- OFR Financial Stress Index at highest-level since onset of Covid-19 pandemic, while other bellwethers have encouraged speculation the Fed could change course.

- Policy shift underway in UK where Bank of England launched emergency QE programme last week following government’s disastrous mini-budget.

Expectations of a pivot in monetary policy have begun to gain traction in financial markets as central banks, led by the US Federal Reserve, come under pressure to ease back on aggressive rate tightening as investor fears grow about the risks of a hard economic landing and a financial crash.

The early signs of a shift in policy are discernible in the UK, following the new government’s disastrous mini-budget on 23 September, which sent markets into a tailspin and led the Bank of England to launch an emergency quantitative easing (QE) programme to buy up UK gilts.

“While recent turmoil in UK financial markets was triggered by imprudent domestic policy announcements, it conveyed a more general message about the fragility of financial markets in an environment of raising rates,” says Silvia Dall’Angelo, Senior Economist, Federated Hermes Limited.

“The risk of severe market dislocations potentially leading to a systemic event has increased substantially,” Dall’Angelo adds. “Accordingly, expectations of a Fed pivot have gained traction in financial markets.”

The US Federal Reserve increased its policy rate by 75bps for the third consecutive time last month and other central banks have adopted similarly aggressive policy tightening as they seek to bring inflation under control¹. But concerns are mounting about how much further the Fed and its peers can continue to hike borrowing costs in the face of a protracted slowdown and a looming recession.

The Fed conducted a similar turnaround in the first quarter of 2019 when halted its quantitative-tightening (QT) programme and began pursuing a mix of backdoor QE and policy-rate cuts – after previously signalling continued rate hikes and QT – at the first sign of mild financial stress and slowing growth².

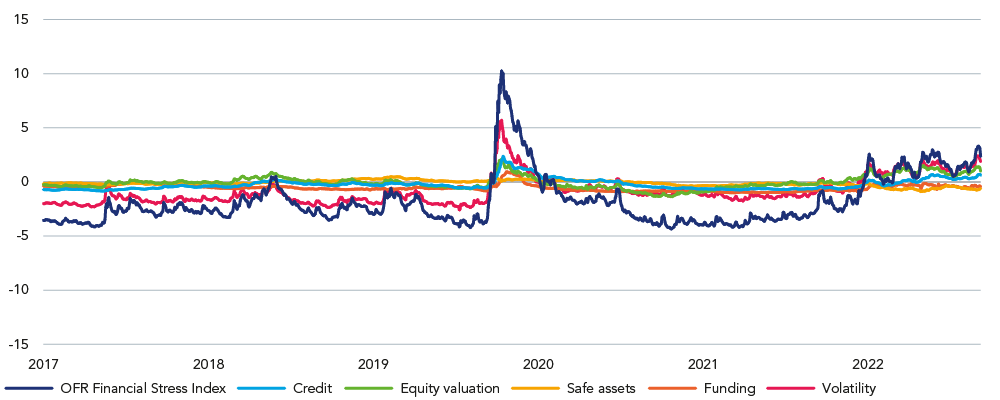

The US Treasury’s Office of Financial Research Financial Stress Index – which acts as a gauge on strains in US markets – hit its highest-level last week since the height of the Covid-19 pandemic (See Figure 1), while other bellwethers such as this week’s worse than expected US jobs data³ have encouraged speculation the Fed could change course on the direction of monetary policy.

Figure 1: US Financial Stress Index on the rise

Embattled equities

The adoption of hawkish monetary policy this year has coincided with equities enduring the longest streak of quarterly declines since the 2008-9 global financial crisis. The pan-European Stoxx 600 closed down 0.6% on 6 October, down 18.8% year to date. The UK FTSE 100 closed down 0.8%4.

“Swings in the equity markets remain broad necessitating the need for diversification across regions, sectors and investment styles,” says Louise Dudley, Global Equities Portfolio Manager, Federated Hermes Limited. “The growth areas of the market continue to suffer, though the spread between value and growth remains consistent as recessionary fears hurt cyclicals and growthier areas are supported by the reassurance of downward pressure on interest rates.”

However, an imminent change to the course of the Fed’s policy trajectory remains unlikely, Dall’Angelo says. “Central banks are slow moving and adjust gradually to incoming information, while financial markets tend to get ahead of themselves,” she says. “The Fed remains seriously concerned by the inflation picture and is laser-focused on the price stability aspect of its mandate.”

Moreover, Fed officials have made it clear that their mandate concerns the domestic US economy, so external spillovers – such as the impact of the strong dollar because of tight monetary policy – do not feature in their reaction function, at least until negative feedback effects become a material threat to the domestic economy, Dall’Angelo says. Most key data points still suggest the US economy remains on a solid footing; with the notable exception of a sharply weakening housing sector. “Central banks [will of course] have to reconsider their policy approach if something big in financial markets approaches breaking point,” she adds.

For further insights into global equities please see the SDG Engagement Equity Fund 2022 H1 Report.

3 US job vacancies plunge by more than 1mn in sign of cooling economy | Financial Times (ft.com)

4 Bloomberg as at 6 October.