A shift from the winners of yesterday

Having now entered a period of structurally higher interest rates, combined with potentially slower economic growth, investors should expect a shift away from the market leaders of the last decade. This process has already started; small and mid-cap stocks generated relative outperformance in 2022, while the NASDAQ 100 (a proxy for large-cap growth/tech) saw valuations compress, with the index closing the year down by over 30%.1

The focus has now switched from cash consumptive companies of the last decade to cash generative ones. Corporate balance sheets are more leveraged than they have been historically, and margin pressure is mounting as companies deal with increased interest, raw material and salary costs. High quality SMID businesses with strong balance sheets, robust market positioning and pricing power will benefit – exactly the type of businesses owned in this strategy.

Over the long term, US SMID has provided superior returns to both large and small cap companies

Valuations are attractive

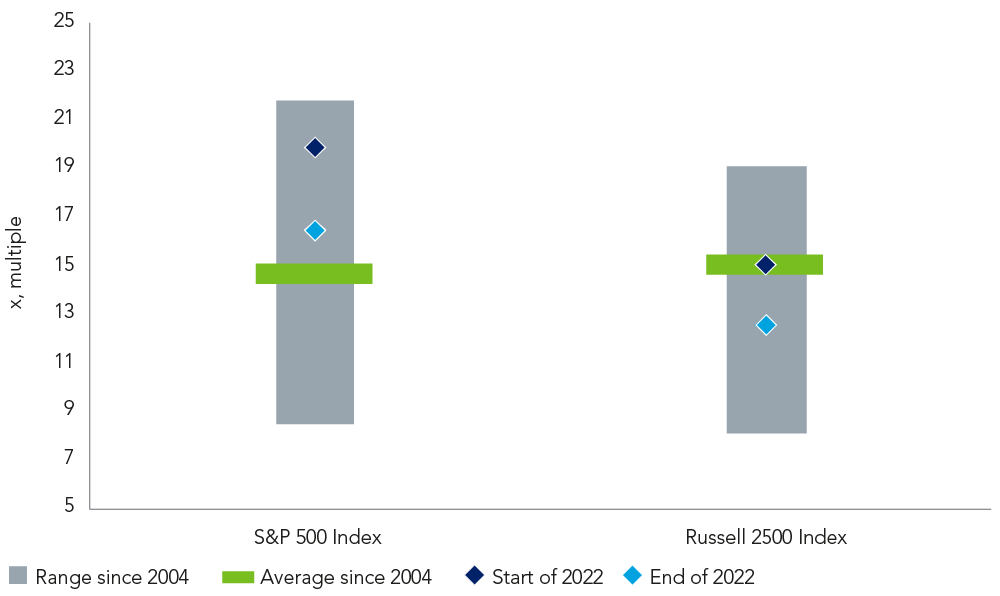

Furthermore, US SMID cap valuations are attractive, providing a great entry point for investors. Current valuations for US SMID companies, on a forward price-to-earnings (p/e) basis, are both cheap relative to their long-term average but also two standard deviations cheaper than US large caps, as illustrated below. Other valuation metrics, for example price-to-book, tell a similar story.

We believe that current valuations are pricing in a deeply negative economic outcome which may prove to be overly pessimistic. Valuations at this level are pricing in little if any growth, and present an opportunity for active managers to take advantage of attractive entry points into quality companies. Such companies offer an attractive risk/reward profile – downside protection in a recessionary environment and structural growth to position portfolios for a stock market recovery.

Figure 1: Forward price-to-earnings since 2004

Source: Bloomberg, as at 31 December 2022.

Regulatory environment supports domestically-focused companies

We continue to see an unprecedented boost to infrastructure support this year, which will provide a tailwind for US companies and in particular SMID cap. The Infrastructure Investment and Jobs Act (IIJA), which was signed into law in 2021, has authorised $1.2tn for infrastructure spending2, which includes the building of roads, bridges and other major projects which will benefit US SMID companies.

Taking this piece of legislation specifically, the Federated Hermes US Equities team view this as having a very beneficial multi-year impact on domestic investment, benefitting such holdings as industry leader Martin Marietta, an aggregates business based in Raleigh, North Carolina. The United States Census Bureau estimates that the national population will grow from its 2000 level (281 million) to reach almost 400 million people by 20503, with much of this population growth expected to occur in the southern states of the US. This will, de facto, lead to a surge in construction, supporting companies like Martin Marietta who have the leading market position for building materials within the region.

