We believe long-term investment in high-quality companies generates excess returns over market cycles.

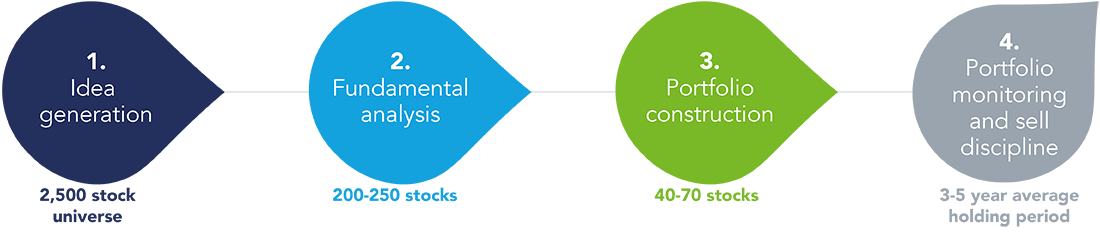

Our usual holding period of three-to-five years allows us to participate in the secular-growth characteristics of many small-cap stocks, and exploit typical market short-termism.

Our focus on quality and cash-flow generation offers a degree of downside protection that we believe provides a relatively low-risk way to access this asset class.

We are an active owner and partner. In practice, this means we maintain a regular dialogue with the companies we own and encourage strong ESG practices.

Federated Hermes Limited has managed regional small-cap strategies since 1987.

Mark Sherlock, CFA, FCA

Head of US Equities

Henry Biddle, CFA, ACA

Portfolio Manager

Michael Russell, CFA

Portfolio Manager