Auf den Punkt gebracht:

- Der Gesundheitssektor wird aufgrund des anhaltenden Bevölkerungswachstums, höherer Lebenserwartung, verbessertem Zugang, sowie kontinuierlicher Innovation und gestiegener Kaufkraft von Privatpersonen und Institutionen weiter wachsen.

- Biowissenschaftsunternehmen wie Vertragshersteller und -entwickler (CDMOs) und Anbieter von Produkten für das Gesundheitswesen profitieren nicht nur von diesem strukturellen Wachstum, sondern sind auch gut aufgestellt, um einen Nutzen aus langfristigen Trends wie der Verlagerung auf Biologika und dem Bedarf an intensiverer Forschung und Entwicklung (F&E) zu ziehen.

Positive Diagnose: Warum der Gesundheitssektor mit weiterem Wachstum rechnen kann

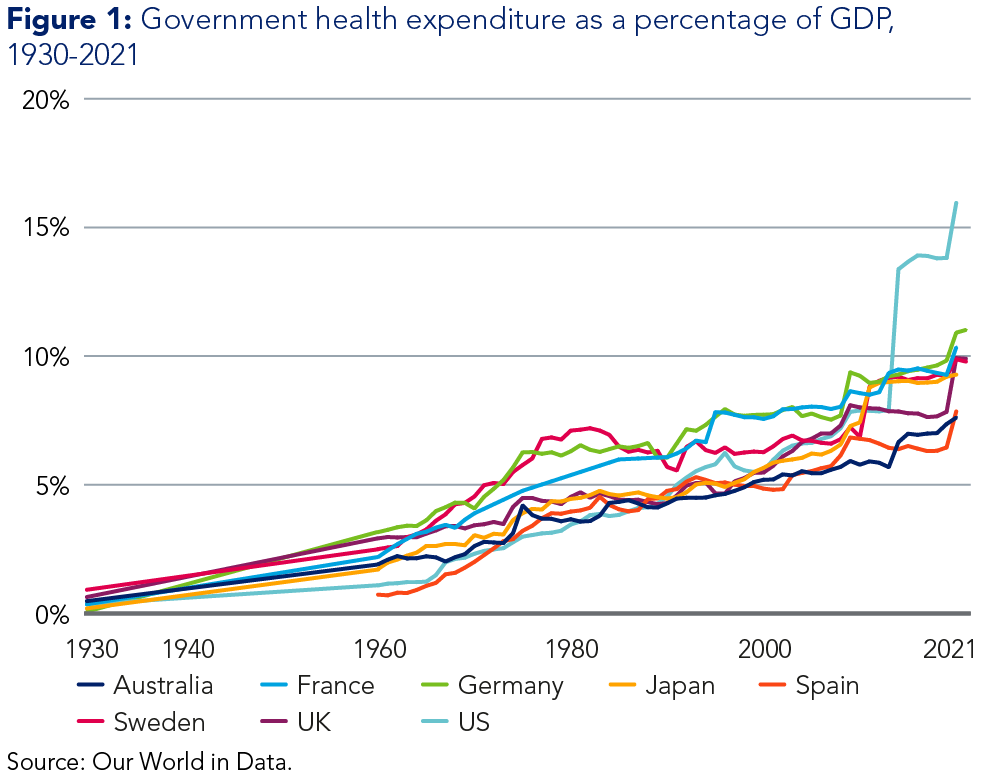

Eine Reihe von Faktoren hat dazu geführt, dass die Ausgaben für das Gesundheitswesen im Verhältnis zum BIP seit den 1960er Jahren kontinuierlich stark angewachsen sind, insbesondere in den Industrieländern. Die meisten dieser Treiber werden auch in den kommenden Jahrzehnten auf dem Markt präsent sein:

- Bevölkerungswachstum: Die Weltbevölkerung hat sich seit Mitte des 20. Jahrhunderts mehr als verdreifacht und erreichte im November 2022 8 Milliarden. Schätzungen der Vereinten Nationen gehen davon aus, dass die Zahl der Menschen im Jahr 2050 bei 9,7 Milliarden liegen und Mitte der 2080er Jahre einen Höchststand von fast 10,4 Milliarden erreichen wird.1

- Lebenserwartung: Die weltweite Lebenserwartung bei der Geburt ist von 46,5 Jahren im Jahr 1950 auf 71,7 Jahre im Jahr 2022 gestiegen; bis 2050 wird sie voraussichtlich 77,3 Jahre erreichen, was zum Teil auf eine verbesserte Gesundheitsversorgung zurückzuführen ist.2 Ein größerer alternder Bevölkerungsanteil führt an sich schon zu einer höheren Nachfrage nach Gesundheitsleistungen.

