As still taught in most schools, science is traditionally divided into the three distinct disciplines of physics, chemistry and biology that respectively focus on fundamental particles, atoms and molecules, and the amalgamation of complex molecules known as life.

But while specialisation has underpinned much of the historic scientific success stories, the borders between the three categories have always been somewhat arbitrary. Increasingly, researchers in science are looking across all fields of knowledge for inspiration and practical ways to advance our understanding of the world.

For example, according to a Cosmos magazine article, a 2018 study published in the prestigious Nature Chemical journal established “for the first time that at one level photosynthesis is a quantum process”.

The recently discovered link between quantum mechanics and photosynthesis suggests the realms of sub-atomic physics and biology are not the separate kingdoms as described in secondary school textbooks.

In its own way, the study of bank bonds has also made a ‘quantum leap’ since the global financial crisis (GFC) with researchers pushed by necessity beyond the comfort zones of macro-economics and bookish account analysis.

Among other well-documented side-effects, the massive capital injections by various governments to prop up banks during the GFC forced bond researchers to adopt a cross-disciplinary approach that spans an understanding of the legal minutiae of prospectus terms and conditions to regulatory fine-print and political word-smithing.

After all, the government underwriting of bank liabilities came – reasonably so – with a few strings attached. Consequently, in addition to their traditional research duties, the post-GFC financial institution fixed income analyst is also a junior lawyer and, as a former Fiorino colleague quipped, a ‘Sunday economist’.

The broader set of analytical skills is now essential in decoding financial institution securities. For instance, the strong political and regulatory backlash against insurance companies and banks that accepted taxpayer money during the GFC to survive has fundamentally changed the bond market in these sectors.

In the aftermath of taxpayer bailouts, government and public outcry at the sight of financial institution executives pocketing massive remuneration packages amid a severe recession triggered some reforms, including bonus claw-backs (fodder for another Fiorino), especially in Europe and the UK.

At the same time, observers noted that risk-taking investors in fixed income securities well down the institutional capital stack were essentially rescued from GFC oblivion by government largesse.

Both these factors contributed to a rethink of bank capital ratios that culminated in the Basel Committee on Banking Supervision reforms (known as Basel III) that landed in December 2010. Basel III was designed to improve the quantum of capital ratios (in percentage terms) as well of the quality of assets underpinning bank credit – as per the simplified version of the original plan outlined in figure 1.

Figure 1. Definition of capital in Basel III

Thier 1 (going concern) | Common Equity T1 (CET1) | Sum of common shares, stock surplus, retained earnings, OCI, minority interest & regulatory adjustments | CET1>4-5% |

Additional T1(AT1) | Capital instruments meeting criteria for AT1 and related surplus | (CET1+AT1)>6% | |

Tier 2 (gone concern) | Capital instruments meeting criteria for T2 and related surplus | (CET1+AT1+T2)>8% | |

Note: % of Risk Weighted Assets (RWAs). OCI represents other comprehensive income. Source: Federated Hermes, Bank for International Settlements, as at February 2021.

The European Parliament added a few more elements to the Basel III universe after approving the Capital Requirements Directive (CRD4) and Capital Requirements Regulation (CRR) in 2013. In a move that tested the newly acquired legal skills of financial analysts, the 2013 European legislation also mandated a 10-year ‘grandfathering’ transition period between Basel II and the new bank capital regime.

Basel III may not be quite as hard to grasp as quantum mechanics, but like physicists, bond analysts must deal with pragmatic outcomes even in the face of theoretical uncertainties. To quote John Bell, the influential Irish physicist whose work ultimately proved the quantum world is a weird as it seems, sometimes we have to assume the theory works ‘for all practical purposes’ (FAPP) even if the reason why remains obscure.

Applying the FAPP principle to Basel III, we analysts must simply note that one outcome has seen the gradual phase-out of certain disqualified subordinated bonds featuring any of the following qualities:

- step-up at first-call date and in general any ‘incentives to call’, which run counter to the concept of ‘perpetual’ capital;

- dividend-pushers;

- provisions permitting redemption within the first five years; and,

- issued out of a special purpose vehicle (SPV).

