Fast reading:

- The healthcare sector is set for continued expansion on the back of ongoing population growth, higher life expectancy, improved availability, continuing innovation and increased personal and institutional spending power.

- As well as benefiting from this structural growth, life sciences businesses such as contract development and manufacturing organisations (CDMOs) and healthcare equipment providers are well positioned to exploit secular trends including the shift to biologics and the need for more intense research and development (R&D).

Positive diagnosis: Why the healthcare sector can expect continued growth

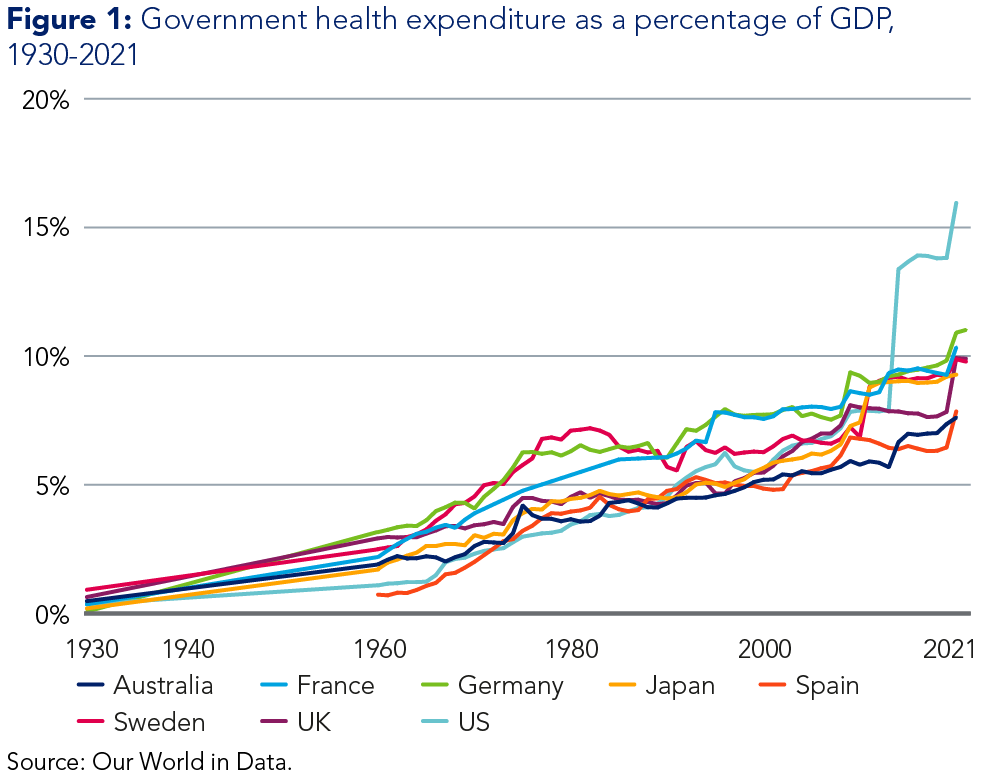

A range of factors have driven significant ongoing growth in healthcare spending as a percentage of GDP since the 1960s, particularly in developed countries. Most of these drivers will continue to be present in the market in the coming decades:

- Population growth: The world’s population has more than tripled since the mid-twentieth century, reaching 8 billion in November 2022. United Nations estimates see it hitting 9.7 billion in 2050 and peaking at nearly 10.4 billion in the mid-2080s.1

- Life expectancy: Global life expectancy at birth rose from 46.5 years in 1950 to 71.7 years in 2022; by 2050 it is expected to reach 77.3 years, partly as a result of improved healthcare.2 A larger aging population in itself creates greater healthcare demand.

- Availability: The World Health Organization’s Universal Health Coverage (UHC) service coverage index increased from 45 to 68 between 2000 and 2021 (although improvements in coverage have slowed in recent years).3

- Innovation: Significant drug discoveries and new methods of treatment for diseases such as cancer and diabetes have boosted demand. Looking ahead, the application of technology including artificial intelligence, 3D printing, gene editing, virtual reality and smart bandages is set to accelerate at an unprecedented rate.4

- Spending power: Both individuals and governments have more money to spend on treatment; the World Economic Forum estimates global healthcare spend increased by more than 40% between 2018 and 2022, reaching US$12tn.5

With improving access to healthcare in emerging market countries offering significant opportunities, the sector can expect an ongoing overall annual growth rate of around 4%.

Over the past 12-18 months, investor attention has largely been captured by the excitement around GLP-1s – the wonder drugs originally developed to treat diabetes but that offer a potential solution to the spiralling global obesity epidemic. While this enthusiasm is justified, it has tended to dominate the narrative to the extent that other dynamic long-term investments within the healthcare arena have been overlooked. We believe the life sciences sector and related businesses represent a strong but somewhat overlooked long-term opportunity.

We believe the life sciences sector and related businesses represent a strong but somewhat overlooked long-term opportunity.

