The industry’s bad name is largely the result of intense competition and high capital expenditure requirements putting pressure on share price performance. However, 2021 sparked a renewed interest in the sector, largely in the form of private-equity driven leveraged buyouts (LBOs) and take-privates (the acquisition of a listed company by a special purpose vehicle) by founding owners.

In this discussion, we assesses the four key drivers of this increased interest, the potential revival of telecommunications investments and the implications for credit investors.

Pressure on cash flow and valuations

One of the main factors deterring equity investors from the telecoms sector is its high capital intensity and thin near-term free cash flow (FCF). At present, telecoms faces two major upgrade cycles: 5G mobile (a once every 10-year cycle) which includes both network upgrades and costly 5G spectrum auctions; and fixed-line upgrades (a once every 20-year cycle), replacing legacy copper networks with fibre infrastructure.

Although these upgrade cycles started prior to 2020, the pandemic accelerated the shift towards digitalisation and solidified the importance of high-speed internet connections in everyday life. In turn, operators responded by accelerating their network deployment schedules leading to increased capital expenditure (capex) envelopes and prolonged pressure on FCF.

Additionally, the European telecoms sector is a mature industry with intense competition, amplifying equity pressures. Currently, most European countries operate with three or four established telecoms providers and, quite often, several smaller, regional alternative providers. While regulators encourage competition, telecoms services are becoming increasingly homogeneous with consumers more willing to switch in search of the best value. In turn, this dynamic drives competition, limiting near-term operational growth.

While the current conditions are not attractive to equity investors – who place greater value on near-term cash flow – it does present opportunities for private equity. With its longer investment horizons (typically 5 to ten years), private equity can look beyond the current upgrade cycle to a point when capital intensity comes down and cash flow generation increases.

Equity underperformance drives opportunistic bids

For the reasons mentioned above, over the past six years, European telecoms has seen material weakness in equity prices, leading to a significant underperformance against the wider market. The STOXX Europe 600 Telecommunications index (SXKP Index), a proxy for the wider publicly traded European Telco sector, is down approximately 25% since the start of 2017, a material underperformance when compared to the approximate 32% growth in the Deutsche Boerse AG Germany Stock Index (DAX – a proxy for European equities) over the same period1.

Source: Bloomberg – 06/01/17 – 06/12/21. STOXX Europe 600 Telecommunications index (SXKP); Deutsche Boerse AG Germany Stock Index (DAX).

Past performance is not a reliable indicator of future performance.

Under the hood, stock price devaluations range from negative 30% to 50% for several large incumbent operators, positioning them as prime take-over targets for private equity. To date, stock price declines for operators in the firing line include Telecom Italia (down ~45%, and down ~60% prior to the KKR offer), BT Group (down ~55%), KPN (down ~11% and ~38% at the low), Vodafone (down ~46%) and Telefonica (down ~59% between 3 January 2017 and 3 December 2021) 2.

In turn, these companies are currently trading at depressed enterprise value (EV) to EBITDA multiples of around 5.0x. This is materially below both historical and fair value levels of 6.5x – 8.0x (depending on asset ownership structures). These factors, combined with the additional elements outlined below, are driving the renewed interest and leading to several somewhat opportunistic take-over attempts.

Company | Transaction | Sponsor | Status |

|---|---|---|---|

MasMovil | LBO | Civen, KKR & Providence Private Equity | Completed – 2020 |

Altice Europe | Take-Private | Patrick Drahi (Company Founder) | Completed – 2021 |

Iliad | Take-Private | Xavier Niel (Company Founder) | Completed – 2021 |

KPN | LBO | KKR / EQT – Stonepeak consortium | Failed: Bids Rejected – 2021 |

BT Group | Take-Over | Patrick Drahi | On-going, acquired 12% – 2021 |

T-Mobile Netherlands | LBO | Apax & Warburg Pincus | Completed – 2021 |

Telecom Italia | LBO | KKR | Initial Bid Stage – 2021 |

Sum of the parts greater than the whole?

While the sum of the parts might not actually be greater than the whole, considering depressed equity valuations there is increasing focus on the highly valued infrastructure assets, such as mobile towers, fixed-line networks and data centres, within integrated telecom operators. Asset monetisation, as a form of unlocking value, is a developing sector trend; one that stems from the need to balance capex and leverage, and is supported by the high multiples being paid to acquire such assets (mobile towers: 10x – 20x, and fibre networks: 8.0x – 9.0x EV/EBITDA).

