- The S&P 500 and Nasdaq surged on Thursday as investors speculated that latest inflation data may encourage US Federal Reserve to ease the pace of monetary tightening.

- Hong Kong Hang Seng’s Index also jumps after China relaxes quarantine rules amid hopes authorities will loosen stringent zero-Covid policy.

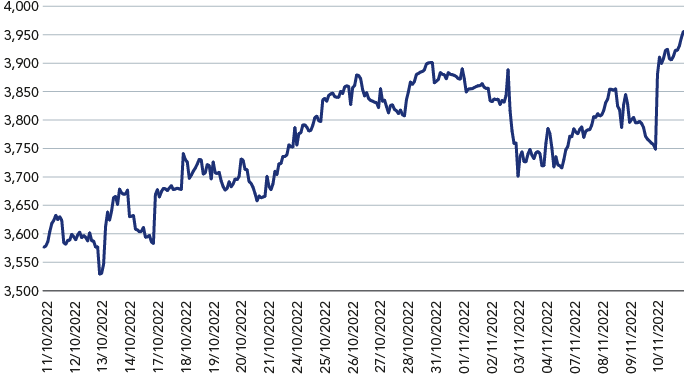

Markets rallied this week after US October inflation data came in lower than expected and China announced an easing of its strict Covid restrictions.

The US blue-chip S&P 500 Index rose 5.5% and the tech-heavy Nasdaq Composite surged 7.4% on Thursday1, the biggest one-day gains in more than two years, as investors speculated that inflation might have peaked, encouraging the US Federal Reserve to ease the pace of monetary tightening.

The Hong Kong Hang Seng Index, meanwhile, jumped 7.7%2,after China reduced the amount of time travellers entering the country must spend in quarantine and removed restrictions on international flights, fuelling speculation that Beijing might begin to loosen its stringent zero-Covid policy3.

Figure 1: S&P 500 surges on October inflation data

The US inflation rate cooled to 7.7% in October, weaker than many forecasts, to hit its lowest level since January4. However, Silvia Dall’Angelo, Senior Economist at Federated Hermes Limited, warned against reading too much into one month’s data. “It does not affect the baseline trajectory for monetary policy in the coming months,” she says.

The Fed raised its benchmark rate by 75bps for the fourth time in a row this month and the latest data may strengthen the case for a modest downshift in the pace of tightening to 50bps in December, Dall’Angelo adds.

“In the short term, the Fed will remain firmly in tightening mode. Inflation is still uncomfortably high, and the labour market remains tight, implying the fight to restore price stability is far from over. Data will continue to define not only the pace of tightening but also the current hiking cycle’s destination. A terminal rate of about 5% next year seems appropriate, but that can change quickly, with risks remaining on both sides,” she says.

US midterm gridlock

Elsewhere in the US, the expected red wave in the US midterm elections failed to materialise, with votes counted so far pointing to a weaker-than-expected performance by some Republican lawmakers in gubernatorial and congressional elections across the country. At the time of writing, Republicans look likely to secure a slim majority in the House of Representatives, while control of the Senate remains too close to call.

“The market was braced for more decisive Republican gains and the indications so far suggest an arguably moral victory for Democrats but a practical outcome that suits neither party,” says Louise Dudley, Global Equities Portfolio Manager, Federated Hermes Limited.

“It looks likely that the Republicans will gain control of the House, albeit with a narrow majority – at the low end of the expectation range that prevailed going into the elections. That would be enough to mark the beginning of a two-year period of divided government and policy gridlock in the US. Gridlock has mixed implications for the economy and financial markets,” says Dall’Angelo.

“From a financial markets’ standpoint, the prospect of no policy change is somewhat reassuring as it implies some sort of certainty, while also matching expectations that had shaped before the mid-term elections. Specifically, gridlock virtually rules out any new fiscal stimulus initiative, with the fiscal stance likely to remain restrictive at a federal level even in a scenario of mild recession in 2023,” she adds.

In bond markets, the yield on the 10-year US treasury had dipped to 3.81% at 12:00 GMT on Friday5.

For further insight on the global macroeconomic outlook please read our latest edition of Ahead of the Curve, Q4 2022.

1 Bloomberg as at 11 November

2 Bloomberg as at 11 November

3 China shortens quarantines as it eases some of its COVID rules | Reuters

4 US inflation cools to lowest level since January | Financial Times (ft.com)

5 Bloomberg as at 11 November