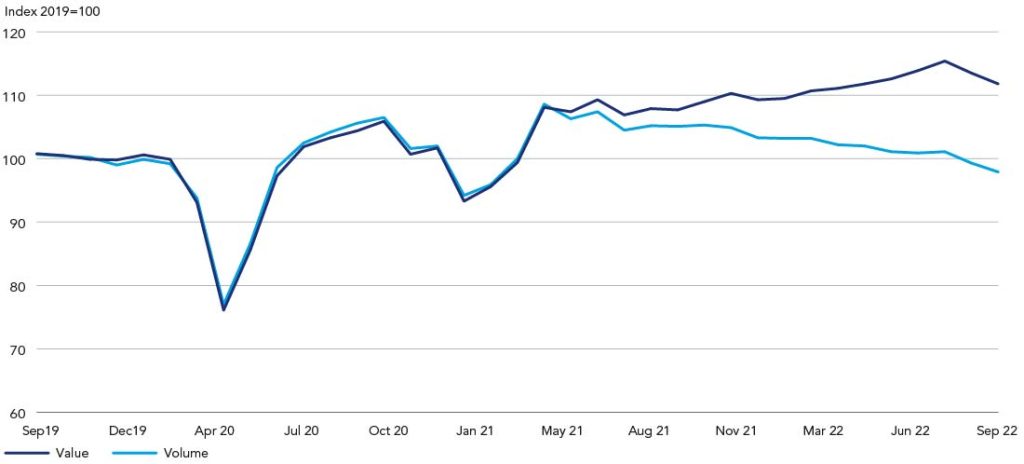

The economic outlook continues to weaken amid political and financial market turmoil. UK retail sales declined more than expected in September with volumes down by 1.4%, driven by rising prices and the cost of living crisis – and further exacerbated by the unplanned bank holiday heralded by the state funeral of Queen Elizabeth II. This follows a downward trend seen throughout 2022.

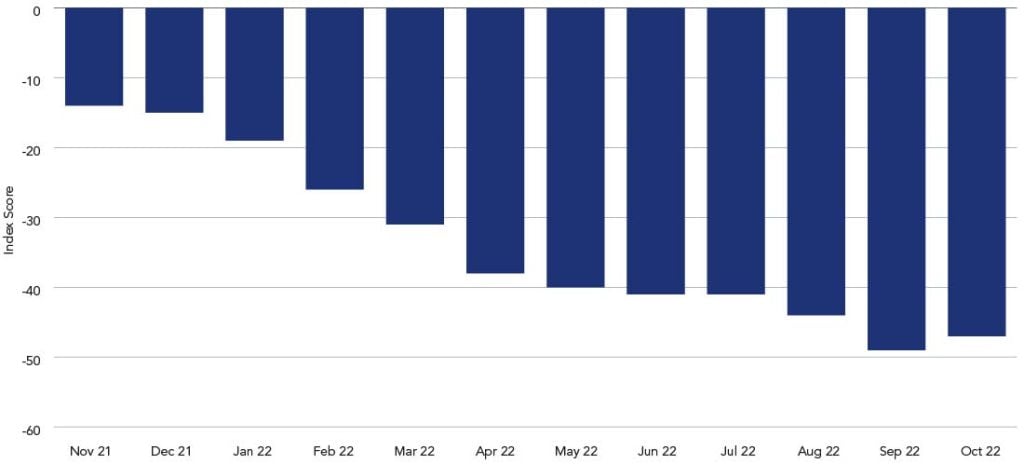

Despite a marginally better reading in October, consumer confidence remains despairingly weak on the back of September’s record-low index score1. In an unwelcome continuation of the year’s bleak economic prospects, UK households face rising food and energy inflation, as well as mounting fears of tougher austerity measures following Rishi Sunak’s appointment as prime minister. The psychological impact of these uncertainties on consumers is concerning for the retail sector, ahead of a crucial Christmas holiday season.

