This just in: The Interstellar Express reports that a vast cache of data has been recovered from Quantum Gravity Well (QGW) 3.14159 that could shed new light on an ancient, defunct civilisation.

Understood to originate from the spacetime region known, in local terms, as ‘Earth’, the information – yet to be fully translated – appears to reference financial conditions over a brief but turbulent period, according to sources familiar with the anti-matter.

“As far as we can tell,” the source says, “the data shows market fluctuations during the two Earth years labeled as ‘2021’ and ‘2022’.”

The rare find follows a number of technical tweaks to the QGW fields that have increased the stability and scope of the time-scanning instruments searching for signs of intelligent life in the universe – past, present or future.

Ironically, the QGW fields are based on an idea first proposed by Earth scientists Albert Einstein and Nathan Rosen in 1935 (local calendar measure): that “bridges” exist in spacetime. While originally dismissed as fanciful, physicists Kip Thorne and Mike Morris later showed that such bridges – or “traversable wormholes” – were indeed possible using a quantum phenomenon known as the ‘Casimir Effect’1.

Figure 1. The wormhole effect

In the first tranche of the translated ‘Earth Extracts’ released today, we paint a confusing picture of financial conditions during the year denominated as ‘2021’:

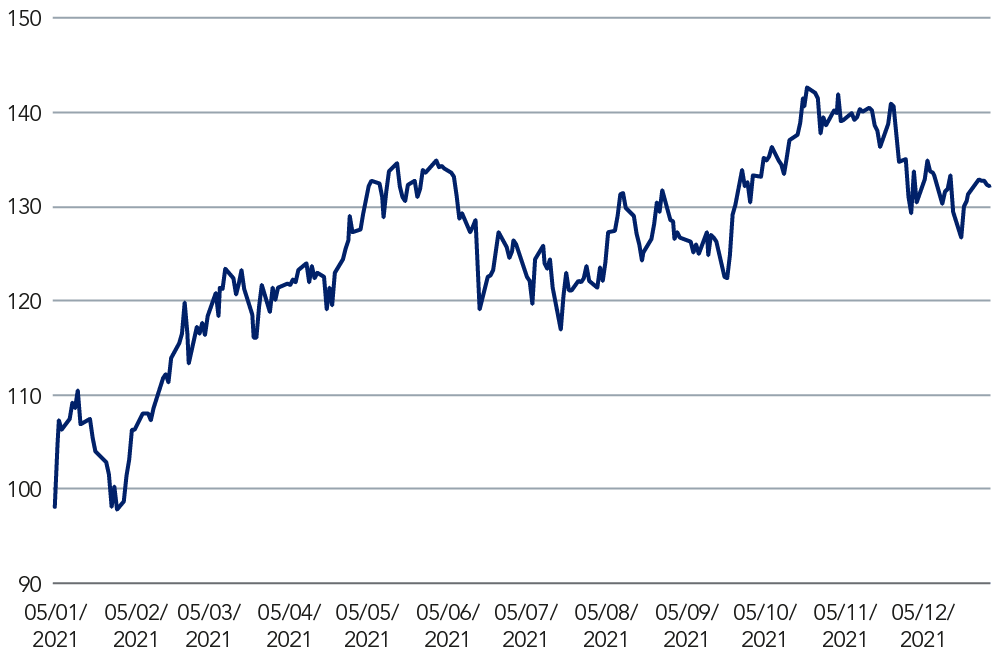

“The benchmark S&P 500 index soared 27% in 20212, suggesting it was easy to make money during the year, especially for passive buy-and-hold investors,” the report says. “However, the static headline annual returns masked significant market turbulence over the 12-month period that saw, for instance, enormous dispersion in financial stocks between sub-sectors, as well as several growth-value mood swings as investors rotated between styles in line with risk-on, risk-off sentiment changes. The chart below illustrates the scale of financial sector volatility for the year…”

Figure 2. Keefe, Bruyette & Woods (KBW) US Bank Index 2021

Source: Bloomberg

“While most financial subsectors actually outperformed the broader S&P 500 index in 2021, some came out better than others, led by investment bank (IB) and broker stocks that rose almost 50% during the year. This result was summed up in a Wall Street Journal headline ‘Thank you Fed’,” the Earth Extracts paper says.

“But on the downside, the payments sector fell 4.7% for the period, while property and casual insurance companies underperfomed the S&P 500 – albeit returning a still healthy 15.6%.”

Earth Extracts point to heightened market uncertainty in 2022, as investors negotiated strengthening cross-currents.

“Investment banks continued to outperform in 2022, supported by successful business pivots that underpinned earnings growth and a healthy return-on-equity (ROE) for most players – even after accounting for the prospects of some normalisation in capital markets activity,” the report says.

“Regardless of such idiosyncratic sector results, markets were largely focused on inflationary fears and an increasingly hawkish tone emerging from the US Federal Reserve (the Fed) and other central banks over 2022. Coming into the year, investors seemed relaxed about the Fed positioning before concerns about central bank surprises or, worse, policy ‘shocks’ ramped up.

“Those fears seemed justifed following the release on January 5 of the Federal Open Market Committee (FOMC) minutes that signaled a sharp shift to a tightening bias at the Fed, as it back-tracked on the previous ‘transitory’ inflation narrative. While the Fed had already announced a faster tapering program and earlier interest rate hikes, the FOMC minutes startled investors with comments indicating the US central bank could start shrinking its balance sheet well ahead of expectations.”

Other snippets released in the Earth Extracts data dump include:

- European financials geared up for higher interest rates in 2022. Betting an upward shift of 100bps across all interest rates would add about 25% to pre-tax profits3 – given the generally low pass-through of higher rates to depositors, some investors may have underappreciated the real earnings sensitivity of the sector. A higher 10-year yield also helped bank multiples;

- Macro factors continued to dominate returns for US life insurers in 2022, reprising the 2021 experience when the sector benefited from rising rates and tight credit spreads. But despite the ongoing boost from higher interest rates in 2022, life insurers struggled to outperform as both equity and credit markets came under pressure; and,

- The Covid-19 pandemic spilled over well into 2022 as new variants (Omicron, in particular) weighed against huge advances in vaccine coverage, herd immunity and new therapeutic drugs during the year.

The Interstellar Express reports, however, some contradictory facts emerging from the Earth Extracts data, particularly in relation to the 2022 period – possibly due to quarkal contamination in the QGW field that entangled alternative universes, according to the source.

Based on the most recent translations, Earth financial markets saw two vastly different outcomes in 2022, suggesting scientists must unravel the information under a dual-universe model (dubbed A and B in the report).

In Universe A it appears the infamous Covid-19 pandemic cleared, spurring the ‘reopening trade’, while the Fed kept inflation under control with well-signalled rate hikes reflected in a steepening curve.

On the contrary, the Universe B result paints a ‘bad macro’ scenario of slowing growth, persistent inflation, bond market panics, flattening yield curves and falling financial stocks as credit concerns hit the sector before it benefited from higher interest rates.

“We don’t know if the QGW results are just noise or true evidence of an important historical regime change in these long-forgotten and obscure Earth financial markets,” the source says. “Only time will tell.”

JBS Haldane, Geneticist (1892-1964)

1 See Michael Morris, Kip Thorne and Ulvi Yurtsever. Physical Review Letters (Vol. 61, No. 13), ‘Wormholes, Time Machines, and Weak Energy Conditions’ (September 1988).

2 Market data throughout this post is provided by Bloomberg.

3 Average based on disclosures from the largest listed banks (Commerzbank, Deutsche Bank, Banco Sabadell, Intesa Sanpaolo and many others).