Genius-at-large Mitchell Feigenbaum was always on the move.

But the wandering physicist stayed still long enough in the early 1970s to uncover a fundamental truth about the inexorable path of certain systems as they journey from apparent stability to chaotic behaviour: chaos approaches at a surprisingly regular rate of acceleration.

As discussed in previous editions of Fiorino, it was Edward Lorenz – father of the ‘butterfly effect’ theory – who first showed how stability morphs into chaos while Claude Shannon revealed the information signal buried in the noise.

In a sense, Feigenbaum bridged the concepts of Lorenz and Shannon with an amazing insight first doodled on a pocket calculator in 1975. Using a-then leading edge HP-65 programmable device, he found a range of mathematical functions degrade to chaos in a consistent pattern.

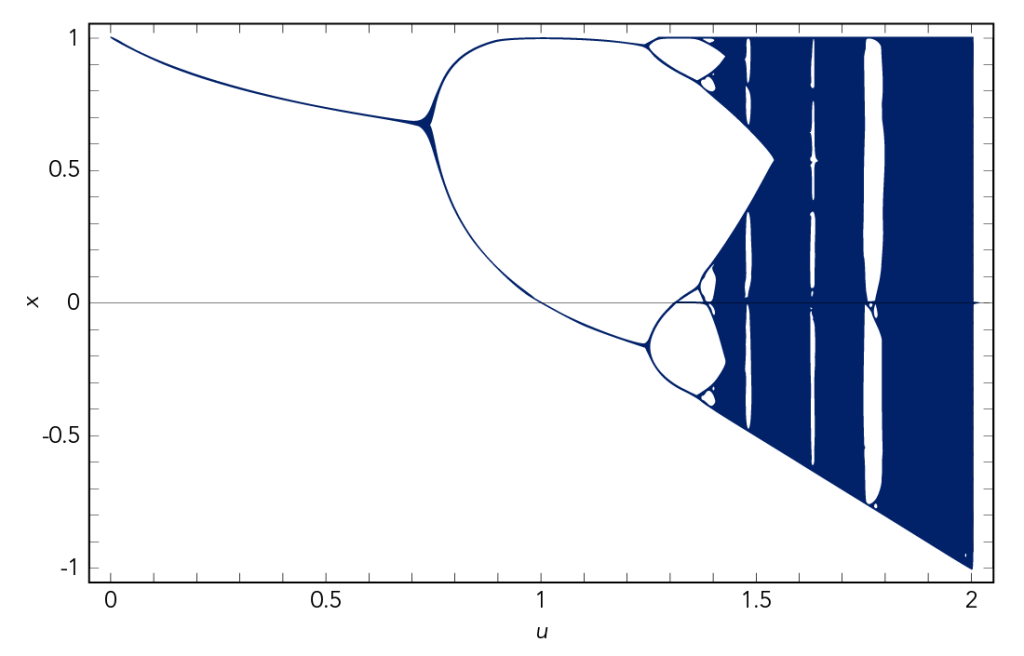

Lorenz had illustrated how certain functions move to chaos via a series of ‘period doubling’ where the system shifts from single-point stability to oscillating between first two points, then four, then eight and so on before tumbling into infinity.

Feigenbaum, however, discovered that the ratio of values between each period-doubling was constant across all chaos-tending systems (defined within mathematical terms) closing in on a rate of 4.669….

Essentially, the first Feigenbaum constant (he actually came up with two constants) implies that change happens slowly at first and then very, very fast.

Figure 1: Feigenbaum constant

Source: Wolfram Math

Box 1: Definitions

Feigenbaum constants: In bifurcation theory, a branch of maths, these are two mathematical constants which both express ratios in a bifurcation diagram for a non-linear map.

Period doubling: boundary region between order and chaos, between smooth flow and turbulence in a fluid. En route to chaos there is splitting of two-cycles into four-cycles, four- into eight-cycles, and so on.

Quick-change sets auto insurers on track to crash with future

Feigenbaum’s constant has since been shown to apply to broad groups of both mathematical and physical systems – and it might even hold a warning for financial industry sectors such as property and casualty (P&C) insurers that could be entering the next period-doubling phase brought on by technological innovation.

Last month Fiorino explored how tech-savvy insurers already use data from social media and the Internet of Things (IoT) to gain actionable insights into policyholder behaviour, supporting underwriting margins in traditional lines of business such as motor, home and health.

Potentially, however, tech might undercut those insurer margins as IoT devices become sophisticated enough to prevent common accidents, damage and injuries at home, in the workplace and on the road.

For example, smarter leak detectors, smoke alarms, and CO2 readers could reduce water damage and fire risks, rendering home insurance policies pointless (or at least subtantially narrowing their scope and lowering premiums).