Taking Telecom Italia as an example, in November 2021, KKR presented a take-over bid that valued the business at EUR10.7 billion. As per our calculations, beyond the domestic service business, Telecom Italia has a potential value unlock in the region of EUR10.5bn (based on the assumed valuation of their Brazilian operations, mobile towers and fixed line infrastructure stakes), which could increase further if its data centres were included. This presents private equity firms with additional cash-generating opportunities should they need to accelerate investment returns.

Ample ‘dry powder’ in a low-interest rate environment

As estimated by S&P Global, as of January 2021, US private equity dry powder (unspent cash that is available to invest) was at an all-time high of $1.9tn, with as much of $300bn ready to be deployed in Europe. Couple this with extremely low borrowing costs, you create an environment of ample liquidity, investors searching for yield and an undervalued telecoms sector.

This environment, along with the factors outlined above, has seen several successful European telecom LBOs, a few ambitious attempts as well as an increase in take-private transactions involving the enterprise’s founding owners buying out minority equity stakes. The rationale behind these transactions often references each discussion point above, creating somewhat of a blueprint for private equity investors to follow. As such, we expect the increased sector interest to continue into 2022.

Implications for credit investors

Risks and opportunities

As credit investors, navigating this new environment of heightened LBO activity presents both challenges and opportunities. The most immediate risk relates to reactionary movements in credit spreads post take-over announcements. As LBO funding typically involves a combination of equity and debt, usually weighted towards debt, the immediate consideration is ‘how much debt will the new owner put on the balance sheet?’. In anticipation of this scenario, credit spreads widen to reflect the expectation of higher leverage and potential rating downgrades.

Regarding portfolio management, there are typically two scenarios linked to positioning: an unexpected take-over or an expected take-over announcement. In the former, scenario analysis is required to determine potential post-transaction organisational structures and financial policies. This analysis allows us to determine the fair value of the debt instruments under the new structure, adjusting our positions accordingly. In the latter, anticipating a take-over event presents an opportunity to capture the negative spread movement by entering credit default swap (CDS) contracts ahead of the anticipated announcement.

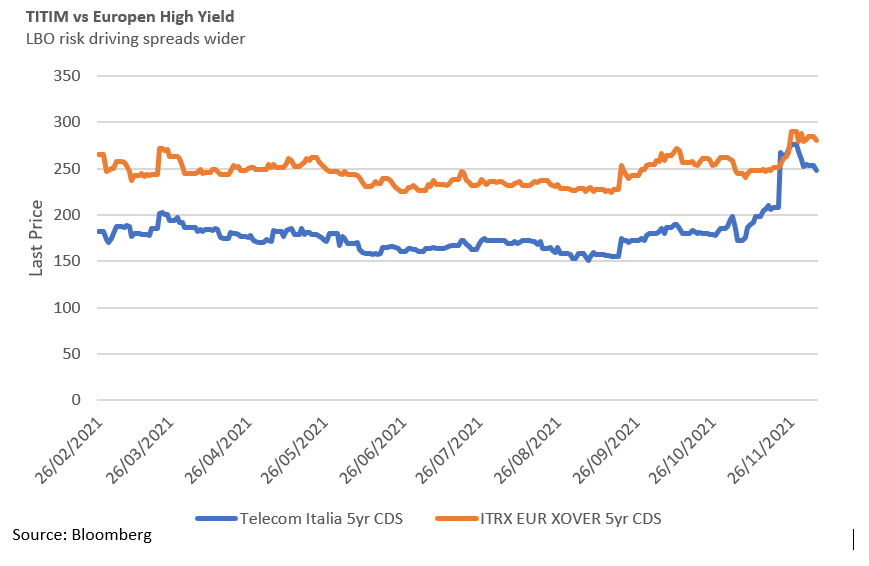

In the example of Telecom Italia, KKR’s offer for the business in its entirety was a surprise, with many expecting an increased investment stake in the company’s fixed-line network. Consequently, following the announcement, Telecom Italia’s 5-year credit default swap (CDS) widen approximately 70 basis points (bps), to roughly 280bps from 210bps prior. Although numerous scenarios exist for the outcome of this transaction, our analysis concluded that, should the deal go ahead, it would most likely increase leverage above 4.0x, positioning the company in line with low-BB / high-single B peers.

We concluded that, as of 25 November 2021 with spread levels of 280-300bps, there was limited further downside should the deal complete and leverage increase in line with expectations. However, should the deal collapse, we expect that spreads will tighten back towards levels seen prior to the announcement (200bps). Additionally, should KKR announce a deleveraging strategy based on asset sales, spreads would likely tighten with reductions in leverage. As such, at the time, our positioning remained the same, given the positive upside/downside analysis in relation to spread levels.

Source: Bloomberg, 26 November 2021

Past performance is not a reliable indicator of future performance.

All market data is sourced from Bloomberg unless otherwise stated