The Chinese property market is widely considered to be the most important industry sector in the world. It has, over the last decade, provided the firepower for global economic growth.

Valued at $55tn, Chinese real estate is four times the size of the country’s GDP, two-thirds that of global GDP and twice the size of its US counterpart. But all is not well beneath the sector’s surface and, by virtue of its size, all investors – whether directly or indirectly exposed – will be profoundly impacted by what the Chinese property sector does next.

Its problems are greater than Evergrande

In September, the Chinese government successfully contained the crisis at the world’s most indebted real estate developer, but the issues that underlay the Evergrande crisis – debt and demographics – are still at work within the system.

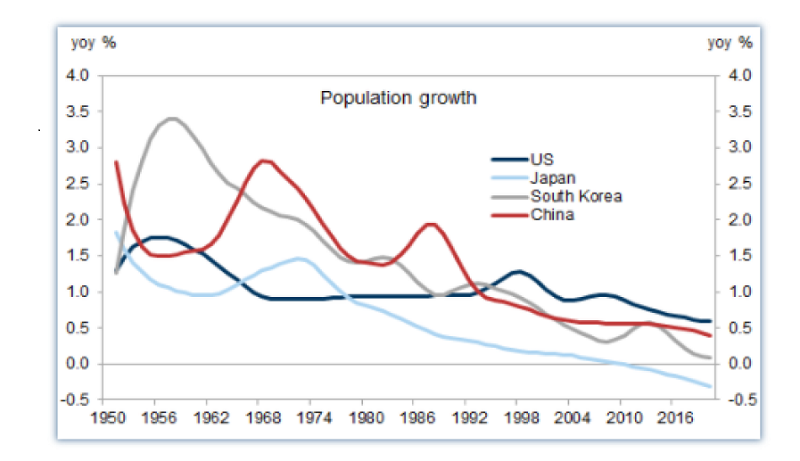

China’s property and construction sector, bloated by overinvestment and overbuilding, represents 29% of economic growth, yet a fifth of the country’s housing units lie empty. Much of the stock falls outside the financial reach of the vast majority of the population and is, instead, being propped up by investment, i.e. speculation demand. Slowing urbanisation, fewer marriages, and a fertility rate that remains stubbornly low at 1.3 1 means that demographically driven demand is nowhere on the horizon.

The Chinese government, acutely aware of this, is seeking to reallocate capital away from property to new sources of economic growth, namely technology, as it aims to enhance factors of productivity and offset the impact of declining demographics on economic output.

Figure 1: Population growth declining in China

Source: Haver Analytics, Goldman Sachs Global Investment Research

All this plays into a new growth paradigm that the government has labelled ‘common prosperity’; a key part of which is to promote property as an instrument of living not speculation.

To achieve this, it has a plethora of tools at its disposal to cool investment demand, while simultaneously de-risking the sector and stabilising property prices. These tools include:

Three red lines

- A supply-side reform aimed at cutting excessive leverage

- Developers are expected to comply with the following restrictions: (1) liability-to-asset ratio, excluding contract liabilities, of lower than 70%; (2) net gearing lower than 100%; and (3) cash to short-term debt ratio of more than 1.0x.

- The more red lines crossed, the less able the developer will be to grow their debt.

Table 1. Financial Ratios used in the 3 red lines testing

Red line | Ratios | Threshold | |

|---|---|---|---|

Red line 1 | Leverage | Liability/Assets (pre sale deposits excluded) | <=70% |

Red line 2 | Gearing | Net interest bearing debts/total equity | <=100% |

Red line 3 | Liquidity | Unrestricted cash/short-term debt | =>1x |

Two red lines

- A demand-side reform aimed at cutting ‘real estate’ systemic risk within the financial system

- Banks must limit exposure to property loans to a maximum of 40% of total loans, including loans to developers and mortgages to homeowners (limits depend on the bank’s size).