- Zugang: Der Universal Health Coverage Index (UHC) der Weltgesundheitsorganisation ist zwischen 2000 und 2021 von 45 auf 68 gestiegen (obwohl sich die Verbesserung der Gesundheitsversorgung in den letzten Jahren verlangsamt hat).3

- Innovation: Bedeutende Arzneimittelentdeckungen und neue Behandlungsmethoden für Krankheiten wie Krebs und Diabetes haben die Nachfrage gesteigert. Mit Blick auf die Zukunft wird sich der Einsatz von Technologien wie künstliche Intelligenz, 3D-Druck, Gene Editing, virtuelle Realität und Smart-Bandagen mit beispielloser Geschwindigkeit beschleunigen.4

- Kaufkraft: Sowohl Privatpersonen als auch Regierungen sind in der Lage, mehr Geld für Behandlungen ausgeben. Das Weltwirtschaftsforum schätzt, dass die weltweiten Gesundheitsausgaben zwischen 2018 und 2022 um mehr als 40 % gestiegen sind und 12 Bio. US-Dollar erreicht haben.5

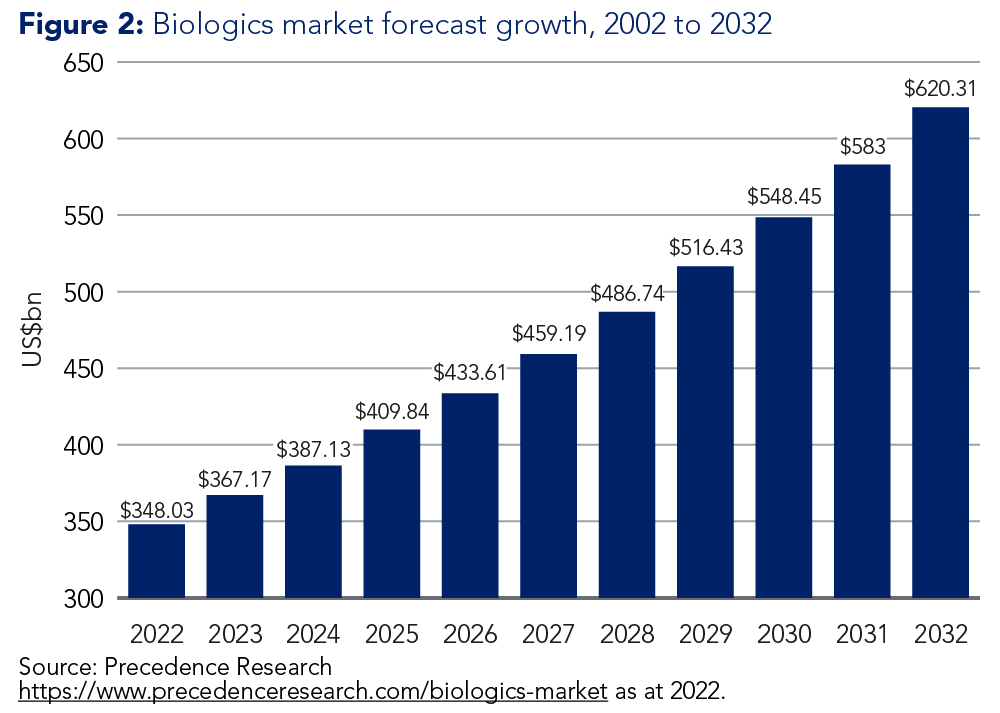

Da die bessere Verfügbarkeit von Gesundheitsversorgung in Schwellenländern erhebliche Chancen bietet, kann der Sektor mit einer kontinuierlichen jährlichen Wachstumsrate von rund 4 % rechnen.

