The financial ecosystem is in a flap.

Inspired by technology, egged on by regulators and energised by youth, new-breed financial barbarians now gather in force at the gates of tradition, threatening chaotic rebellion in a world built on the promise of predictable stability.

If the 20th century financial system prided itself on boring conservatism – epitomised by entities such as the bank, the building society, the life insurance company, ‘The Man from the Pru’ and the mutual society – the tech-enabled challengers, lumped under the broad ‘fintech’ label, operate under different rules.

In the fintech universe ‘move fast and break things’ holds more cachet than the Bank of England motto ‘Sic vos non vobis’ (or ‘thus we labour but not for ourselves’ for those not fluent in Latin).

And even though we can see the coming storm, it’s not clear yet how the once steady-state financial system will adapt to the swirling vortex of disruption bearing down on incumbents.

Flight plans disrupted

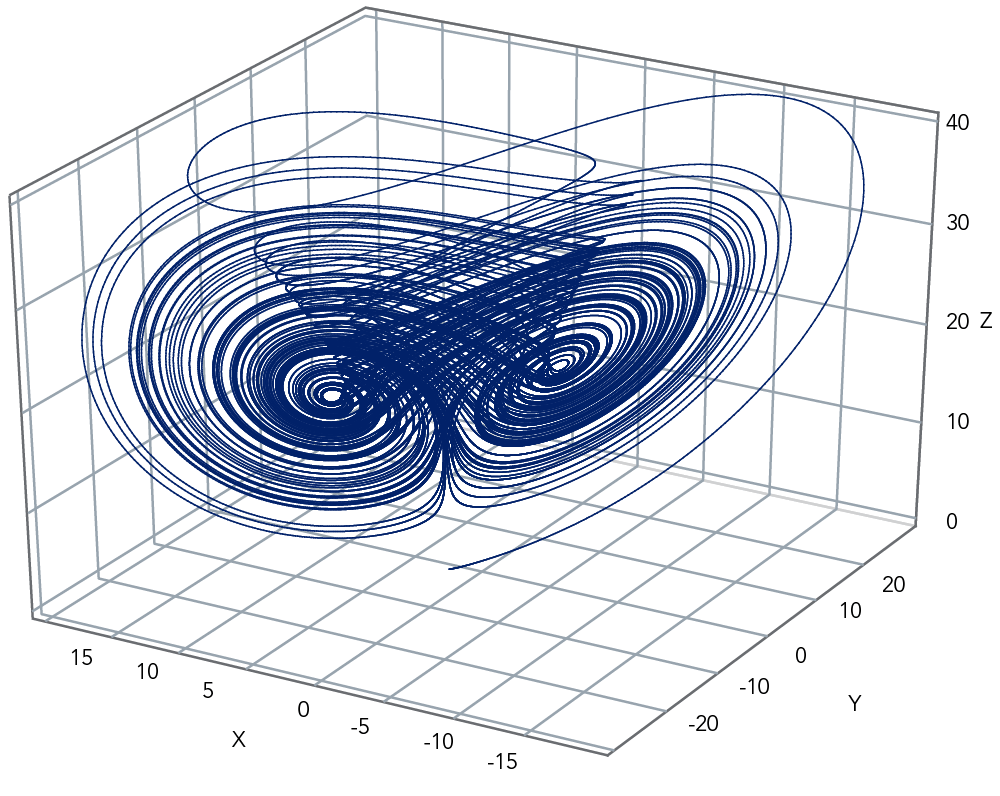

As MIT professor and metereologist Edward Lorenz defined it, chaos abounds when “the present determines the future, but the approximate present does not approximately determine the future”.

Lorenz was the first to show that dynamic systems may evolve in a deterministic fashion with visible patterns evident in detailed data while remaining rigorously random from a coarse-grained point of view: in other words, we can’t predict the future from a rough idea of present conditions.

His mathematical modelling proved that determinism and randomness, far from be opposite, can be utterly compatible.

Not many people may have read his influential 1963 paper, ‘Deterministic Nonperiodic Flow’ but the Lorenz theory gained widespread popularity as the ‘butterfly effect’ – or the idea that the flap of a butterfly’s wings can dramatically change long-term weather outcomes (known in maths-speak as ‘sensitive dependence on initial conditions’).

Based on various limiting factors, the Lorenz equations can be expressed in a visual format (as below) that has the synchronistic satisfaction of resembling a butterfly.

Figure 1. Lorenz oscillators

New arrivals breeze in, banks fly to digital

Given the kaleidoscope of fintechs currently fluttering through the financial system, neither incumbents nor independent observers should feel too confident about predicting longer-term industry outcomes.

As media gush about noveau banks – variously described as neo, digital or challenger – or tag the ‘tech’ line to a swarm of start-ups buzzing around the formerly dull enclaves of insurance or financial regulation and the like, investors are also piling into the sector.

Typically operating in unregulated grey areas, these upstart companies are attracting an ever-increasing amount of investment as market players take bets on the fintech potential to both deliver returns and disrupt traditional financial structures.

