Fast reading

- The uptake of alternative energy sources – such as nuclear and renewables – is likely to accelerate as governments seek to reduce exposure to hydrocarbon flows in the event of future conflicts.

- With gas supplies constrained, many countries will scramble to secure alternative sources, which may result in gas prices remaining elevated. On the flip side, we expect improved policy support for electrification, leading to increased EV sales.

- GEMs Equity has numerous holdings that should benefit from these ongoing shifts, including India’s PowerGrid, Brazil’s WEG, and China’s CATL.

The war in the Middle East continues to rage, despite efforts to negotiate an end the conflict.

Damage to oil and gas facilities – including Ras Laffan in Qatar, the largest liquified natural gas (LNG) terminal in the world – will likely take a number of years to repair before they can fully resume operations.

In this note, we assess the medium- to long-term consequences of the conflict, which has seen the closure of the Strait of Hormuz, energy prices skyrocket, attacks across the Gulf, and the Iranian regime suffer significant body blows.

In our opinion, the main implications are:

- Shake-up of the status quo in the Middle East

- Changes in global energy security priorities

- Role of gas versus coal

- Alternative energy sources

- Further weakening of EU industrial competitiveness (versus China)

- Potential shift towards low-cost but effective defence equipment.

- Negative impact on global macro outlook – affecting investment cycles, rates, inflation and growth.

Middle East shake-up

Despite the rise in energy prices, the region remains vulnerable to a prolonged conflict amid ongoing uncertainty.

Oil and gas output has been badly hit, although it’s worth noting that unlike its neighbours, Saudi Arabia has been able to shift volumes through the East-West pipeline to the port of Yanbu on the Red Sea.

Gulf countries have invested heavily to develop their economies into regional business and tourism hubs and the conflict will likely have a significant impact on capital flows. The once-booming UAE property market has begun to cool, and deep discounts are likely because of the significant supply of new units. Other meaningful impacts may include:

- A shake-up of the geopolitical backdrop in the region, including the security arrangements that underpin the petrodollar1. We expect Middle East governments to become more cautious and may look to hedge their positions.

We expect capital flows to slow down, moving away from the Middle East and towards other regions, as global investors become more cautious. In the short-term, we expect Gulf sovereign wealth funds to deploy capital domestically rather than invest abroad, partly in response.

Figure 1: FDI into the wider Middle East region*

Energy security

As a net exporter, the US is less impacted by the Middle East crisis.

Many Asian countries have borne the brunt of the fallout with about 80% of the oil and gas passing through the Strait of Hormuz going to Asia2.

This exposure has sent shockwaves across many countries that have limited energy inventory, particularly gas.

In India, authorities have prioritised households over businesses in certain regions. In other countries, governments have sought to put a lid on petrol and diesel prices by reducing taxes and limiting exports.

We expect the Iran crisis to prompt many governments to re-assess their energy security. As a result:

- Coal will remain a key part of the mix, as many Asian countries have large reserves. The share of gas in the energy mix has been increasing at the expense of coal. With a gas shortage expected after the conflict is over, coal will play a crucial role to plug the gap.

- The uptake of alternative energy sources – such as nuclear and renewables – is set to accelerate as governments seek to reduce exposure to hydrocarbon flows in the event of future conflicts.

- In addition, policymakers will seek to create a larger buffer stock of oil and gas to mitigate against any future disruptions.

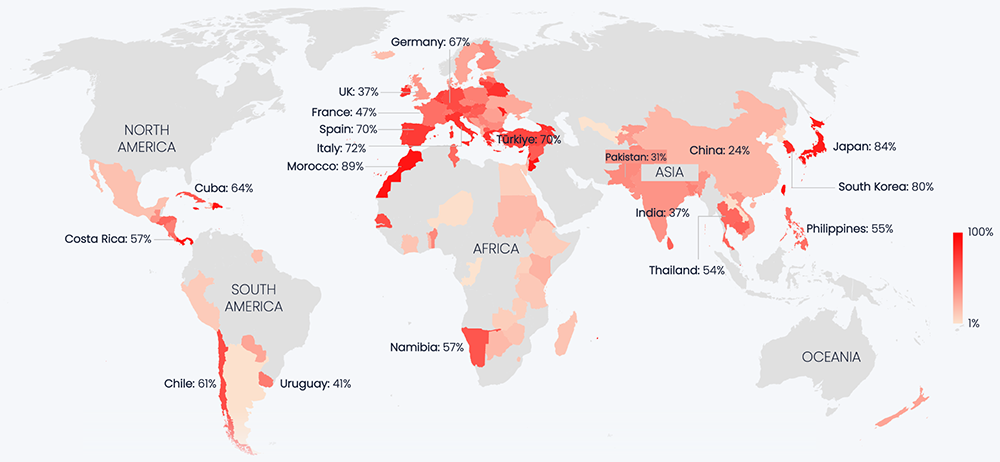

Figure 2: Fossil fuel import dependency is widespread

50 countries import more than half their primary energy as fossil fuels

EU competitiveness

EU gas prices are almost twice the level they were before the crisis.

The EU industrial complex was already struggling from a loss of competitiveness relative to China from the fallout from the Russia-Ukraine war.

