In a new study conducted with Beyond Ratings, ‘Pricing ESG risk in sovereign credit, part II’, Federated Hermes reveals a meaningful relationship between sovereign environmental, social and governance (ESG) scores and CDS spreads in developed markets.

Analysing 5-year CDS spreads and ESG scores from 28 developed market (DM) countries and 31 emerging market (EM) countries during 2009-2018, the study has shown:

- Developed markets: We find a significant relationship between ESG scores and sovereign CDS for both DM and EM. The relationship appears to be stronger for DM.

- Pricing: The relationship between CDS spreads and ESG factors is stable, which suggests a steady pricing relationship

- Sub-factors: The strongest relationship between CDS spreads and ESG scores exists for the social and governance sub-risks, particularly for DMs

In 2019, Federated Hermes and Beyond Ratings published the first part of this study which assessed the correlation between ESG factors and sovereign credit spreads. The results established an inverse relationship: on average, the countries with lower ESG scores have the widest CDS spreads, while those with the highest ESG scores have the tightest CDS spreads. This research has progressed further to investigate which countries in the dataset are driving this relationship. That is why the second part of the study has been conducted, to show whether the relationship is principally driven by DMs or EMs.

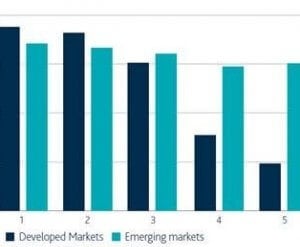

The first stage of the new study looked at the relationship between ESG and CDS spreads in an unconditional way, without controlling for any effects that might influence the relationship. The unconditional average CDS spread was assessed per quintile – data split into five equal groupings based on a country’s ESG score. Apart from a small anomaly in the fourth quintile, the results displayed in figure 1 show a clear observable relationship between ESG strength and CDS spreads for DM sovereigns.

Figure 1: Average CDS spreads by ESG quintile, 2009-2018

Lowest ESG score 5 = higest ESG score

Hermes and Beyond Ratings, as at December 2019

In the empirical analyses of the new paper, we then split the sample into DM and EM groups, and assessed if the relationship between ESG scores and CDS spreads is statistically significant for DM and EM, even after controlling for credit risk, as measured by the sovereign credit ratings. The results show ESG factors have a more significant effect on DM sovereign credit spreads than for EM countries, and the highly significant relationship between ESG scores and CDS spreads documented in the original study is clearly driven mainly by DM countries. Yet despite this statistically weaker relationship, ESG scores do have an impact on EM credit spread.

“With this study, we have provided yet another piece of evidence that ESG factors can be considered as a risk management tool. There are several key learnings which also have important implications for other debt instruments, such as money market securities. It is nowadays imperative to also consider ESG factors in the investment process. The research will help our credit team make better investment decisions and help them price ESG risks with greater precision.”

Julien Moussavi, Ph.D., Head of Sustainable Investment Sovereign Research, Beyond Ratings, said:

“ESG risks are at the heart of sovereign credit risk, and the finance industry is developing its understanding of how both developed and emerging markets are exposed to these risks. By using Beyond Ratings’ ESG scores and historical CRAs’ credit ratings, our model captures the financial materiality of these risks more acutely in the case of developed markets and it unveils that ESG risks are increasingly relevant for emerging markets, although they are yet to be accurately and coincidentally priced. Additional tests using a range of country classifications and explanatory variables at different levels aim to ensure that our main results are robust.”