Car insurance, in particular, appears ripe for a Feigenbaum phase shift as auto manufacturers incorporate safety tech as standard and offer risk cover to drivers directly. Electric vehicle pioneer, Tesla, for instance, has rolled-out its ‘safety score’ system across Arizona, Illinois and Texas after first launching the service in California in 2019.

The Tesla system provides drivers with transparent feedback on their on-road habits, ranking them on an ‘unsafe to safe’ scale (see diagram below). At the same time, Tesla now offers insurance cover for its customers using real-time driver data to assess accident risk (and premiums) in a move that might challenge traditional insurers.

Figure 2: Tesla safety score beta

“[…] In order to calculate your daily Safety Score, we use the Predicted Collision Frequency (PCF) formula below to predict how many collisions may occur per 1 million miles driven, based on your driving behaviors measured by your Tesla vehicle. Driving on Autopilot (including 3 seconds after Autopilot is disengaged) will not be factored into the Safety Score formula, but the miles driven while on Autopilot are included in the total”.

Tesla modelled its safety score system based on six billion miles of real driver data. The company intends to tweak the formula as more information flows from on-road users.

Incumbent P&C insurers stand to face significant challenges if other smart car-makers follow the Tesla lead.

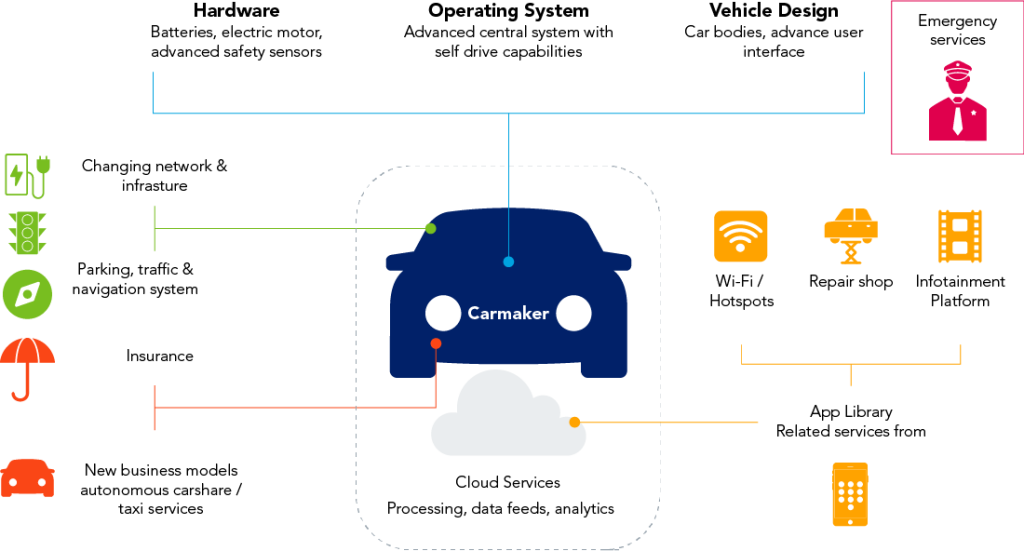

As smart car penetration accelerates (slowly at first, then very, very fast), manufacturers could expand their share of the insurance market thanks to a superior underwriting model and strong customer relationships. In Moody’s model of the tech-centric auto world (see below), manufacturers hold the key to a wider suite of services, including insurance.

Figure 3: The auto insurer-tech ecosystem

Source: Moody’s Investor Service

Importantly, the thin underwriting margin of traditional P&C car insurance (once risks are factored in) and high capital burden in the industry – set by regulation – may deter the big-name data-rich tech firms from entering the market.

Auto manufacturers, many of which already own car-financing subsidiaries, face fewer barriers to entry – and might, indeed, view insurance as a natural next step with revenue diversification benefits to boot.

The exact course of change is difficult to predict with total accuracy but it seems clear that technology will eventually reduce total motor insurance claims costs, possibly outweighing the inflationary impact of expensive in-car gadgetry. As risks and accidents decline, car insurance premiums and profits should follow downwards.

Almost since the birth of the motor car in the late 19th century, insurers have been able to count on recurring revenue as consumers offset the financial risk of driving in ever-more chaotic conditions.

With technology now capable of analysing, and somewhat constraining, the on-road chaos, insurers might be entering a new period where previously stable earnings wobble into uncertainty.

Change is constant, and as Feigenbaum observed in 1975, so is the pace of change. Car insurers may have to buckle-up as future hurtles towards them, 4.669-times faster than ever.

János von Neumann, maths genius (1903 – 1957)