The business case for life science tools and services

As well as the structural growth of the healthcare market globally, firms focused on life sciences services and equipment benefit from two strong secular growth themes.

Theme 1: The shift to biologic drug production

Historically, the pharmaceutical industry focused on small-molecule pills or chemotherapy type ‘poisons’ to treat illnesses. However, over time, these approaches have offered diminishing returns. Increasingly, the sector is moving towards the commercialisation of monoclonal antibodies – as well as next-generation treatments such as gene and cell therapy.

Monoclonal antibodies are a group of proteins known as immunoglobulins; they are essentially identical copies of specific antibodies that can be used in the diagnosis and treatment of diseases.

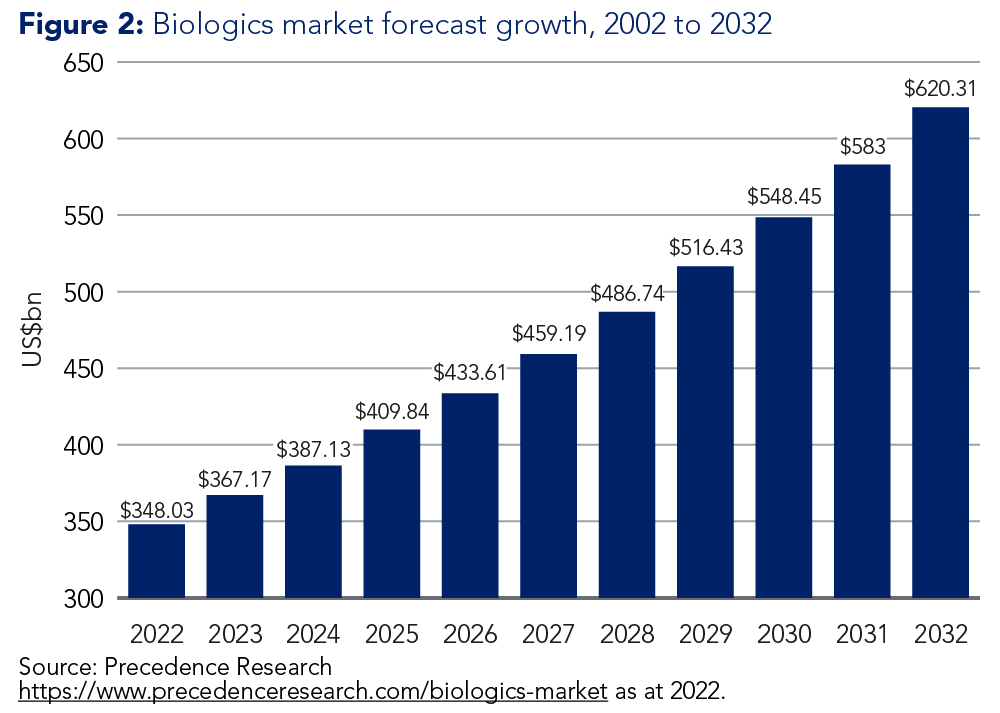

The shift towards biologic drug production has already been in play for a decade, but we have good visibility on it continuing; around 70% of pipeline starts and 40-50% of production are currently biologics, leaving a lot of remaining potential.

As more complex molecules, monoclonal antibodies require different discovery and production technologies from traditional medicines; the transition to biologics is therefore driving high single-digit growth for companies exposed to this megatrend.

