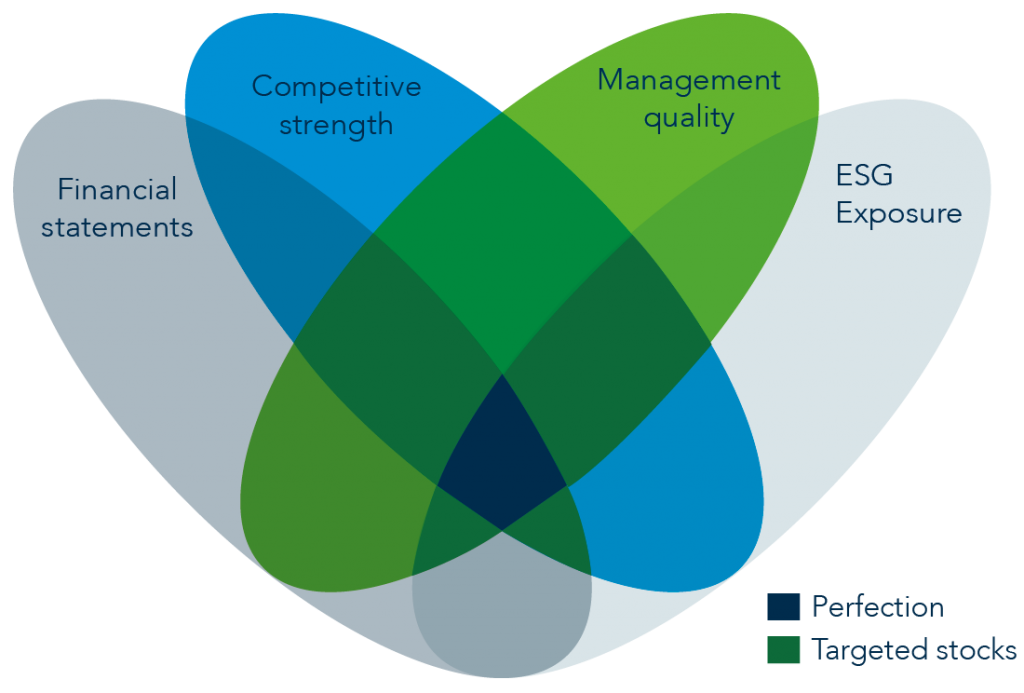

Pragmatism over perfection

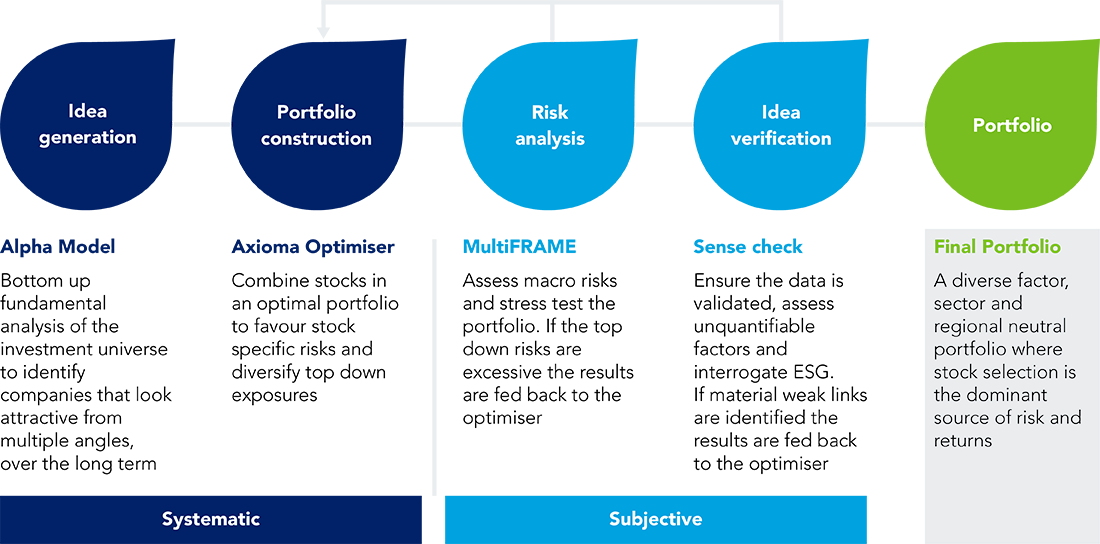

Systematic analysis

Risk management

Geir Lode

Head of Global Equities

Louise Dudley, CFA

Portfolio Manager

Lewis Grant

Senior Portfolio Manager

Head of Global Equities

Portfolio Manager

Senior Portfolio Manager