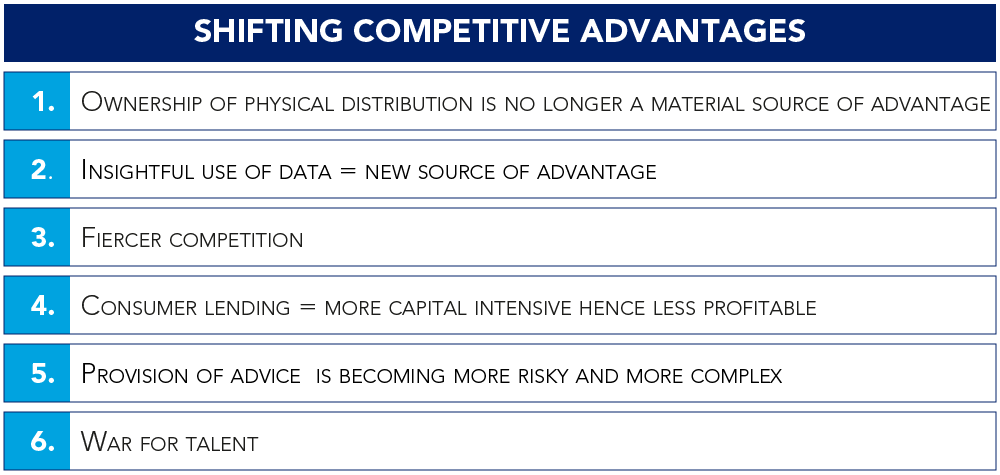

Incumbent banks have certainly woken up to the danger – as illustrated in this recent seven-point synopsis of the changing market dynamics published by one of the ‘big four’ Australian financial institutions, ANZ.

Figure 2. Competitive advantage shifting

Source: Federated Hermes, elaboration on ANZ, FY21 Results Set

Point one in the ANZ list is self-evident. Consumers today are inured to electronic payments and will, if forced to, track down an ATM rather than join a bank queue to withdraw cash.

Matt Hammerstein, Barclays UK chief, put the situation succinctly as: “Fifty years ago, almost 90 per cent of all transactions took place inside a branch, but today that number is less than 10 per cent.”

The inexorable consumer trend has seen bank branches disappear from high streets across the developed world, with Europe no exception.

European Central Bank data warehouse numbers show the CAGR 1997-2020 of branch numbers as: (8.2%) in the Netherlands, (4%) in Germany, only marginally down in Italy (0.3%).

Everything, it seems, is turning digital as banks address a number of intransigent business concerns such as:

- a high cost/income ratio

- the need to improve customer engagement; and,

- keeping fintechs at bay.

By contrast, digital-only start-up banks can bootstrap convenient, quick and affordable banking services under a business model unencumbered with the legacy baggage of old-school institutions.

Traditional banks, in turn, have invested heavily to improve products and services to counter the fintech challenge. Despite some early wins, the new entrants, too, must ultimately convert their rapidly expanding customer ranks into profits.

Cue revolution: open banking floats third-party hopes

Box 1: Open Banking (PSD2)

The European Union (EU) adopted the ‘Second Payment Services Directive’ – or PSD2 – in 2015, which was transposed into national legislation in 2018 and, after delays, implemented in 2021.

PSD2 upends the traditional bank-customer value chain – that previously offered asymmetric benefits to incumbents – by allowing the transfer of customer financial data ownership from the institutions to business and individual clients via open application programming interfaces (APIs).

Customers can now choose between banks or third-party providers (TPPs) – other banks or authorised non-banks – to carry out payment instructions. Clients must give TPPs prior agreement to access accounts in a major boost to consumer power in the banking relationship.

Open banking is escalating the threat for the banking industry as PSD2 both encourages new entrants while enabling all TPPs to offer value-adding product enhancements.

For instance, PSD2 has already prised open the European small-to-medium enterprise (SME) market to the growing hordes of entrepreneurial financial services operations.

Europe and the UK host more than 24 million SMEs – defined as having 250 or fewer employees – in what has long been a lucrative playing ground for established banks. Banking competition remains much tighter in the European/UK larger company sector where only 44,000 or so entities met the threshold (250 plus employees) in 2017.

Just a few years since inception, the PSD2 regime has clearly introduced a strong competitive element with over 100 TPPs offering services to the European SME market as at 2020, across three main categories:

- lending (fast application process);

- payments (invoicing, smooth B2B transactions); and,

- customer data services such as onboarding or loyalty programmes.

After many decades of relatively stable ‘initial conditions’ in a highly regulated, closed-shop environment, banking is entering a new era as several factors – including technological advances, changing customer preferences, regulatory pressure and investment flows – add uncertainty to the equation.

In an increasingly dynamic system, investors must be prepared for a wider range of outcomes in the banking sector, remembering the lesson from Lorenz that patterns emerge out of chaos.

The next Fiorino will explore the subtle interaction between determinism and randomness in a few financial names in our credit portfolio.

We’re watching for butterflies.

Robert Frost (1874-1963), American poet.