The longest equity bull market in history (at least for the US) came to an end on the 19th February, just a couple of weeks short of its 11th birthday. In the midst of our pandemic crisis, Eoin Murray, Head of Investment at the international business of Federated Hermes, refreshes his study on bear markets in order to understand their characteristics and prospective recovery profiles.

We have previously suggested that this pandemic crisis has provided an exogenous shock to our economic and financial system – for this reason, we find it most valuable to think about how it might unfold through that same viral lens.

From shock to consequence

During crises, markets typically go through a number of discrete phases, and this one need be no different. First markets moved into phase one, “the initial shock” – at this stage, markets capitulate en masse, risk assets collapse as correlations head to unity and governments and central banks respond with policy triage that they hope will stave off (some of) the damage.

Phase two, “the consequences”, brings pause for thought, as investors consider the second order effects, before enjoying a brief false dawn rally, also referred to sometimes as “the dead cat bounce”. However, upon further reflection, investors ponder third round effects and decide that they were in fact right initially and further market consolidation ensues. Phase two can recycle multiple times and this is where I believe we are now.

Lastly, we wait for the post-bear phase, or in this case, the post-virus phase, in which the recovery begins and investors can take pause to reflect on a longer-term outlook and begin to contemplate the precise nature of the changes and fractures that will follow. For this phase to start, we would need greater certainty around herd immunity (together with mass testing) and/or significant progress towards the development of a viable vaccine.

Historical bears

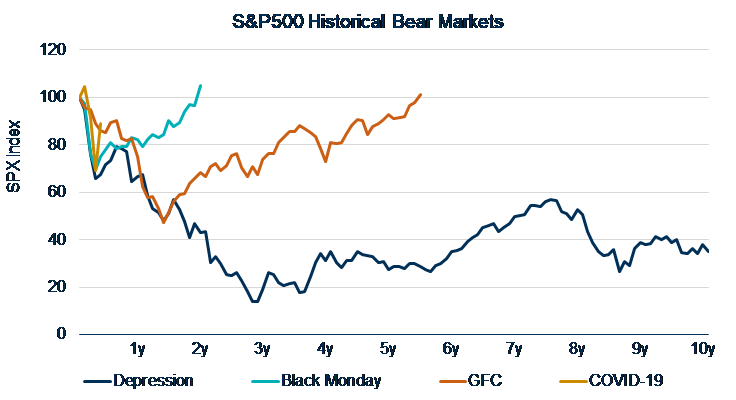

There is no question that we have been enjoying a relief rally, and we can reflect on some of the underlying reasons. We can start by looking at four of the best-known bear markets and seeing their respective rallies, in comparison to today’s pandemic crisis.

Figure 1: Historical Bear market comparison

Source: Bloomberg, Federated Hermes International

Of course, there will be subtle differences in this time of unprecedented uncertainty, as there is a total absence of guidance available from past examples due to the medical nature of our current situation, but perhaps the broad elements of the standard playbook will still hold true.

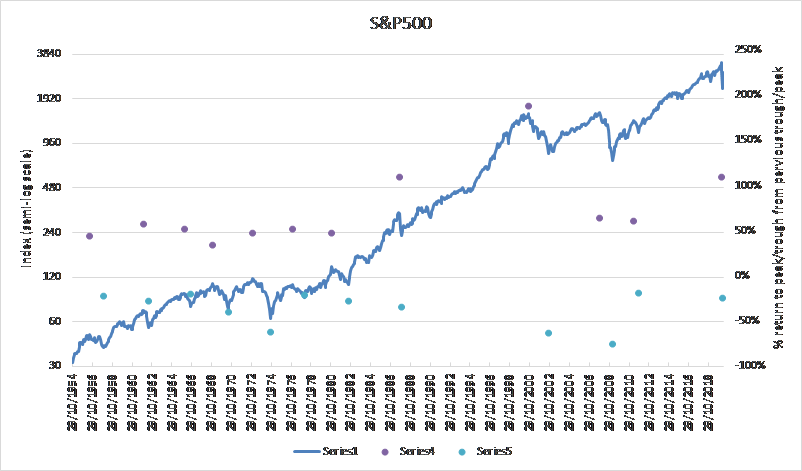

US stocks bounce back

Figure 2: Bull and bear markets

Source: Bloomberg, Federated Hermes International

There’s no such thing as a bear market without a bear market rally. We’re in the middle of that now– since the mid-March lows, US large cap stocks have gained back c.56% of the losses, technically lifting them back into a new bull market (+c.25.5%), even if we’re still in a world that is defined by the extreme uncertainty for the global economy and on the outlook for corporates.