With gas supplies constrained, many countries will scramble to secure alternative sources; the EU will compete with Asian buyers, which may result in prices remaining elevated for longer. Such a scenario will increase the EU’s vulnerability, squeeze growth and hinder disinflation.

On the flip side, we expect improved policy support for electrification (which should lead to increased electric vehicle (EV) sales).

Beyond the economic fallout from the crisis, the erratic and bellicose approach of US President Donald Trump continues to test the Western alliance and further strains are likely to emerge.

Figure 3: European gas prices have risen sharply

Defence spending

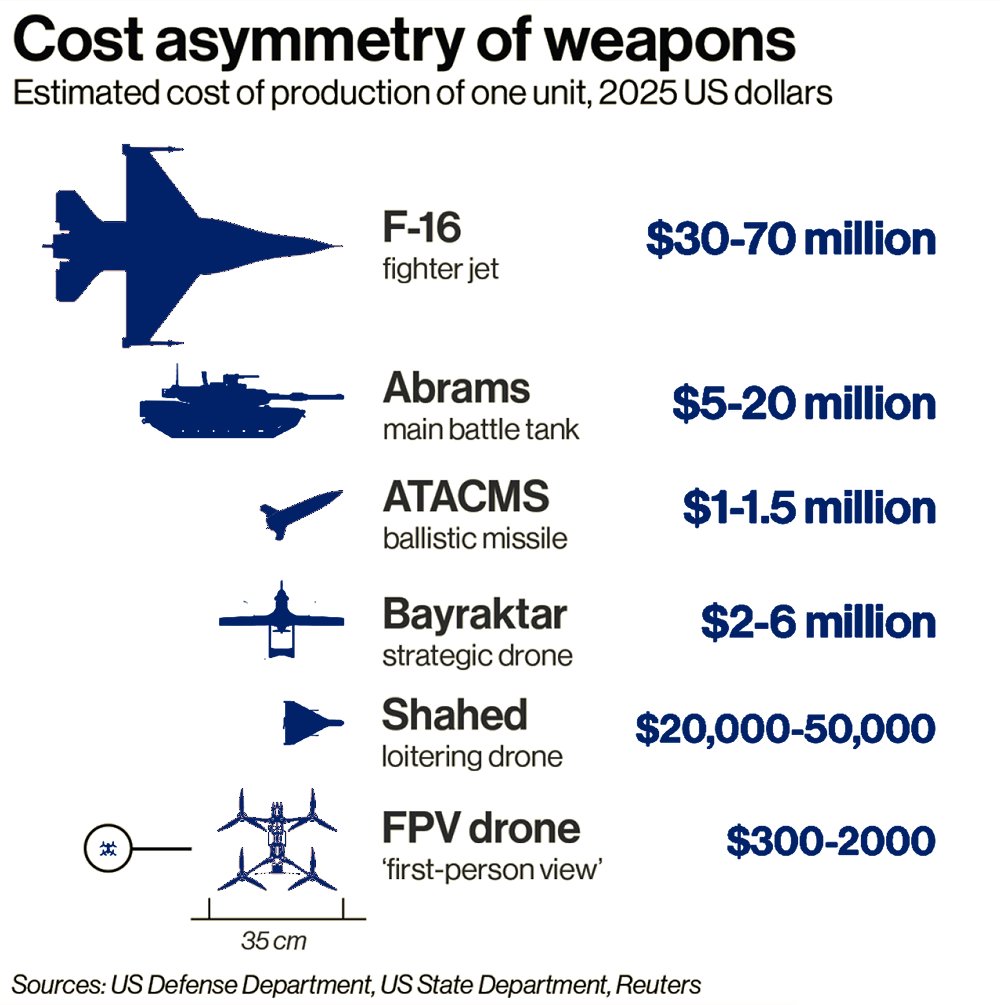

Military conflicts typically lead to increased spending on defence, boosting companies in the sector. The Iran war, however, has highlighted the effectiveness of relatively cheap drone technology, compared to expensive missile interceptor systems.

At times during the conflict, Iranian drones have appeared to overwhelm Western air defence systems.

Going forwards, this economic asymmetry is likely to disrupt traditional military and defence systems, which will drive demand for cheap and effective related tech.

Figure 4: Cost asymmetry of weapons

Global macro outlook

The energy shock has arrived when the global economy has been adjusting to tariff-related uncertainty.

It will only serve to heighten uncertainty further, which will dampen private sector investment and squeeze tight fiscal resources as governments try to mitigate the impact of higher oil prices on households and businesses.

In the last few years, artificial intelligence (AI) has been a principal driver of growth (particularly in the US). Thus far, there have been no indications that the sweeping AI data centre build-out has been impacted by the crisis. However, it is likely data centre plans in the Middle East will get delayed until there is a formal resolution to the conflict.

Investors will monitor how the energy shock has affected the AI build-out. The captive power generation strategies of data centre operators will now be under scrutiny to ensure steady ongoing capex spend.

As noted earlier, the supply of gas from Qatar – which supplies 20% of the world’s LNG – may remain constrained for some time. A number of segments of the global economy will suffer from higher-for-longer energy prices, potentially impacting inflation and the interest rate cycle.