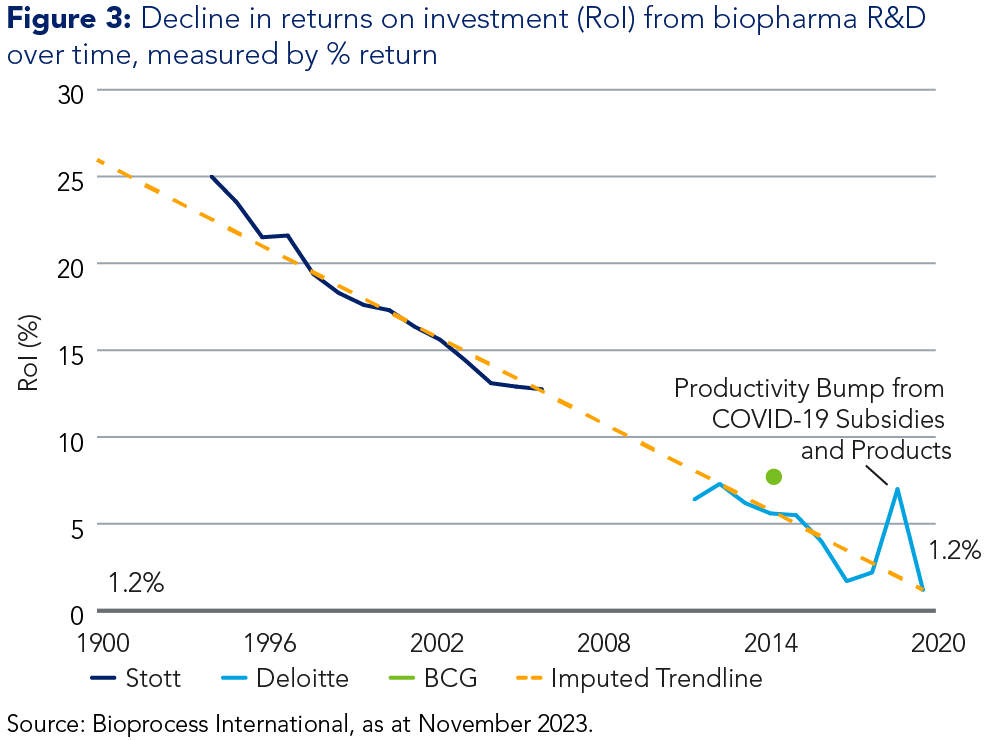

Theme 2: Declining productivity in drug R&D

The returns on R&D investment in the pharmaceutical industry have been steadily declining over the past 30-40 years. A constant flow of drug discoveries through the 1980s and 1990s slowed in the new century as the incremental market opportunity became smaller. This raised the bar to take forward new drugs. At the same time, the intensity of research required to isolate potential candidates for commercialisation has become much higher.

Overall, the necessary spend to generate the same level of output in terms of drug sales has risen significantly. This increasing spend creates a growing market for both CDMOs and laboratory equipment manufacturers.

Life sciences and sustainability

The life sciences sector is generally well-aligned with positive societal outcomes. CDMOs and equipment manufacturers help to minimise the cost of drug discovery and the delivery of new medicines, while ultimately helping with the challenges of unmet medical need.

The efforts of these life science businesses contribute directly to UN Sustainable Development Goal (SDG) 3, which aims to promote healthy lives and well-being for all.

According to the UN, the Covid-19 pandemic and other crises have impeded progress towards Goal 3 in recent years, with increases in treatable illnesses including tuberculosis and malaria.6 Companies with a diagnostic portfolio are using their tools to directly help address these key public health challenges.

The increasing spend required by the need for higher intensity research creates a growth market for both CDMOs and laboratory equipment manufacturers.

Investment implications

We see significant long-term investment potential in the best companies among two main types of life science business:

- Contract, development and manufacturing organisations (CDMOs): Businesses providing third-party services to pharmaceutical firms to develop and produce drugs, taking them from concept to active use in bettering the lives of patients. Lonza is an example of a pure-play CDMO currently held in the strategy, while holding Thermo Fisher also offers CDMO services through its Patheon brand.

- Specialist tool and equipment manufacturers: Makers of instruments and related consumables used for a) diagnostic testing in a hospital or other healthcare environment (as well as for DNA verification at crime scenes); b) life sciences research in discovery settings such as academia or at large biopharma companies.

While the life sciences sector underperformed the wider market in the first three quarters of 2023, this was caused by transitory headwinds from three key factors:

- The end of the Covid-driven boost in healthcare spending.

- A funding crisis within biotech which led to spending cuts by emerging biopharma companies.

- The debt crisis in China, which dampened growth in the country in H2 2023.

Broadly negative sentiment towards the healthcare sector impacted a number of firms with strong fundamentals, including those held by the Strategy. However, given the structural trends in play, we have strong conviction in the long-term opportunities for these companies.

Despite short-term issues in China, healthcare and the levelling up of provision to a first-world standard continues to be a major commitment within the country’s five-year plan. China is also aiming to rival the west in terms of drug discovery.

More broadly, the rise in spending, the transition to biologics and the increased focus on drug R&D should act as strong drivers for long-term secular growth in healthcare.

High-quality life science stocks will be well-positioned to reap the rewards while contributing strongly to a more sustainable future.

Sustainable Global Equity, 2023

Archive:

Please view previous reports below:

- Sustainable Global Equity, June 2022-23

- Sustainable Global Equity, Q1 2023: China’s ‘great reopening’

- Sustainable Global Equity, Q4 2022: The inflation game changer

Watch this video to hear Martin Todd, Portfolio Manager, respond to the key questions surrounding sustainable investing.

Please visit the Strategy’s capability page to learn more.

The above does not represent all of the securities held in the portfolio and it should not be assumed that the above securities were or will be profitable. This document does not constitute a solicitation or offer to any person to buy or sell any related securities or financial instruments.

1 ‘Population: Our growing population’. United Nations website accessed 19 February 2024.

2 ‘Population Prospects 2022: Summary of Results’. Published by the United Nations Department of Economic and Social Affairs. Accessed 19 February 2024.

3 ‘Universal health coverage (UHC)’. Published on the World Health Organization website, 5 October 2023.

4 ‘5 innovations that are revolutionizing global healthcare’. Published by the World Economic Forum, 22 February 2023.

5 ‘World Heath Day: 8 trends shaping global healthcare’. Published by the World Economic Forum, 5 April 2023.

6 ‘Goal 3: Ensure healthy lives and promote well-being for all ages’, Health – United Nations Sustainable Development.