Fast reading

- ESG ratings consistently show Chinese companies lagging their EM peers on ESG, prompting questions about whether China is investable from an ESG perspective.

- While the ratings do not capture the full picture, there is no doubt that China is challenging for the ESG investor – despite various positive regulatory drivers for ESG in the country.

- Yet the world cannot win the fight against climate change without China successfully transitioning to a low carbon economy. Private investment is critical to help achieve this goal, alongside concerted government action.1

- China, meanwhile, continues to face economic headwinds, not least from the ongoing fallout from Covid-19, its struggling property sector and geopolitical tensions with the US.

- In this context, a bottom-up approach is needed to identify companies showing positive ESG momentum and openness to shareholder dialogue, while playing into long-term structural themes that will deliver sustainable growth.

- For the committed, long-term investor, it is entirely possible to achieve this through in-depth qualitative research and a focus on themes that are set to transform the Chinese economy – notably digitisation, automation, electrification and renewables – all of which have the potential to help achieve the UN SDGs, while addressing China’s social and environmental challenges.

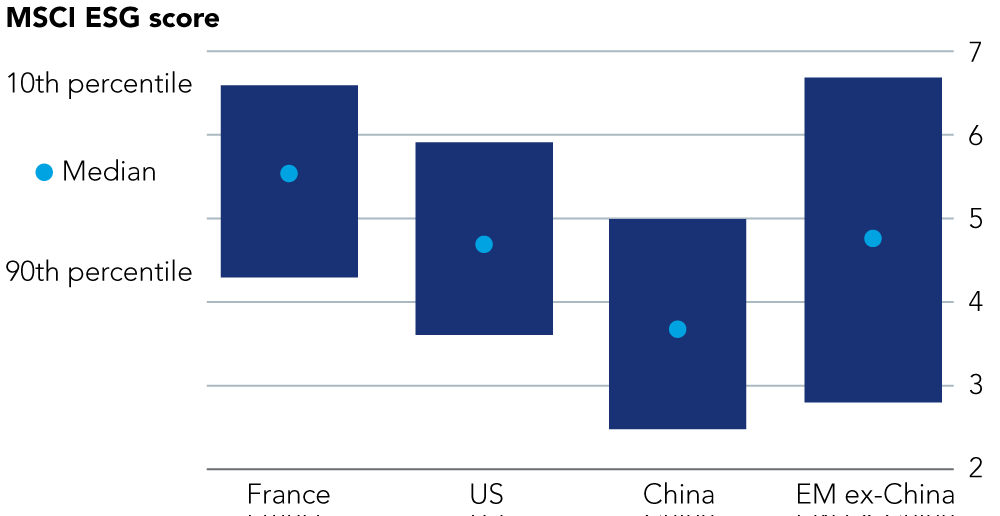

ESG ratings consistently show Chinese companies lagging their EM peers on ESG (see Figure 1) with more controversies, weaker corporate governance scores and red flags concerning human rights, leading to questions about whether China is investable from an ESG perspective.

Figure 1: Median ESG scores are lower for Chinese companies

What is certain, however, is that the ratings do not capture the full picture. Many Chinese companies are penalised for lack of disclosure (understandably); while some global ESG issues can be more or less material in a Chinese context because of local nuances, such as different policy priorities.

One example can be found in the gaming sector, where more attention is given to preventing gaming addiction among adolescents as a response to local policy priorities. Such variations are not well reflected in global ESG frameworks which can also penalise Chinese state-owned enterprises (SOEs)2 that still dominate the economic landscape (71% of Chinese companies listed on the Fortune 500 are SOEs3).

Regulatory action driving ESG gains

While China may not be seen as an ESG friendly market, regulatory action is driving improvements across the sustainability agenda. The country’s most significant achievement over the last 40 years has been the lifting of 800 million people out of poverty through rapid economic growth and government policies to alleviate poverty through the ‘common prosperity’ agenda, targeting regions disadvantaged by geography and a lack of economic opportunities. This change, in itself, has been instrumental in delivering a central aim of the UN SDGs.