Figure 1: UK retail sales volume falls below pre-pandemic levels

Figure 2: UK consumer confidence remains depressed

The view across the pond

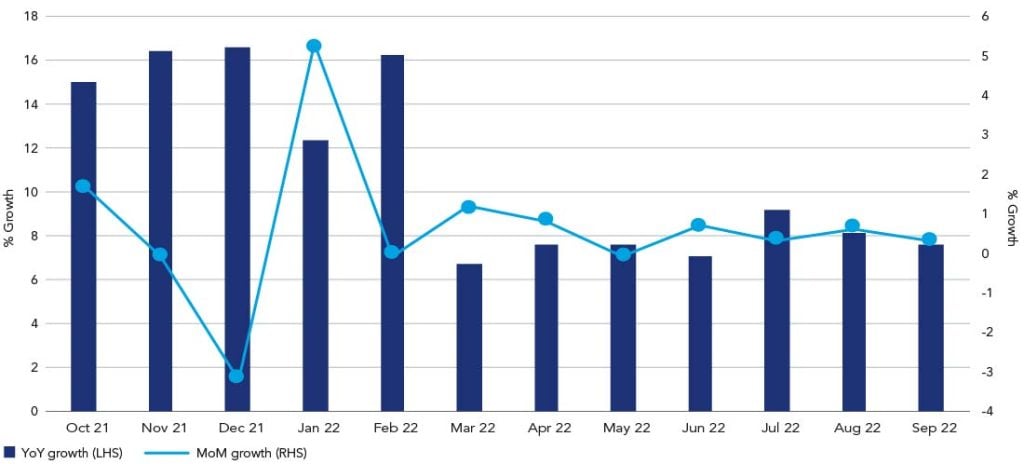

Looking to the US economy, at first glance it appears to have remained stronger in comparison with other major economies. Despite this, our base case is that the US will experience a mild recession around the middle of next year. Retail sales for September (excluding motor vehicle and gasoline stations) increased slightly month-over-month, and were 7.5% higher year-on-year. However, when adjusting for inflation, there was a decline – inflation stood at 0.4% month-over-month, and 8.2% year-on-year.

Consumer sentiment remains weak, and we expect spending will moderate as inflation shows no signs of abating, and tighter monetary policy takes a toll on consumption. Additionally, savings generated by households during the Covid-19 pandemic seem to have unwound, with personal savings rates standing at 3.1% in September, vs. a 33.8% peak in April 2020.

Figure 3: US retail sales (excluding motor vehicles and gasoline parts)

Figure 4: US households have been tapping into their savings

Non-food retailers face challenges

Many retailers in the US and UK have issued profit warnings in recent months driven by a mix of lower demand, continued supply chain challenges, and cost pressures. So far, retailers have managed to pass on the higher costs through pricing but, as consumers economise, it will become harder to avoid price surges.

Inventory levels in the sector remain high; companies have increased stock to cope with supply chain issues, resulting in an excess of unsold merchandise. We expect to see a boom in promotional activity this holiday season, as retailers turn to bargains to sell off additional stock and appeal to budget-conscious shoppers. For consumers searching for the best deals, shopping will begin early to benefit from key promotional days, such as November’s Black Friday.

The current rate environment is another challenge for retailers in both the UK and US, as borrowing costs increase. Nevertheless, we see this mainly impacting lower quality companies, with high levels of floating debt and those financing front end maturities. The estimates from Moody’s suggest that if the one-month LIBOR increases to 4-5%, half of retailers in the US rated B2-B3 will have interest coverage below 1.5x compared to around 30% today.

In addition to this, the strengthening of the dollar will impact cost prices for UK retailers, as many clothing factories price goods in dollars. However, most retailers will likely only start to feel the effects of this in 2023, as most will have already hedged currency requirements for this year.

On a more positive note, the easing on capacity constraints, and dollar freight costs easing in certain places, can partly mitigate the negative pressures retailers are experiencing.

The 2022 Christmas outlook

In the 2021 holiday season, consumers were keen to spend as they benefitted from pent-up demand and the easing of pandemic restrictions. This time around, we expect soft real growth for retailers, characterised by consumers’ search for promotions. This will translate into tighter margins for companies and will likely result in higher leverage metrics driven higher by diminished earnings power. Higher quality companies will focus on controlling costs; for example, hiring fewer seasonal workers, and managing inventory to minimise the impact on margins and optimise their liquidity position. Expectations are low, so there is a chance that companies will outperform their already lowered outlook.

Taking these challenges into consideration – our expectations of earnings being pressured, leverage ticking up and considering the cyclicality of the sector – we remain cautious and selective of the non-food retail sector. Our positioning is weighted towards companies in the higher-quality end of the high yield spectrum and investment grade with good liquidity, predominantly fixed rate debt, and those not facing significant near-term maturities.