Table 2. Property Loan Limits used in the two red lines testing

Tier | Property/Total loan limit | Residential mortgage/Total loans limit |

|---|---|---|

Large banks | 40.0% | 32.5% |

Mid-sized banks | 27.5% | 20.0% |

Small and non-regional banks | 22.5% | 17.5% |

Regional banks | 17.5% | 12.5% |

Village banks | 12.5% | 7.5% |

Source: People’s Bank of Chins, CBIRC, and Moody’s Investors Service

Pre-sale system

- The widespread practice of selling properties before they are complete is under government scrutiny and in the crossfire for reform. In response to some recent violations by developers, new rules are being drafted to strengthen the supervision of developers’ pre-sales funds, which are supposed to be stored in escrow accounts until home delivery.

- In many low-tier cities, pre-sales can begin as soon as construction has started, however, some past excesses have made the system a leading candidate for reform. We are closely monitoring the pace at which these tightening measures are rolled out as many developers still operate on a fast-turnover model and are heavily reliant on pre-sales. Changes in the regime have already begun to negatively impact developers’ cashflow as capital markets remain mostly shut for now.

Property tax reform

Proposed tax reforms are now tied to the common prosperity goal, implying that:

- taxation is viewed as a market stabilisation measure to curb price growth; and

- taxation will target the country’s high-income groups.

- The property tax could hurt speculation and investment demand but the impact on structural and upgrade demand is likely to be negligible. The move would serve as an important means of establishing a wealth redistribution system as part of government efforts to achieve common prosperity.

Other measures that the Chinese government has implemented over the past year include land auction reforms, local home purchase restrictions, the banning of private equity investments into residential real estate, and the restricting of land auction premiums to within 15%.

Markets moved by misplaced optimism

Together these measures have successfully curbed speculative activity, but have also exposed the financial fragility of the country’s developers.

As a result, since September, the sector has sold off sharply. The worst of the carnage has, however, been contained within the high-yield segment, and the market has seen only a few defaults among smaller developers and zero bankruptcies among the larger names (Evergrande and Kaisa Group have yet to formally default).

At the time of writing, higher quality names have already begun to bounce back from the late October/early November sell off. This positive shift in sentiment is being driven, not by any profound change in fundamentals, but by the market’s expectations that the government will ease policy, particularly in relation to the three red lines and property loans.

In our view, this optimism is misplaced. Unlike in past cycles, in which government easing created over stimulation, we do not expect this to be replicated this time round. Instead, we expect a slow and gradual easing process as the three- and two-red line policies remain the base line of the government’s long-term policy goal for the property sector.

With a slew of onshore and offshore debt due to mature in December 2021/January 2022, we believe the sector sell-off has a few more months to run before an inflection point is reached.

What is hidden...

We are concerned by the ubiquity of hidden debt within the system, and see this as a potential tail risk in H1 2022. The lack of financial transparency across the sector has created an epidemic of off-balance sheet lending of which it is hard to know who owes what to whom.

For example, ratings agency Fitch informed the market that Fantasia Group Holding – a leading Chinese developer – had only recently disclosed “for the first time” that it had $150m of private bond liabilities that did not appear on its balance sheet or other financial statements.

Such proliferation of ‘unknowns’ adds to our ongoing caution.

On the policy side, we do not expect any meaningful easing activity from the government on the two main tools to curb speculation (i.e. the two and three red lines). Until now, authorities have done ‘just enough’ to manage systemic risk to avoid mass unemployment and protect residential homebuyers as the deleveraging of the sector takes place. We do not believe this ‘just enough’ approach is likely to change in the short or medium term.

As a result, investors with direct exposure to Chinese developers should, in our view, take steps to diversify.

Positioning: why we’re holding out

Within our credit portfolios, we are focused on holding high-quality, higher-beta investment grade names, and high-quality BBs with lower risk of hidden debt and better revenue visibility (as measured by land banks in years).

Amid signs that the market may be getting ahead of itself with regards to policy relaxation, we are holding out for more attractive entry points to emerge over the coming months as more ‘surprising’ missed coupon payments could unfold.

