Fast reading

- Trump’s proposed tax policies look favourable for the US tech sector as a lower tax burden should free up resources at many industries to spend on technology. Rising tech spend is likely to benefit Taiwan and South Korea as both economies are integral to global tech supply chains as well as the Indian IT service sector.

- US relations with China have steadily deteriorated under President Biden and the de-coupling of both economies is likely to continue. For 2025 and beyond, China’s domestic economic policy will be an important consideration to offset any negative implications from tariffs.

- Tariffs could pose a risk to Mexico. However, the depreciation in the Mexican peso should offset some of the sting from the incremental implementation of any import levies.

- The Indian economy is largely domestically driven, so the impact of any tariffs will be muted. However, the new US administration could seek negotiations to reduce the trade deficit with India, which could affect certain sectors.

The incoming US administration under President-elect Donald Trump heralds a significant shift in domestic and foreign policy – which represents a wide range of potential upshots for emerging markets (EM). However, as outlined below, we do not believe that a Trump presidency 2.0 will undermine the key structural forces that support the long-term growth prospects for EM.

China: various scenarios

Despite Trump’s strident rhetoric on the campaign trail, we do not believe that his victory in the US election is either better or worse for China than had Kamala Harris triumphed.

It’s fair to say that while the trajectory for US-China relations under the Biden-Harris administration was on a predictable and steady path towards decoupling, we now face a situation where both more positive and more negative outcomes are possible.

In our view, Trump is primarily focused on achieving specific economic and political aims rather than being implacably ideologically opposed to China. Under the new US administration we expect further tariffs will be imposed on Chinese imports. However, we believe the threat of sweeping tariffs will primarily be used as a negotiating tactic by the Trump administration as it seeks a trade deal with China that will moderate the trade deficit between the two countries.

Trump is primarily focused on achieving specific economic and political aims rather than being implacably ideologically opposed to China

In light of China’s low household consumption by global standards, we think there is a possible landing area for a deal here.

A lot more of China’s productive capacity has the potential to be absorbed by domestic demand than at the present time; therefore elements of the deal may require the rebalancing of China’s economy towards consumption and supply side restructuring. Such changes would be welcome.

In the event that no trade deal is reached and 60% tariffs on imports to the US are imposed, we would expect China to respond with significant fiscal and monetary stimulus, and also revalue its currency. We believe that all parties will seek to avoid such an outcome as the fallout could have global implications.

However, should this ‘worst case’ scenario come to pass it’s possible that the resultant upheaval spurs fundamental reforms to the Chinese economy, which could have far-reaching and positive long-term consequences. We remain vigilant for such potential silver linings.

In our portfolio allocation, we have stayed away from companies that rely heavily on exports from China to the US because of the acute risks they potentially face.

The People’s Bank of China’s (PBoC) monetary policy measures to spur the economy announced in September have been followed by a US$1.4tn stimulus package, approved by the National People’s Congress in November, to help tackle off-balance sheet local government debt. However, investors seem to have been left disappointed by the scope of the stimulus measures.

Figure 1: China augmented fiscal impulse to GDP

Many market participants nonetheless expect further fiscal expansion in 2025 and additional measures to support the property market and encourage domestic consumption. The PBoC will also remain active in supporting the economy.

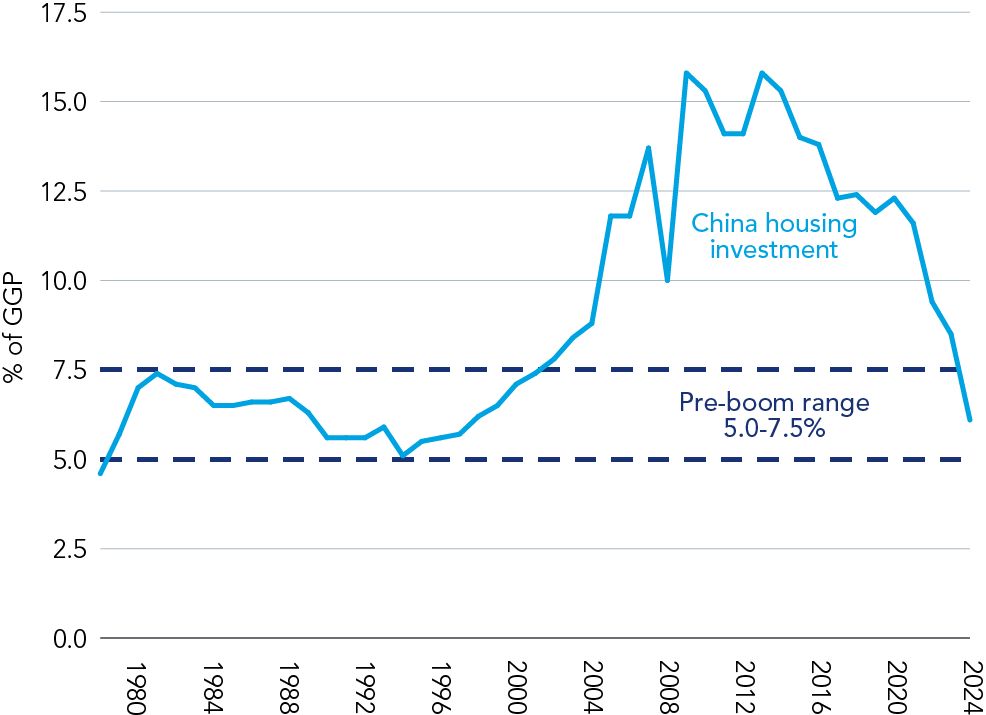

Figure 2: Housing investment in China may already be back to pre-boom range

Taiwan and South Korea’s tech dividend

President-elect Trump’s proposed economic policies – such as tax cuts, boosting domestic production and deregulation – are likely to prove favourable for the US tech sector and they should free up resources at businesses across a range of sectors which they are likely to spend on developing key areas, such as technology.

