Fast reading:

- Earlier this week, UBS rescued rival Credit Suisse in a state-backed deal, following a weekend of tense negotiation.

- The US$3.2bn sale1 came as regulators pushed to prevent further contagion across financial markets.

- Top central banks have taken synchronised action to boost liquidity but all eyes are on further action from the Fed.

Markets took a pause from turmoil this week after a series of dramatic bailouts in the banking sector raised concerns around wider fissures on the global economy.

In the space of seven days, four major banks – Silicon Valley Bank (SVB), Signature and First Republic in the US, and Credit Suisse in Europe – were rescued in an echo of the banking sector turbulence that heralded on the global financial crisis of 2008-09.

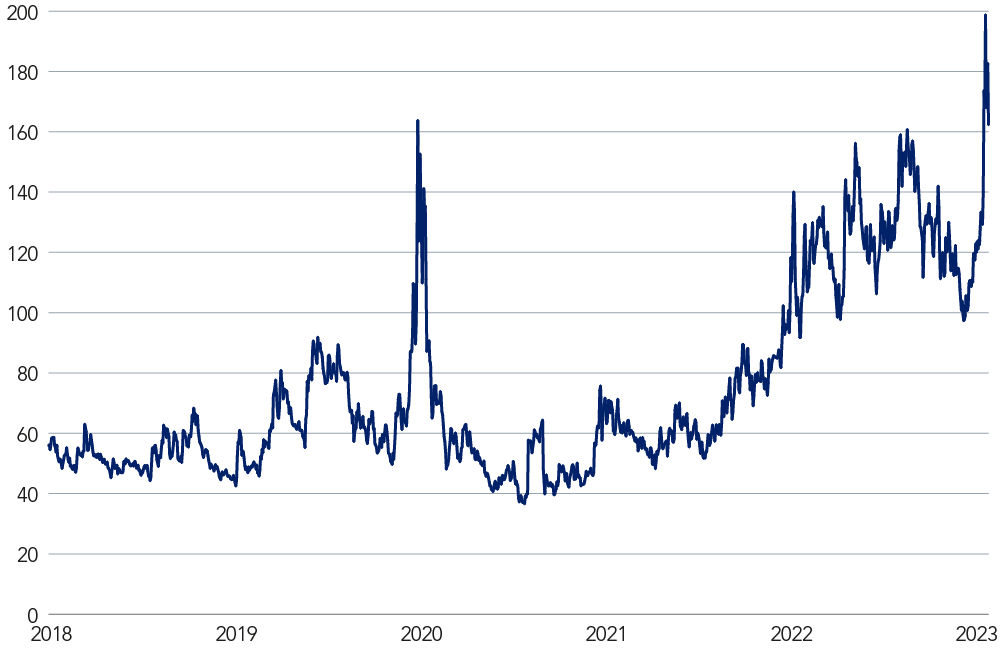

Figure 1: Volatility in front-end rates jump beyond pandemic-level highs

Source: MOVE Index, Bloomberg, as at 21 March 2023.

Silvia Dall’Angelo, Senior Economist, Federated Hermes Limited, downplayed fears of broader market contagion but noted that the events of the past week had sparked a crisis of confidence in the banking sector.

“We are seeing a dip in confidence against the backdrop of an environment of higher rates rather than a spiralling deterioration in fundamentals,” she said, adding that further fallout should be limited by a speedy policy response from central banks.

“Banks with pre-existing vulnerabilities have come under pressure, but policymakers can intervene with short-circuit breakers and that is what they have done swiftly and successfully so far,” she said.

Filippo Maria Alloatti, Head of Financials (Credit), Federated Hermes Limited, highlighted opportunities in the fixed income space, albeit against an uncertain backdrop. “We are positive on duration – our view of falling inflation and slowing growth continues to play out, while strong wage gains and hot labour markets present a barrier to easing,” he says. “At the end of the day, 2023 is about waiting for the impact of last year’s tightening.”

AT1s: At the heart of the storm

Much of the commentary over the past week has focused on the question of additional tier one (AT1) bonds, a class of hybrid debt introduced in the wake of the global financial crisis to boost bank capital and insulate against bailouts.

In the takeover of Credit Suisse, holders of the bank’s AT1 bonds were wiped out in what the Swiss Financial Market Supervisory Authority (Finma) described as a ‘complete write-down’ of their value. Yields on bank debt spiked in response as investors questioned whether this could set a precedent for other additional tier-one bonds.

Michalis Ditsas, Investment Director for Fixed Income at Federated Hermes Limited, said he expected regulators in the UK and Europe would be supportive of the AT1 class – as was the case during 2020 when markets were similarly rocked by Covid-19. Indeed, the strong relative value of the AT1 sector in comparison with corporate debt has further increased over the past few days, presenting attractive investment opportunities, he added.

We are seeing a dip in confidence against the backdrop of an environment of higher rates rather than a spiralling deterioration in fundamentals.

Stock markets were awaiting the response of the US Federal Reserve on Wednesday, following the Federal Open Market Committee’s two-day meeting, as the central bank weighed up whether to press ahead with its tightening plans or pause rate rises in the face of the banking sector turmoil.

Across global stock indices, the equities picture was mixed. In Europe Germany’s Dax and the region-wide Stoxx 600 fell 0.1%2, whereas the FTSE 100 Index was down by 0.3%3 in early trading after the latest inflation data defied economist forecasts and saw an unexpected jump to 10.4% last month4, bolstering expectations the Bank of England (BoE) will raise its benchmark interest rate on Thursday. Asian equities appeared to advance, with the Hang Seng Index adding 1.7%5 as markets reopened from a one-day break.

To find out more about our view on fixed income, please read our latest 360° report.