Markets see-sawed this week as investors awaited key US labour data, which will indicate if the economy has started to cool, and whether US Federal Reserve will seek to address stubbornly high inflation with faster and higher interest rate rises. At a two-day hearing in Washington this week, Fed chair Jay Powell said the US central bank was willing to return to more aggressive policy tightening but stressed that no decision had yet been made1.

“The Fed’s approach is being watched like a hawk,” says Geir Lode, Head of Global Equities, Federated Hermes Limited. “Investors are wondering how hard the foot on the gas pedal will be to avoid a downturn.”

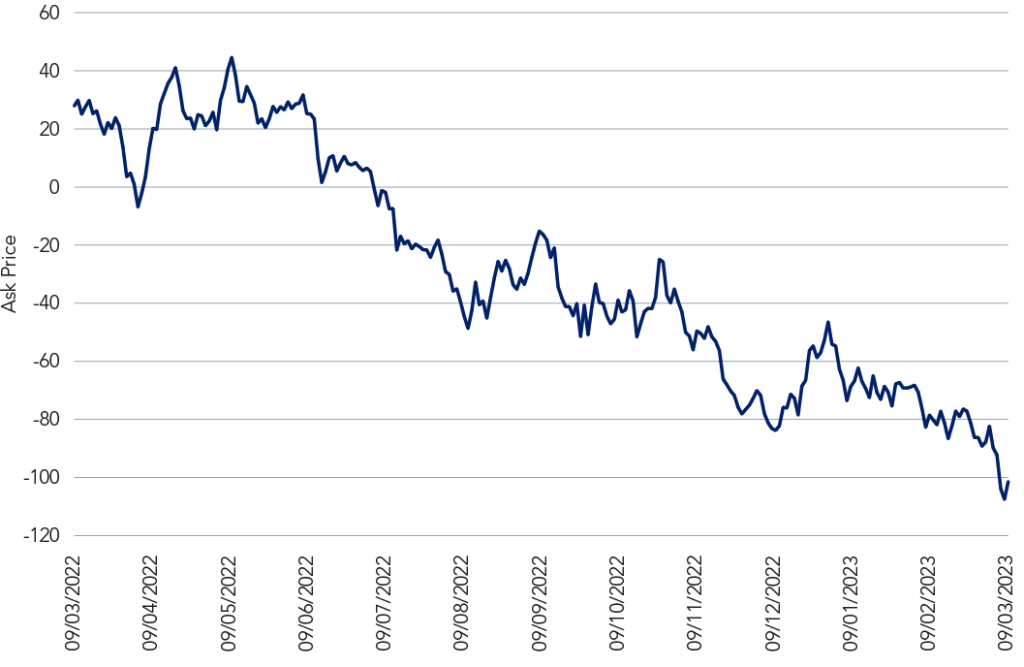

An inverted yield curve, in which yields on short-dated bonds are more than those of longer-dated bonds, is often viewed as a harbinger of recession. The yield on the two-year US treasuries hit highs not seen in more than a decade this week, jumping above 5%, while the yield on the 10-year US treasury hovered below 4% at 16:30 GMT on Thursday2.

“It’s the first time in four decades markets saw a full percentage point discount,” Lode says.

Figure 1: The yield curve measuring the difference between two-year and 10-year US treasury yields surpassed negative 1% this week for the first time since 1981

“During his semi-annual testimony to Congress, Fed Chair Powell provided hawkish remarks on the short-term trajectory of monetary policy. He suggested that the strength of economic data justifies a higher terminal rate, emboldening market expectations of an upward revision to the Fed’s dot plot at the upcoming March meeting,” says Silvia Dall’Angelo, Senior Economist, Federated Hermes Limited.

Markets have begun to price in a 50bps rate rise in March but are awaiting key economic data, notably Friday’s non-farm payrolls numbers, which will reveal if the US economy has started to slow. Short-term rates markets now expect a peak rate of 5.6% in Q3 2023, compared to 5.1% in the Fed’s December forecasts, Dall’Angelo adds.

US job openings declined slightly in January but still far outnumber available workers, indicating significant tightness in the labour market, according to data released this week by the US Labor Department3.

ECB divisions

In contrast, European Central Bank (ECB) officials have publicly disagreed over the pace and extent of tightening going forward. Some members have urged for more aggressive action in light of concerning developments in inflation, while others have stressed declining headline inflation and risks to economic growth.

Eurozone inflation fell less than forecast to 8.5% in the year to February, from 8.6% in January, prompting expectations of a further increase in interest rates because of persistently rising prices4 .

“Despite recent downgrades in eurozone Q4 GDP, high consumer and wage inflation will dominate the ECB’s thinking. For now, a 50bps rate hike is a done deal for March, and more might follow,” Dall’Angelo adds.

The Fed’s approach is being watched like a hawk

“With demand weakening, we expect pressure on corporate revenues to increase at a time when inflation is still persistently above central bank targets,” says James Rutherford, Head of European Equities, Federated Hermes Limited. “As a result we expect profit margins to decline, something that has often been the prelude to a recession.”

European shares closed down on Thursday following a bumpy week’s trading, with Norway’s OBX down 0.9%, Switzerland’s SMI falling 0.69%, and the UK FTSE 100 down 0.63%5 .

For further insights on inflation and fixed income please see our 360°, Q1 2023 report.