Figure 4: The impact of a higher oil price on inflation

Summary

The global investment landscape is undergoing a structural overhaul driven by geopolitical tensions, economic realignment, demographic shifts, climate challenges, and rapid technological progress.

In our view, companies that can address these pressures while delivering strong profitability and returns on equity are best placed to outperform. Our investment focus, therefore, centres on long-term structural trends rather than short-lived market cycles.

GEMs Equity holdings that should benefit from ongoing shifts:

Power Grid (India)

The Iran crisis is a wake-up call for India as it is hugely dependent on imports to meet its ever-increasing energy needs. The country imports 80% of its oil and 50% of its gas4. India needs to significantly invest in its power and energy infrastructure to support its long-term growth aspirations. PowerGrid, as India’s largest transmission company, is uniquely positioned to benefit from the massive capital expenditure (capex) required in the power sector. As the energy mix shifts toward renewables, transmission capex will have an increasingly important role to play (compared to generation capex).

Rumo (Brazil)

Rumo plays an essential role in Brazil’s agribusiness export engine, offering the most efficient rail‑based logistics solution, linking the country’s major grain‑producing regions to key coastal ports. Rumo’s network provides a significantly cheaper and more reliable alternative to long‑distance trucking, especially given the vast geography and infrastructure bottlenecks across Brazil.

WEG (Brazil)

WEG has long been recognised as a global leader in industrial electric motors, automation and efficiency technologies. In recent years, the company has broadened its portfolio towards clean‑energy solutions, including equipment for wind and solar generation as well as large‑scale battery storage systems. This expansion positions WEG at the centre of the global shift towards electrification and renewable energy. As a consequence of the Iran conflict, many countries will accelerate investment in alternative energy sources. WEG’s broad and technologically-advanced offering across renewable‑energy components, grid‑support equipment and storage solutions provides the company with clear pathway to capture rising investment flows into global clean‑energy infrastructure

GTT (France with more than 50% EM exposure)

GTT occupies a unique position in the global LNG industry. Its core business – membrane‑based containment systems for LNG carriers – has a 100% market share and is supported by decades of accumulated intellectual property and engineering expertise. It creates a wide technological moat that is likely to remain intact for the foreseeable future. A plausible outcome of tensions in the Middle East is that LNG importers seek to diversify away from Qatar into alternative supply routes, which could have a significant impact on shipping intensity. Transporting LNG from the US to Asia, for example, requires roughly 50% more shipping capacity than the global average (and almost three times more than the Qatar‑to‑Asia route)4. This structural increase in tonne‑miles would create the need for a larger global LNG carrier fleet, providing a robust long‑term demand backdrop for GTT’s specialised containment technology

CATL (China)

CATL is the world’s leading battery company, manufacturing EV batteries (for both passenger and commercial vehicles) and energy storage batteries. Even before the current crisis, CATL was growing rapidly – Q4 sales volumes expanded 50% YoY and net profit increased by 57% – and we expect the company to add more than 50% to its capacity in the next 12 months as it increases market share in new markets5. The Middle East conflict will likely only accelerate its growth rate as consumers choose EVs, and governments invest in energy security such as renewables and energy storage systems.

BYD (China)

BYD is the world’s largest manufacturer of EVs, and the second-largest battery maker (after CATL). It released a super-fast charging car battery this year. We expect high oil prices will encourage a sharp acceleration in EV purchases, boosting BYD and its ‘value for money’ proposition. We expect a lot of the company’s growth will be in overseas markets such as Latin America, Southeast Asia and Europe. According to our estimates, BYD makes more than 5x the profit per car in overseas markets compared to domestic markets.

Beijing-Shanghai High-Speed Railway (China)

The Beijing-Shanghai High-Speed Railway owns and operates the 1,318-km line connecting China’s two largest cities. A new 450km/h high-speed electric train – the CR450 – is set to begin operations this year, and should reduce the journey time from 4.5 hours to just over 3 hours. The company competes with airlines covering the route and has about 50% market share of passenger volumes. Higher jet fuel prices will force airlines to hike prices, making the rail route more competitive and further helping it gain market share.

Nari Tech (China)

Nari is the largest supplier of secondary grid equipment – such as dispatch systems, control systems, monitoring systems, grid software, relay protection systems – to the power grid in China. The Beijing government recently announced a huge increase in grid investment as part of its latest five-year plan. On top of this, many other countries are investing heavily in the grid to accommodate more renewable capacity and rising demand because of AI data centres, boosting Nari’s international growth. Higher energy prices will further incentivise grid investment around the world, amid a renewed focus on energy security.

This information does not constitute a solicitation or offer to any person to buy or sell any related securities or financial instruments.

1 Petrodollar: a notional unit of currency earned by a country from the export of petroleum.

2 Don’t lock in future fossil fuel insecurity in response to the Iran war – CEOBS

3 India Targets Import Cuts With Historic Oil and Gas Drilling Campaign

4 bne IntelliNews – LNG supply crunch as carrier orders outstrip shipping capacity

5 Company reports

BD017452