to tap into cash in escrow accounts from pre-sales, which created severe onshore liquidity issues, even for the better-capitalised developers. High unrestricted cash balances on the books essentially meant nothing as this “unrestricted” cash became no longer accessible by developers.

Fast forward a few months and onshore maturities started kicking (Dec-2021 / Q1 2022). As developers elected to avoid defaults at all-costs with escrow accounts now unavailable for use, scarce liquidity of better-capitalised developers were earmarked for onshore & offshore bond maturities. These bonds have cross-default provisions, meaning a payment failure would trigger a default.

With this cash crunch, developers were essentially willing to forsake paying suppliers or other types of off-balance sheet debt to bypass a default. This shift in prioritisation explains why we’ve seen daily news year-to-date about developers either not (i) paying suppliers, (ii) trust providers or (iii) ABS tranches because, out of the scarce liquidity developers could gather, all was set aside for onshore & offshore bond repayments as market access for both remained shut. This is what ultimately led to this broader sell-off, payment failure of hidden debt because of this lack of access to liquidity.

A sector in secular decline, cherry-picking of survivors remains key for long-term outperformance

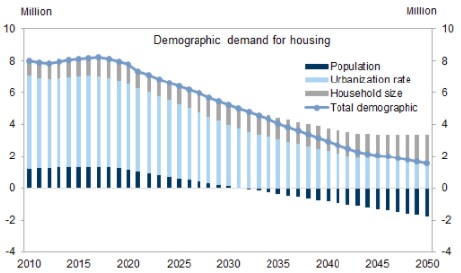

Property sales in China remain in structural decline for demographic-led reasons. We expect sales volumes to decline c.-45% over the coming decade to 2030. Or to put it differently, we expect a 5% annual decline of volumes. This is hardly exciting, and given the amount of leverage within the sector, defaults will indubitably ensue. However, paramount to Chinese regulators is stability.

Household formation may decline from 8mn per year in the 2010s to 1.5mn by 2050

Source: Haver Analytics, Wind, Goldman Sachs Global Investment Research

As China now attempts to cut its dependence on real estate, we do not expect a significant relaxation of policy aside from a loosening of access to liquidity as our base case scenario. In our opinion, policy easing will be used as last resort to support the downside, as opposed to stimulating the industry, with a particular focus on price stability.

Over the next decade, volumes will inherently come down given the ongoing demographic pressure but should be partially offset by price stability (+1-2% a year) meaning sales value would be down 3-4% a year in a (admittedly faulty) linear model.

Yet before the recent news on escrow accounts, bond valuations were pricing ~75% of the market going bust (ie almost all POEs), which seems misaligned with a long-term declining, yet still stable, environment where better-capitalised operators can in fact survive and in some cases even prosper (SOEs are expected to take market share).

In the face of this extreme negative sentiment for POEs, regulators must come up with a narrative to support POEs’ liquidity. This would bolster social stability and prevent a situation whereby consumers stop buying properties from POEs altogether as a result of insolvency. If this were to occur, house prices could plummet, which in turn could lead to social instability. As ~70% of China’s household wealth is tied to property, price stability is closely linked to social stability. With the announcement of this new set of rules, we think that political will to support selected POEs has increased.

In conclusion, while we still expect high headline risk and choppy bond prices over the next quarters, we think a clear set of rules on escrow funds could loosen the vice on liquidity and ultimately help maintain price stability by maintaining better-capitalised privately-owned developers afloat. This could be a potential turning point for a broader and more sustained rally in the onshore and offshore market. Solving the onshore liquidity crisis should be the first step towards stabilisation of the sector. We continue to view our previous screens and adjusted leverage metrics as important tools to identify long-term survivors in a structurally declining sector, and from here we are looking for attractive deeply convex opportunities under our stressed framework.