Our goal is to be ready to buy when we believe systemic risk is fully priced in. Meanwhile, we are targeting diversification opportunities through negative screening that identifies companies with the following characteristics:

Potential hidden debt

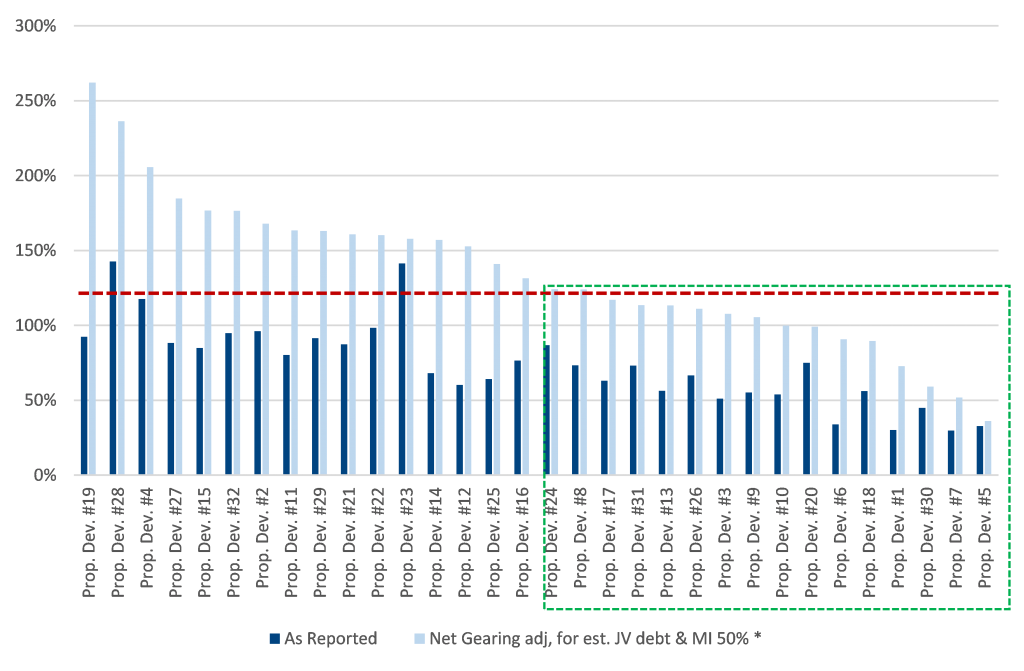

- We achieve this by adjusting for potential put options of minority interests, estimated guaranteed debt at joint ventures, and monitoring increases in payable

Figure 2: Net gearing as of H1 2021 (as reported and adjusted)

‚Prop dev‘ is an anonymisation of the property developers‘ names

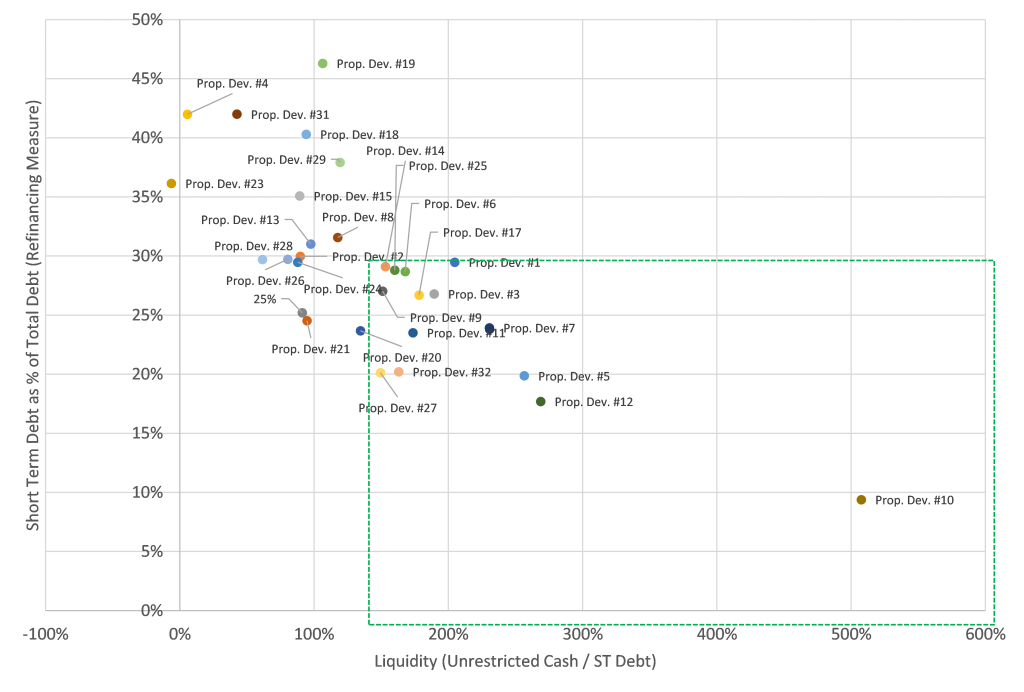

High refinancing risk

- We monitor this by plotting a company’s liquidity against its short-term refinancing needs.