So deep pullbacks are a common feature of markets in the immediate aftermath of crises, and this particular bear has been no different on that front.

Despite the recent gains made by US large caps, we think it’s likely a stretch for investors to chase the move much higher from here. The market cares about cumulative losses and time taken to recoup earnings. Assuming a 25% fall in US equity EPS in 2020 and a 20% recovery in 2021, that should leave the nominal level of corporate earnings 10% below their pre-Coronavirus peak and forward-looking multiples looking frothy relative to history.

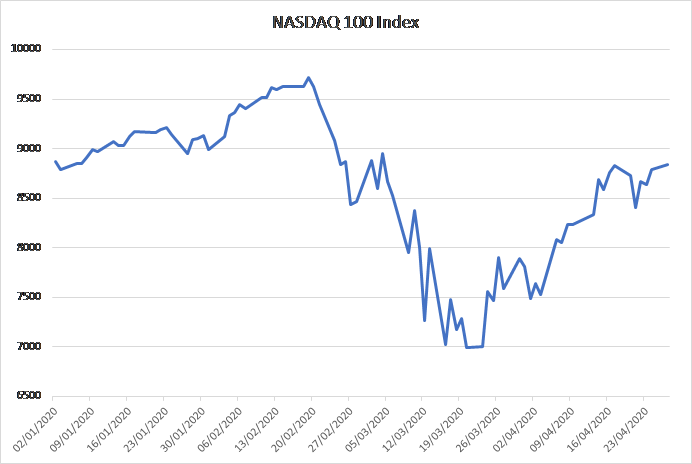

Tech takes the bull by the horns

Taking a look at the tech-heavy NASDAQ index for US equities, we see an even more extreme picture.

Figure 3: Tech index

Source: NASDAQ, Federated Hermes International

The NASADAQ dropped only -32.9% from its peak, recovered +23.4%, with that recovery representing 67.6% of the original losses. This represents quite the bear market rally, and points to a more fundamental shift in market leadership (continuing a trend that has been in place for several years now), both during the initial drop and then certainly in the rally.

The concentration of market cap in the largest stocks has been climbing steadily during the post-GFC bull run, but it has soared during this pandemic crisis. The stock market is in some sense being propped up by a handful of mega-cap tech companies. The five largest stocks in the S&P500 now account for over 20% of its total market cap, exceeding the 18% concentration level reached during the dot-com bubble.

The breadth of the stock market is an indicator of how many stocks are advancing relative to those that are declining, and when a market has narrow breadth it means that a relatively small group of stocks is driving the upside movement in the market, while the majority are not performing similarly, quite possibly even declining. So, while the index as a whole is just c.16% off its record highs reached in February, the median stock remains c.27% below previous highs. Similar past episodes tend to be followed by below average returns, with current narrow momentum reversed.

Does history repeat itself?

All bear markets have some similarities and from that we can conjecture as to how things might pan out going forward. But each of them is of course unique and things never play out exactly as they have in the past. In this crisis, European markets have not recovered as far as US markets, other risk assets such as credit have also recovered but again not by as much as equity leaders.

Global bond yields are still hovering near all-time lows, while cyclical commodities (including oil) for the most part remain under real pressure. Further afield, while gold prices are surging (the home of the bears), emerging market currencies have been struggling against the dollar.

There is no question that a powerful policymaker (governments and central banks) and regulator backstop has been behind this risk rally, in addition to growing optimism on the medical front. Equally market behaviour has started to normalise, even though pockets of illiquidity still persist. The likelihood of second- and third-order effects in risk markets, especially credit, is most certainly reduced, but far from removed completely – defaults, for example, are still inevitably going to happen.