Fast reading

- With the below-1.5˚C target increasingly looking unlikely, investors are moving beyond a narrow decarbonisation narrative and embracing a broader mandate focused on adaptation: ensuring systems can withstand rising temperatures, mounting climate volatility, and accelerating electrification demand.

- Global energy sector investment is projected to reach US$3.3tn in 2025, reflecting governments’ efforts to reduce reliance on imported fossil fuels and protect energy security amid geopolitical tension.

- Our private equity focus is on proven, growing companies operating in attractive niches, typically with asset-light models, clear customer ROI and exposure to decarbonisation, efficiency, compliance or risk mitigation drivers.

Our approach

At Federated Hermes Private Equity, we have been making climate transition-focused investments for over a decade. Our investment process is underpinned by a thematic framework based around megatrends, combining demographic, technological and societal shifts which are reshaping the world in which we live. These shifts are disrupting established business models and markets across industries and creating significant investment opportunities.

With global warming below 1.5˚C looking unlikely, investors are moving beyond a narrow decarbonisation narrative and embracing a broader mandate focused on adaptation: ensuring systems can withstand rising temperatures, mounting climate volatility, and accelerating electrification demand. This requires capital to shift toward the enabling layers of the economy such as power infrastructure, water systems, data‑driven efficiency, and the services that keep these critical assets resilient.

The climate transition landscape is broad, incorporating sectors such as electrification, decarbonisation and digitalisation. Within this universe, we have observed the emergence of a renewed focus on ‘resource resilience’ as a key theme in a time of increasing geopolitical uncertainty: investments in technologies, services and critical infrastructure underpinning the transition towards a more resilient and resource-efficient economy.

Why ‘resource resilience’ now

Global energy sector investment is projected to reach US$3.3tn in 20251, reflecting governments’ efforts to reduce reliance on imported fossil fuels and protect energy security amid geopolitical tension. A catalytic driver of this shift is the onset of the ‘age of electricity’, with growing demand from industry, cooling, transport, data centres, and artificial intelligence (AI). Electricity sector spending alone is set to reach US$1.5tn in 20252, now exceeding oil, gas, and coal combined.

Climate‑tech trends reinforce this pivot: 2025 saw climate investment rise to US$40.5bn3, up 8% year‑on‑year, driven largely by demand for power‑hungry AI infrastructure and grid flexibility solutions rather than by pure decarbonisation plays.

While renewables continue to scale rapidly, infrastructure remains a critical constraint.

While renewables continue to scale rapidly, infrastructure remains a critical constraint. Grid investment, at roughly US$400bn annually4, has consistently lagged the US$1tn deployed into new generation capacity, leaving more than 1,650 GW of wind and solar awaiting connection in 20245. It is estimated that grid capacity will need to grow by over 50% by 2050 to meet net-zero trajectories. Connection queues, permitting delays, and shortages of transformers and cables are now among the most material brakes on the energy transition. This imbalance has increased the strategic value of companies that support the modernisation, upgrade and maintenance of electricity networks. Additionally, opportunities exist in grid digitalisation, allowing better monitoring and improved efficiency.

The IEA’s Clean Energy Equipment Price Index reached a record low in early 2024 (down 60% over the decade6), with solar and battery prices continuing to decline. These trends helped to drive US$127bn in clean‑energy supply‑chain investment in 2025.

Similarly, the falling cost of solar has led to a surge in distributed systems across emerging markets (EM).

Water systems are also rapidly becoming a central pillar of the resource resilience thesis. The global water and wastewater treatment market is forecast to grow from US$351bn in 2025 to US$591bn by 2030 (approx. 11% CAGR)7, fuelled by technological developments such as nanofiltration, AI-based monitoring and smart metering.

Accessing ‘resource resilience’ via private equity

We believe private equity is uniquely positioned to scale the enabling layers of the transition, particularly in the lower mid-market, where investors can access smaller, dynamic businesses with greater governance and control than in many public markets. Our focus is on proven, growing companies operating in attractive niches, typically with asset-light models, clear customer ROI and exposure to decarbonisation, efficiency, compliance or risk mitigation drivers.