In terms of tech spend, many businesses in the US have been prioritising investment in artificial intelligence (AI), but this is likely to expand into other areas as the Trump administration cuts taxes and slashes regulation.

Any expansion of the US tech industry is likely to benefit Taiwan and South Korea as both economies are integral to global tech supply chains.

We will of course keep an eye on how new tariffs or protectionist measures might impact Taiwan and South Korea. It is important to note that there is limited global capability to manufacture advanced semi-foundry and memory microchips outside of the two Asian countries. Therefore, any pressure from tariffs will likely be passed on to US customers through higher prices.

Figure 3: Taiwan Semiconductor Manufacturing Company (TSMC) vs. Intel

It’s possible that the incoming Trump administration might seek to modify Joe Biden’s flagship Inflation Reduction Act (IRA). However, we see limited prospects of drastic changes to the programme because foreign companies – such as TSMC, Samsung and Hynix – are central to US efforts to overhaul domestic supply chains.

US chip giant Nvidia, for example, is heavily reliant on South Korean memory chipmaker Hynix; and we expect Nvidia to step up its partnership with Samsung to meet its growing high-bandwidth memory (HBM) requirements. (The only US-based alternative is Micron – which operates on a smaller scale and cannot fulfil Nvidia’s requirements entirely. The portfolio also has exposure to Micron.)

While the outlook for the global tech sector remains positive, we expect a negative knock-on effect for the South Korean electric vehicle (EV) battery businesses from Trump’s proposed removal of EV subsidies in the US. The portfolio has no exposure to such companies and is therefore immune to any big changes to the EV landscape.

India’s balancing act

Relations between India and the US have strengthened in recent years. The US views India as vital strategic partner to counterbalance China’s growing influence in the Indo-Pacific region and this trend is likely to continue under President Trump.

The Indian economy is largely domestically driven, so the impact of any tariffs will be muted. It is worth noting, however, that the previous Trump administration prioritised addressing bi-lateral trade deficits and the new US administration could seek negotiations to reduce the trade gap with India, which could affect sectors such as agriculture and pharmaceuticals.

Changes in the US immigration policies under Trump – such as restrictions on H-1B visas – could affect Indian professionals seeking employment in the US. However, many Indian IT companies with US operations have reduced their dependency on H-1B visa holders and are primarily hiring locally in the US.

Figure 4: Country beneficiaries from production relocation or new capacity

Latin America: strong dollar impact

In Latin America, a lot of focus will fall on Mexico. Trade and immigration were dominant topics during Trump’s campaign.

Tariffs pose a risk to Mexico. However, the depreciation in the Mexican peso – down 17% YTD against the US dollar1 – should offset some of the sting from the incremental implementation of any import levies.

A review of the United States-Mexico-Canada Agreement (USMCA) – a free trade agreement between the US, Mexico and Canada – is scheduled for 2026 but could be moved forward to 2025.

In our view, any short-term uncertainty should give way to a more benign outlook for Mexico over the medium term. It is worth remembering that the last Trump presidency – despite his disparaging rhetoric – worked out quite well for Mexico.

Brazil, meanwhile, could face challenges as the strengthening US dollar puts additional pressure on the Brazilian real. There are concerns that inflation expectations in Brazil are drifting away from the central bank’s target, which could lead to an increase in the pace of rate hikes.

Figure 5: Brazilian interbank deposit rate

The silver lining to this tricky backdrop is that it could support Finance Minister Fernando Haddad’s efforts to rein in public spending, which are a necessary step to improve the country’s fiscal situation.

Conclusion: fundamentals intact

The shift in priorities under the new US administration presents a wide range of potential outcomes for emerging markets. However, it’s worth noting that Trump’s policies also have the potential to destabilise the US economy.

Higher tariffs could increase costs for the US consumers and an expanding fiscal deficit could elevate bond yields and keep interest rates higher for longer, which could drive up borrowing costs for US companies, adding to the US government’s interest expense, which in turn could further squeeze government spending.

Despite the negative headlines, we do not believe that a Trump presidency 2.0 will undermine the structural growth drivers that support EM. Many developing countries have pivoted towards domestic consumption, stepped up investment in infrastructure, and expanded digitisation penetration, driving efficiency and productivity.

Emerging economies control the supply of critical commodities and play a vital role in tech supply chains where there are no credible Western alternatives. Moreover, many EM countries benefit from favourable demographics – and have plentiful supplies of labour – and are therefore unlikely to be impacted by the wage hike spiral which many Western economies may have to grapple with.

Overall, the fundamentals of emerging markets are sound. In times of fiscal profligacy in the West, most emerging economies are doing the right thing by managing the bond market’s expectations. Economic vulnerability is low, structural growth drivers are intact, and valuations in EM equity markets are at a significant discount to developed markets. Most EM countries have not cut rates substantially, and a few EM central banks have already started hiking, highlighting most emerging economies track record of monetary policy prudence.

For more information on Global Emerging Markets Equity.

BD014999