In den letzten 12-18 Monaten wurde das Interesse der Anleger weitgehend durch die Aufregung rund um GLP-1-Medikamente geweckt – die Wundermittel, die ursprünglich zur Behandlung von Diabetes entwickelt wurden, aber auch eine potenzielle Lösung für die weltweit zunehmende Adipositas-Epidemie darstellen. Dieser Enthusiasmus ist zwar gerechtfertigt, hat jedoch dazu geführt, dass andere vielversprechende, langfristige Investitionen im Gesundheitsbereich versäumt wurden. Wir sind der Ansicht, dass der Biowissenschaftssektor und die damit verbundenen Unternehmen eine starke, aber ein wenig übersehene langfristige Chance darstellen.

Wir glauben, dass der Biowissenschaftssektor und die damit verbundenen Unternehmen eine starke, aber ein wenig übersehene langfristige Chance darstellen.

Der Business Case für biowissenschaftliche Instrumente und Dienstleistungen

Neben dem strukturellen Wachstum des Gesundheitsmarktes weltweit profitieren Unternehmen, die sich auf Dienstleistungen und Produkte im Bereich der Biowissenschaften konzentrieren, von zwei zentralen langfristigen Wachstumsthemen.

Thema 1: Die Verschiebung hin zur Produktion von biologischen Arzneimitteln

In der Vergangenheit konzentrierte sich die Pharmaindustrie auf niedermolekulare Pillen oder chemotherapieartige „Gifte“ zur Behandlung von Krankheiten. Im Laufe der Zeit haben diese Ansätze jedoch zu sinkenden Erträgen geführt. Der Sektor bewegt sich zunehmend in Richtung der Kommerzialisierung von monoklonalen Antikörpern, sowie von Therapien der nächsten Generation wie Gen- und Zelltherapie.

Monoklonale Antikörper sind eine Gruppe von Proteinen, die als Immunglobuline bekannt sind; sie sind im Wesentlichen identische Kopien spezifischer Antikörper, die bei der Diagnose und Behandlung von Krankheiten verwendet werden können.

Die Verlagerung hin zur Produktion von biologischen Arzneimitteln ist bereits seit einem Jahrzehnt im Gange, aber es bestehen gute Aussichten, dass sie sich fortsetzt; etwa 70 % der Pipeline-Starts und 40-50 % der Produktion entfallen derzeit auf Biologika, so dass noch viel Potenzial vorhanden ist.

Als komplexere Moleküle erfordern monoklonale Antikörper andere Entdeckungs- und Produktionstechnologien im Vergleich zu herkömmlichen Arzneimitteln. Der Übergang zu Biologika führt daher zu einem hohen einstelligen Wachstum für Unternehmen, die von diesem Megatrend betroffen sind.