This approach prioritises buyout and growth buyout opportunities where transformative capital can support commercialisation, scale-up, and operational improvements, while avoiding early-stage science risk, consumer fad risk and hype-driven green valuation premia. In our view, the lower mid-market offers a compelling balance of targeted thematic exposure and financial discipline, supported by rigorous underwriting, diversification and careful partner selection.

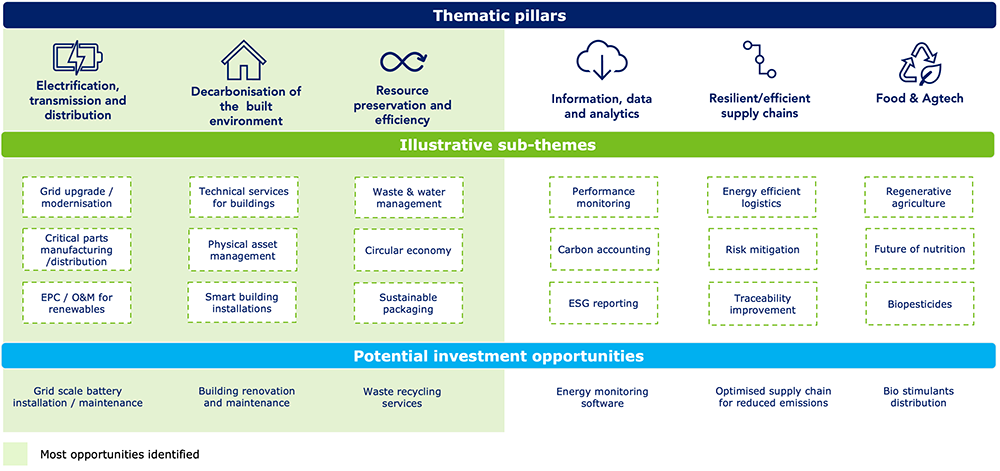

Investment opportunities within ‘resource resilience’ can be evaluated across six principal thematic pillars, with a particular emphasis on the first three sub-themes: electrification, transmission and distribution; and decarbonisation of the built environment, alongside resource preservation and efficiency. These align particularly well with businesses operating in the lower mid-market.

Figure 1: Investment opportunities within ‘resource resilience’

To date, our investment team has backed a range of businesses supporting the energy transition, decarbonisation efforts and the environmental data ecosystem. These include an electric vehicle (EV) charging infrastructure engineer aligned with transport electrification and the UK’s 2035 ICE phase-out; a sustainability consulting and software platform that strengthens corporate environmental reporting; and a provider of gas compliance and energy transition services to housing associations and local authorities, acting as a strategic enabler of UK public sector ambitions to decarbonise ageing housing stock and improve energy performance certificate (EPC) ratings.

The portfolio also includes a US MIT PhD spinout providing diagnostics and carbon tracking solutions to improve property efficiency, as well as a Polish cloud analytics business serving public, scientific and research institutions, including the European Space Agency (ESA). The latter’s infrastructure supports large-scale satellite data analysis, including applications in climate and carbon monitoring. The team has also recently backed an independent distributor of wind turbine spare parts for wind farm operators, providing procurement, refurbishment, logistics, repair coordination and a multi-brand online marketplace for components.

Conclusion

At Federated Hermes, we view the climate transition as a long-term megatrend that remains central to our investment approach. Our emerging focus on resilience builds on this foundation, ensuring we remain aligned with the transition while sharpening our attention on the next critical phase: adaptation, reliability, efficiency, and overall system performance.

By directing capital toward areas with the greatest potential for risk-adjusted impact, we aim to capture compelling economic opportunities while reinforcing the resilience and sustainability of the real economy.

For information on Private Equity

BD017885