Figure 3: Liquidity vs. short-term refinancing needs

‚Prop dev‘ is an anonymisation of the property developers‘ names

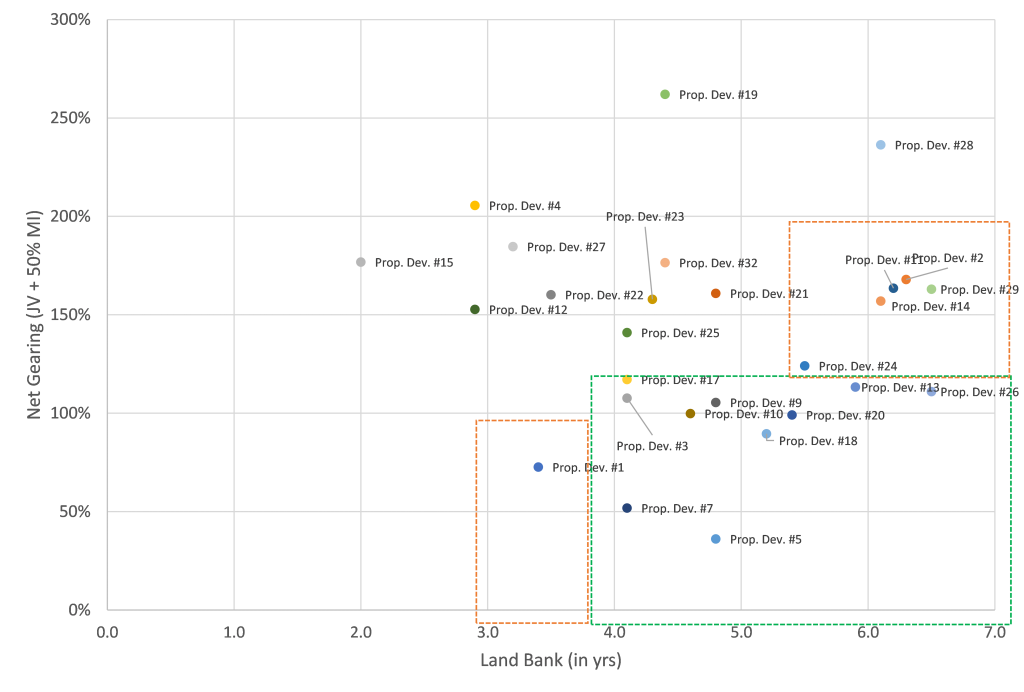

Low revenue visibility

- To judge this, we compare revenue visibility (as expressed in land bank years) to current net gearing.

Figure 4: Highest revenue visibility vs. net gearing

‚Prop dev‘ is an anonymisation of the property developers‘ names

Summary: a conscious uncoupling

In the near term, ramifications from a tighter policy regime are negative for credit, resulting in the potential for:

- More aggressive pricing concessions in the near term to accelerate cashflows and deleverage (as already seen at Evergrande);

- Lower transparency on financials (more joint ventures and off-balance sheet debt);

- A lower growth outlook as debt-funded growth becomes unavailable.

That said, the medium-term ramifications are positive for the sector as a whole and particularly for Chinese high yield property as it will promote healthier balance sheets and lower interest costs long term. It is also likely to favour quality growth and allow for better margins while accelerating sector consolidation.

Overall, the world is witnessing the end of China’s decade-long housing boom, but we believe the era that will replace it will be ‘credit positive’. The industry is in the midst of mass de-risking of its balance sheet and, for investors, this will be beneficial over the mid to long term.

Source: All market data, Bloomberg, unless otherwise stated.