Riteniamo che l'investimento a lungo termine in società di alta qualità generi rendimenti aggiuntivi nel corso dei cicli di mercato.

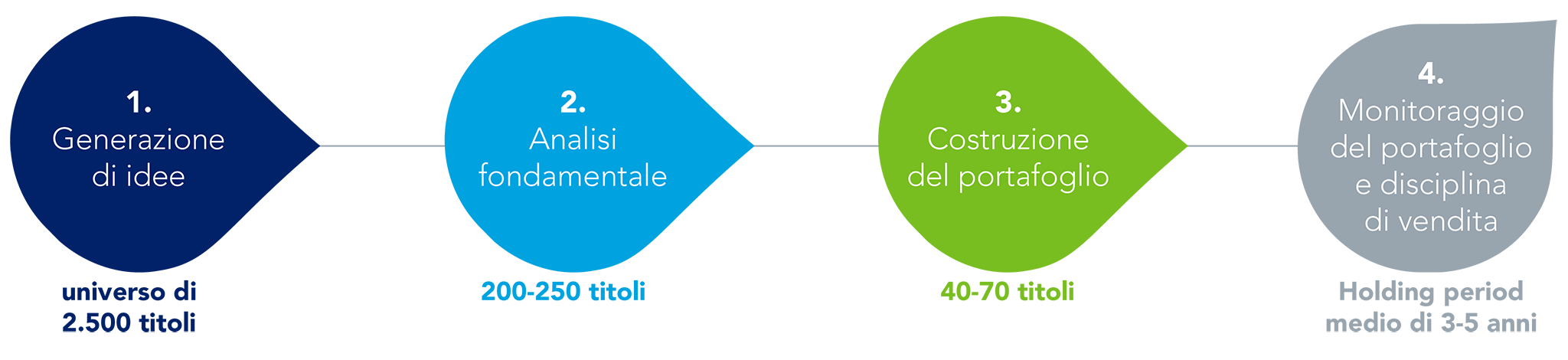

Il nostro holding period tipico di 3-5 anni ci consente di partecipare alle caratteristiche di crescita secolare di molti titoli small cap e sfruttare le tipiche tendenze di mercato di breve termine.

La nostra attenzione alla qualità e alla generazione di flussi di cassa offre un certo grado di protezione dai ribassi, che riteniamo si traduca in una modalità di accesso a questa asset class caratterizzata da un rischio relativamente basso.

Siamo investitori e partner attivi. Nella pratica, ciò significa che manteniamo un dialogo regolare con le società detenute e incoraggiamo solide pratiche ESG.

Federated Hermes Limited gestisce strategie regionali small cap dal 1987.

Mark Sherlock, CFA, FCA

Head of US Equities

Henry Biddle, CFA, ACA

Portfolio Manager

Michael Russell, CFA

Portfolio Manager