Thema 2: Sinkende Produktivität in der Arzneimittelforschung und -entwicklung

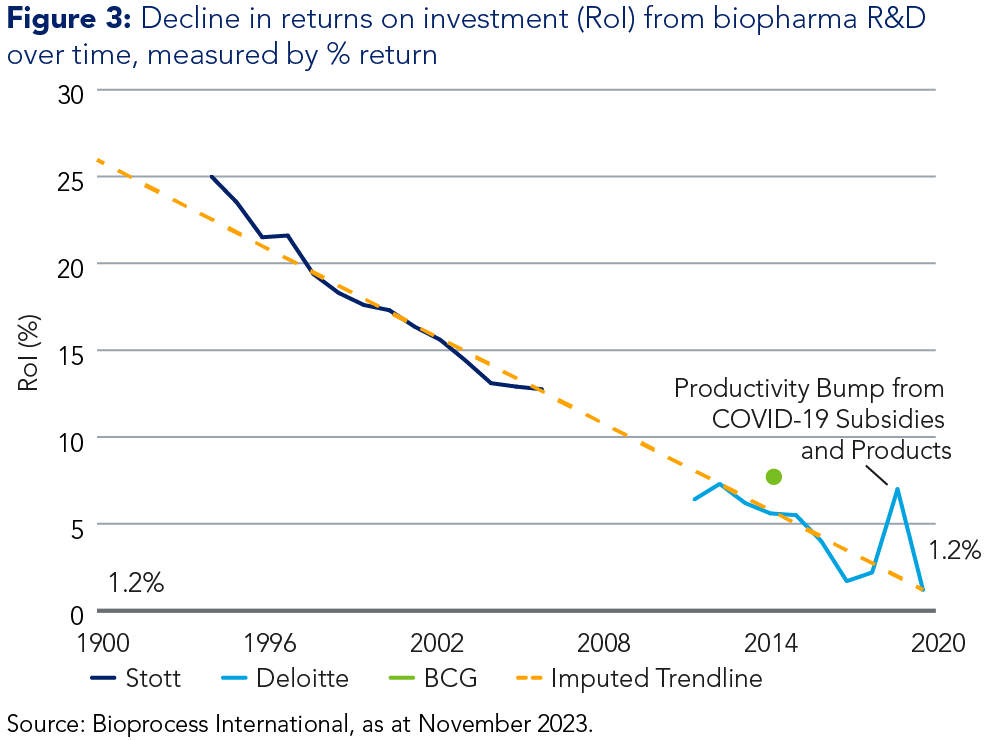

Die Renditen der F&E-Investitionen in der Pharmaindustrie sind in den letzten 30 bis 40 Jahren stetig gesunken. Der konstante Strom von Arzneimittelentdeckungen in den 1980er und 1990er Jahren verlangsamte sich im neuen Jahrhundert, da die zusätzlichen Marktchancen geringer wurden. Damit wurde die Messlatte für die Einführung neuer Medikamente höher gelegt. Gleichzeitig hat sich die Intensität der Forschung, die erforderlich ist, um potenzielle Kandidaten für die Vermarktung zu finden, deutlich verstärkt.

Insgesamt sind die Ausgaben, die benötigt werden, um die gleichen Ergebnisse bei den Arzneimittelverkäufen zu erzielen, erheblich gestiegen. Diese steigenden Ausgaben schaffen einen wachsenden Markt sowohl für CDMOs als auch für Hersteller von Laborgeräten.

Biowissenschaften und Nachhaltigkeit

Der Bereich Biowissenschaften ist im Allgemeinen gut auf positive gesellschaftliche Ergebnisse ausgerichtet. CDMOs und Gerätehersteller tragen dazu bei, die Kosten für die Arzneimittelforschung und die Lieferung neuer Medikamente zu minimieren, und helfen letztlich dabei, die Herausforderungen des ungedeckten medizinischen Bedarfs zu bewältigen.

Die Bemühungen dieser Biowissenschaftsunternehmen tragen direkt zum UN-Ziel für nachhaltige Entwicklung (SDG) 3 bei, das darauf abzielt, ein gesundes Leben und Wohlbefinden für alle Menschen zu fördern.

Nach Angaben der Vereinten Nationen haben die Covid-19-Pandemie und andere Krisen in den letzten Jahren die Fortschritte bei der Verwirklichung von SDG 3 behindert, und die Fälle behandelbarer Krankheiten wie Tuberkulose und Malaria haben zugenommen.6 Unternehmen, die über ein Diagnostik-Portfolio verfügen, setzen ihre Instrumente ein, um direkt zur Bewältigung dieser wichtigen Herausforderungen im Bereich der öffentlichen Gesundheit beizutragen.

Die steigenden Ausgaben, die aufgrund des Bedarfs an intensiverer Forschung erforderlich sind, schaffen einen Wachstumsmarkt für CDMOs und Hersteller von Laborgeräten.

Auswirkungen auf Investitionen

Wir sehen beträchtliches langfristiges Investitionspotenzial bei den leistungsstärksten der beiden zentralen Arten von Biowissenschaftsunternehmen:

- Vertrags-, Entwicklungs- und Fertigungsunternehmen (CDMOs): Unternehmen, die Dienstleistungen für pharmazeutische Unternehmen erbringen, um Arzneimittel zu entwickeln und herzustellen und vom Konzept bis zur aktiven Anwendung zur Verbesserung des Lebens von Patienten beizutragen. Lonza ist ein Beispiel für ein reines CDMO, das derzeit in der Strategie gehalten wird, während Thermo Fisher – auch in der Strategie enthalten – über die Marke Patheon ebenfalls CDMO-Dienstleistungen anbietet.