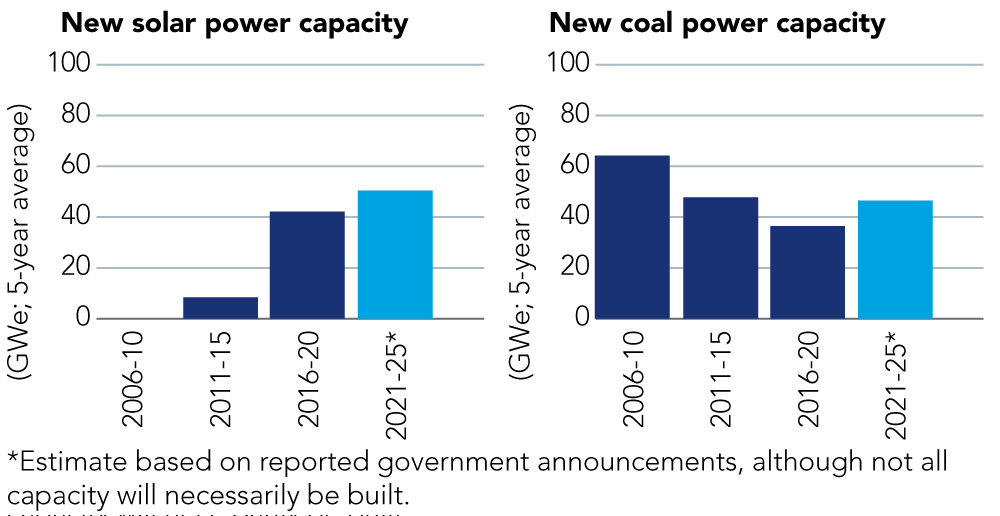

On the environmental side, China remains an undisputed global leader in solar and energy storage technologies and has a sizeable wind turbine manufacturing supply chain. Hydrogen is also set to play a key role in China’s decarbonisation efforts. While the Beijing government continues to order more coal (see Figure 2 below) it is also ramping up new solar capacity which will be instrumental in the country’s bid to reach net zero by 2060.

Figure 2: Beijing government is ordering more solar (and more coal)

Outside of the energy sector, there is considerable government support for investments in energy efficiency improvements and process innovation, which are vital to achieving net zero. Progress on creating a circular economy4 has been slower with the focus mainly on improving waste management, but it is progressing.

Meanwhile, large companies are aligning with the government’s 2030 and 2060 targets with many going further to set 2050 targets (800 companies so far according to the Carbon Trust).5 Supply chain emissions (Scope 3) remain under-reported, yet this a global issue. We have also seen Chinese export-focused firms spurred on by international regulations such as the EU’s Carbon Border Adjustment Mechanism.

On governance, the State Council6 has recently issued guidelines to drive improvements in board composition, including a welcome recommendation that all SOEs have a majority of independent directors and fully independent audit committees. Generally, the government is pushing for more mixed ownership and modernisation of SOEs. We are also seeing improvements in ESG disclosure requirements, with mandatory environmental reporting for high impact companies, albeit less advanced than neighbours such as India (where more comprehensive ESG reporting is mandatory for the top 1,000 listed companies).

The social side is lagging

This progress is unfortunately not matched on the social side, notwithstanding the huge achievements on alleviating poverty through ‘common prosperity’ and some other areas of leadership (eg. protection of minors on gaming platforms, female participation in the workforce).

A recent report by Sheffield Hallam University7 has flagged exposure to forced labour in China’s solar and auto supply chains and the risks have been well documented in other industries such as agriculture.

Working conditions in manufacturing also remain an issue with high employee turnover (reaching 40% in some companies) indicating some underlying challenges. Internal migrant workers are also vulnerable to exploitation since, on migrating to urban areas to take up low paid manufacturing jobs, many still lack access to social benefits under the hukou (household) registration system.

Meanwhile, the ‘996’ work culture8 in the technology sector remains an issue in some areas despite government efforts to address it. Newer social issues – such as digital rights, privacy and surveillance – are also under the spotlight with technology companies coming under scrutiny for their data-sharing policies with the Chinese government.

Vigilance to avoid or mitigate ESG risks

Some of these issues are by no means unique to China (modern slavery, for example, remains a global phenomenon and is reportedly higher in other EM countries9), nevertheless they remain risks that require evaluation, mitigation, and when appropriate, avoidance.

While not all state-owned enterprises (SOEs) are alike, we avoid SOEs in traditional sectors where the risk of political interference is too high (for example, banks, property and heavy industry) and only invest in SOEs that demonstrate due consideration for minority shareholders.

To learn more about responsible investing in emerging markets, read our ESG Materiality report.

1 China accounts for 27% of global carbon dioxide and a third of the world’s greenhouse gases. To reach net-zero emissions by 2060, the World Bank estimates China needs between US$14-17tn in additional investments for green infrastructure and technology in the power and transport sectors alone, and much of this will need to come from the private sector. China’s Transition to a Low-Carbon Economy and Climate Resilience Needs Shifts in Resources and Technologies (worldbank.org).

2 A state-owned enterprise (SOE) is a large organisation created by a country’s government to carry out commercial activities.

4 A circular economy is a type of economic system or model that minimises waste and pollution, maximises resource efficiency and reuse, and designs products and services to last longer or be recycled.

5 Especially across ICT, textile and manufacturing sectors, some businesses are seeking to reach carbon neutrality ahead of national climate targets. Accelerate to Net Zero: a view from China | The Carbon Trust.

6 The State Council is the chief administrative authority of the People’s Republic of China. It is chaired by the premier and includes the heads of each of the constituent departments.

7 Driving Force | Sheffield Hallam University (shu.ac.uk)

8 The 996 working hour system is a work schedule practiced by some companies in China. It derives its name from its requirement that employees work from 9:00am to 9:00pm, six days per week.

9 The Global Slavery Index identifies India, Indonesia and Mexico has having higher rates of modern slavery than China.