Don’t forget the little guy

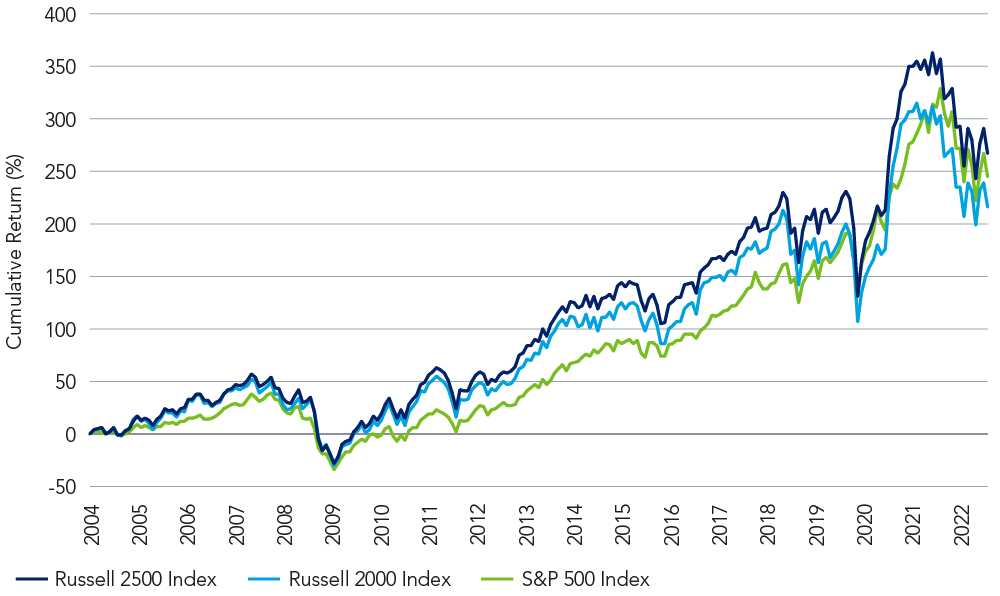

Historically, it has been easy to overlook US SMID as an asset class; many of the headlines post the 2008 Global Financial Crisis (GFC) have been dominated by large cap tech names. However, over the long term, US SMID has provided superior returns to both large and small cap companies, as demonstrated below.

Figure 2: US SMID provide superior returns compared to large/small cap

Source: Bloomberg, as at 31 December 2022.

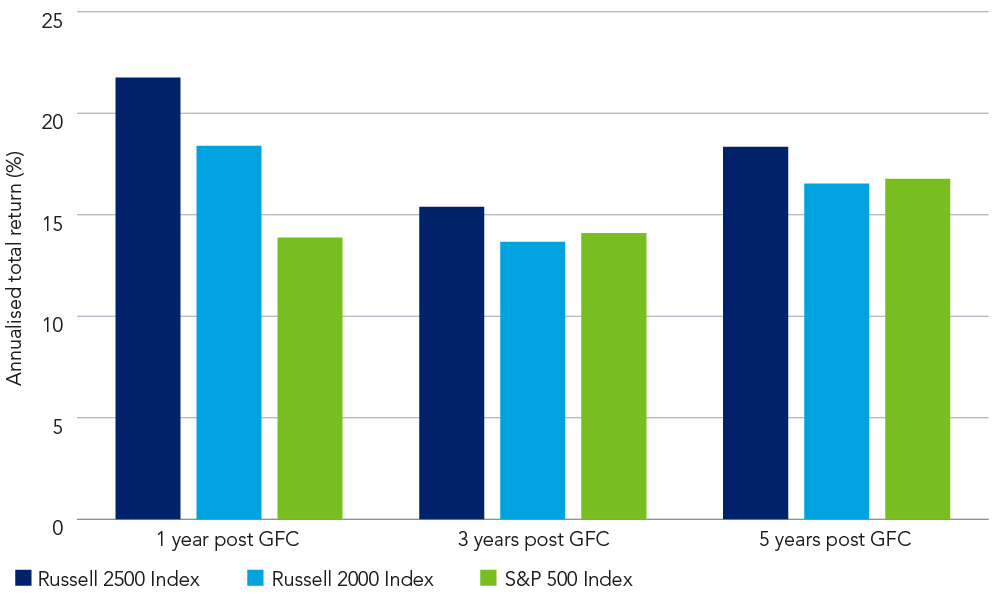

The benefits of a US SMID allocation in early cycle can similarly be seen below. US SMID is the strongest performer over one, three and five years post-GFC and can provide superior growth, with lower volatility than small cap.

SMID can also provide stronger growth as it offers exposure to companies that are earlier in their development, whereas large-cap companies can see their growth opportunities diminish as their development matures. In any given year, 95%4 of global merger and acquisition (M&A) deals involve a SMID company being bought. They also benefit from higher inside ownership than their large-cap peers, as owners have more vested interest in delivering strong and sustainable returns.

Figure 3: Annualised returns in early cycle

Source: Bloomberg, as at 31 December 2022.

Given the change in monetary policy that has been ‘status quo’ since the GFC, the supportive regulatory backdrop, and the attractiveness of the valuation of the asset class, we remain constructive on the opportunity presented by US SMID. Investors who have recessionary concerns should allocate to a US SMID fund that has a quality bias to provide downside resiliency to portfolios in 2023.

To find out more about our US SMID Equity offering, please visit our capability page.

1 NASDAQ 100 Index, as at December 2022.

2 Government Finance Officers Association, ‘Infrastructure Investment and Jobs Act (IIJA) Implementation Resources’, as at 2021.

3 U.S Census Bureau, International Database, as at 2020.

4 JP Morgan, ‘The case for SMID’, as at 31 October 2022.