- Spezialinstrumente- und Gerätehersteller: Hersteller von Instrumenten und zugehörigen Verbrauchsmaterialien, die a) für diagnostische Tests in einem Krankenhaus oder anderen medizinischen Umfeld (sowie für DNA-Verifizierung an Tatorten); b) für biowissenschaftliche Forschung in Einrichtungen wie Hochschulen oder großen Biopharmaunternehmen verwendet werden.

Der Biowissenschaftssektor schnitt in den ersten drei Quartalen 2023 schlechter ab als der Gesamtmarkt, was auf vorübergehenden Gegenwind durch drei Schlüsselfaktoren zurückzuführen war:

- Das Ende des durch Covid ausgelösten Anstiegs der Gesundheitsausgaben

- Eine Finanzierungskrise im Bereich der Biotechnologie, die zu Ausgabenkürzungen bei aufstrebenden Biopharmaunternehmen führte

- Die Schuldenkrise in China, die das Wachstum im zweiten Halbjahr 2023 dämpfte

Die allgemein negative Stimmung gegenüber dem Gesundheitssektor wirkte sich auf eine Reihe von Unternehmen mit soliden Fundamentaldaten aus, darunter auch auf diejenigen, die im Rahmen der Strategie gehalten werden. In Anbetracht der strukturellen Trends sind wir jedoch fest von den langfristigen Chancen für diese Unternehmen überzeugt.

Trotz kurzfristiger Probleme in China sind die Gesundheitsversorgung und die Angleichung an den Standard der Ersten Welt weiterhin ein wichtiges Anliegen im Fünfjahresplan des Landes. Auch in der Arzneimittelforschung will China dem Westen Konkurrenz machen.

Generell dürften der Anstieg der Ausgaben, der Übergang zu Biologika und die verstärkte Konzentration auf die Forschung und Entwicklung von Arzneimitteln starke Triebkräfte für ein lang anhaltendes Wachstum im Gesundheitswesen sein.

Qualitativ hochwertige Biowissenschaftsaktien dürften gut aufgestellt sein, um die Früchte zu ernten und gleichzeitig einen wichtigen Beitrag zu einer nachhaltigeren Zukunft zu leisten.

Sustainable Global Equity, 2023

Archiv:

Hier finden Sie unsere bisherigen Berichte (auf Englisch):

- Sustainable Global Equity, June 2022-23

- Sustainable Global Equity, Q1 2023: China’s ‘great reopening’

- Sustainable Global Equity, Q4 2022: The inflation game changer

Sehen Sie sich dieses Video an, in dem Martin Todd, Portfoliomanager, die wichtigsten Fragen rund um nachhaltige Investitionen beantwortet.

Bitte besuchen Sie unsere Webseite, um mehr zu unserer Strategie erfahren.

Die vorstehenden Angaben stellen nicht alle im Portfolio gehaltenen Wertpapiere dar, und es sollte nicht davon ausgegangen werden, dass die oben genannten Wertpapiere profitabel waren oder sein werden. Dieses Dokument stellt weder eine Aufforderung noch ein Angebot an eine Person zum Kauf oder Verkauf der entsprechenden Wertpapiere oder Finanzinstrumente dar.

1 ‘Population: Our growing population’. United Nations website accessed 19 February 2024.

2 ‘Population Prospects 2022: Summary of Results’. Published by the United Nations Department of Economic and Social Affairs. Accessed 19 February 2024.

3 ‘Universal health coverage (UHC)’. Published on the World Health Organization website, 5 October 2023.

4 ‘5 innovations that are revolutionizing global healthcare’. Published by the World Economic Forum, 22 February 2023.

5 ‘World Heath Day: 8 trends shaping global healthcare’. Published by the World Economic Forum, 5 April 2023.

6 ‘Goal 3: Ensure healthy lives and promote well-being for all ages’, Health – United Nations Sustainable Development.