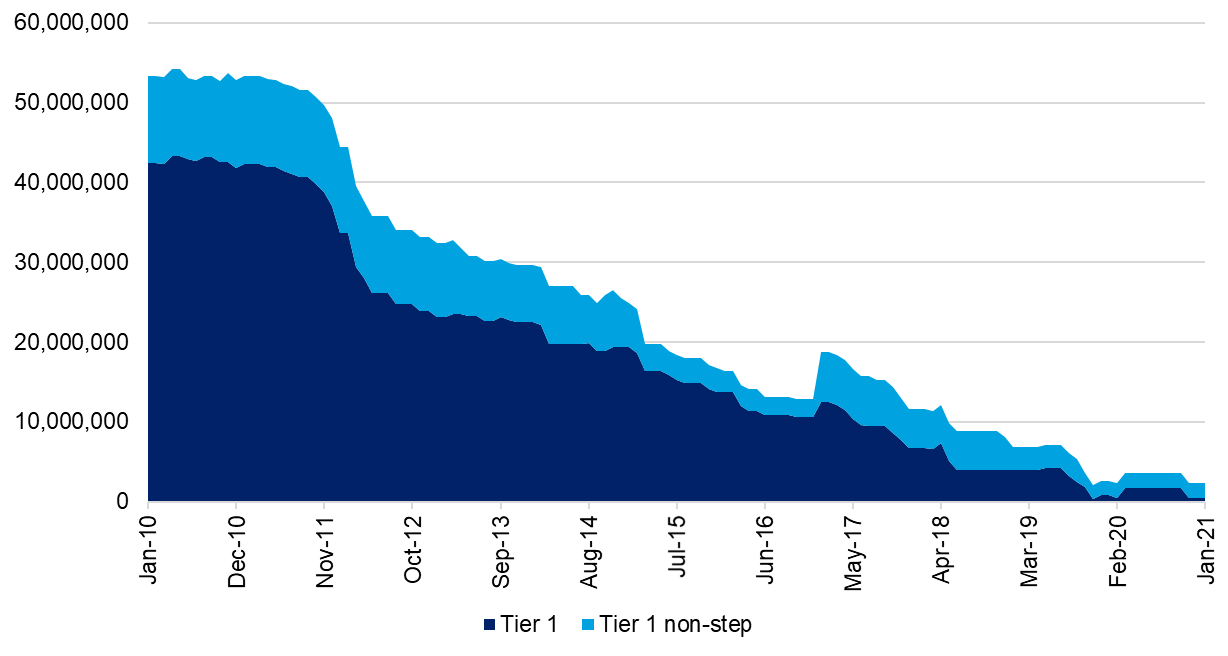

In the post Basel III environment, bank fixed income securities with the above specifications became known as ‘legacy bonds’. By far the largest chunk of legacy bond holdings reside in the Tier 1 (T1) category, lodged among the hybrid and non-step sub-species.

Even before the start of the official Basel III grandfathering period in January 2012 the par value of such legacy bonds had been steadily declining. As of January 2021, the legacy bond component sat at about €2.3bn compared to the €180bn of Additional Tier 1 (AT1) – or ‘new style securities’ – outstanding at the end of 2020. In turn, this represents circa 130bps of the European bank risk-weighted assets (RWAs).

Figure 2. Legacy T1, €bn par amount

Source: Federated Hermes, based on Credit Suisse Contingent Convertible Index data, as at February 2021.

European regulators piled on a new layer of complexity to the bank capital regime on April 16, 2019, with the introduction of the ‘banking package’ – codified as Capital Requirements Regulation 2 (CRR2), Capital Requirement Directive 5 (CRD5) and Bank Recovery and Resolution Directive 2 (BRRD2*) – that defined and extended the scope of the previous legal framework.

In the September quarter of 2020, both the European Banking Authority (EBA) and UK Prudential Regulation Authority (PRA) weighed into the issue with strongly worded advice for bank CFOs: remove ‘infection risk’ from your capital stack.

The EBA published its opinion on legacy instruments with a focus on two issues1 that may create ‘infection risk’ within the capital structure (by disqualifying other parts of the debt hierarchy), namely:

- linkages between the distribution of capital layers (common shares, preference shares, sub bonds, among others) and flexibility (that is, the possibility to turn these distribution payments off if the need arises; and,

- clauses that might contradict the eligibility criteria of subordination.

Meanwhile, the PRA followed suit with a carefully drafted letter to CFOs that will require UK lenders to file an action plan with the regulator by March 31 this year2.

Issuers of legacy securities face several alternative scenarios, including:

- redeem at next call date, usually at par;

- embark on a liability management exercise (LME), buying securities back or exchanging in kind;

- modify the bond terms and conditions (after securing bondholder approval); or

- in exceptional cases, do nothing, leaving the bond outstanding as a ‘non-capital instrument’.

Despite all the mind-bending complexities of the Basel III world for analysts used to the relative simplicity of the pre GFC market, taking a broad approach to researching securities can bring rewards.

The legacy bond market is a case in point. We have been analysing legacy bonds since the GFC through several lenses, concluding that with the asset class facing negative net supply in a world of tightening credit spreads, a multi-disciplinary investor can still discover pockets of value.

Wolfgang Pauli, the late Austrian quantum pioneer

Looking outside the box

Financial market analysis has never been an exact science. As Sir Isaac Newton, a great scientist by any measure, famously noted after losing a fortune in the South Sea Bubble of 1721: “I can calculate the movement of stars, but not the madness of men.”

Uncertainty remains a principle in markets (and indeed in quantum mechanics) but recent history has taught both financial analysts and scientists the rewards of looking outside the box for new ways to manage risk or see the world.

1 See https://www.eba.europa.eu/eba-issues-opinion-address-possible-infection-risk-stemming-legacy-instruments for more information.